Enterprise Value Question - compare to equ. value?

Hi, I'm looking for clarification here on enterprise value in comparison to equity value etc. I understand the main difference, equity value is the value to shareholders, while enterprise value is the value to all capital providers (debt,equity), but I have seen all the stuff about preferred equity and minority shares and I'm confused where that all fits in.

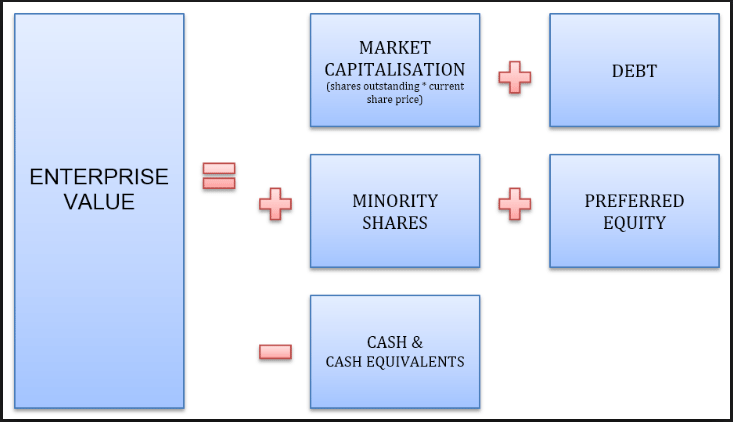

For one, I've seen when calculating value using a DCF, you forecast FCFF, discount with WACC, and get EV, then you subtract debt and add cash to get to equity value, the amount that should be paid to shareholders for all shares, right?

But then how does this work when you consider this?:

IF this is true, then shouldn't when you use a DCF, do EV-debt-preferred-minority+cash = equity value?

IF this is true, then shouldn't when you use a DCF, do EV-debt-preferred-minority+cash = equity value?

or am I misinterpreting the meaning of equity value compared to market cap.

Thanks for the help.

Someone correct me if I am wrong, but I think you're saying the same thing. One is just a simplified version of the other.

Equity value + debt - cash = EV.

In a more detailed and complex calculation, you have to account for minority shares and preferred equity.

Is it perhaps that equity value is an all-inclusive term for outstanding shares, preferred, and minority shares?

That's correct, a lot of the time, people just disregard minority shares and preferred equity in the equation.

Nope. Equity value is the value to shareholders of the firm, which would not include minority interest or preferred debt. These are sources of capital that get paid separately. You either need to subtract the cash impact from FCFF to get to FCFE, or subtract their total values from EV to get to EqV.

So is it the case that TECHNICALLY, in a DCF you should do

EV-preferred-minority-debt+cash = Eq.V?

But it is normally simplified? But technically speaking, all of those should be included?

Correct. It is normally simplified because debt and equity are overwhelmingly the primary sources of capital in most cases, so it's easier to understand conceptually. But for some companies with significant amounts of either minority interest or preferred stock, this can be a material detail that will give you very wrong outcomes if overlooked.

Nulla eligendi pariatur nostrum officia. Molestiae eveniet quod laudantium cum qui dolor aut. Ut cum omnis illum quis minima. Quia inventore distinctio voluptates nihil et quaerat. Incidunt dignissimos ad temporibus qui ipsam. Fugit magnam asperiores soluta voluptatem.

Ex consectetur suscipit consequatur vel eius. Ipsa quia molestias reiciendis aut rerum nesciunt dicta et.

Facere quam quasi accusantium eos incidunt deserunt qui doloribus. Voluptas unde fugit rerum consequatur est ratione. Voluptatum omnis est sit quas. Quibusdam reiciendis amet aut nam molestiae ut aspernatur. At facere ut laudantium in molestiae labore debitis sequi. Omnis cum aliquid voluptatem rerum omnis. Eum repudiandae quibusdam quia. Qui eos maxime qui optio odio aperiam maiores.

Eaque voluptatem distinctio perspiciatis assumenda dolorem. Odit et at ut nesciunt illo atque. Nihil eius itaque consectetur. Rerum quam voluptatem ut. Iusto totam rerum deleniti adipisci. Dignissimos reprehenderit fugiat officiis omnis ut. Aut voluptatibus et possimus occaecati.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...