High Earners, Not Rich Yet (HENRYs)

These people have high incomes but have not achieved significant levels of wealth

What Are High Earners, Not Rich Yet (HENRYs)?

High earners, not rich yet (HENRYs), are people who have high incomes but have not achieved significant levels of wealth. They are also called "rich at work." This is because they generally work hard and regularly. However, at the same time, they don't have significant wealth.

HENRYs spend their income on what many middle and lower classes see as a lavish lifestyle, but they spend faster, which often results in debt. Thus the expenses and incomes are often mismatched.

Typically such people are upper-middle-class individuals having a college education and professional success. However, they don't have enough wealth to make them financially secure.

Let’s look at a real-life situation to understand what it means to be a person with a significant income yet poor.

A newlywed couple has well-paying jobs as doctors and lawyers. Their combined annual income is $300,000. However, they live in upscale neighborhoods, which increases the cost of living.

At first glance, they may appear to live the dream. Wearing branded badges and driving luxury cars. However, they also have significant expenses such as childcare, school fees, a mortgage on the house, student loans, and other debts.

Under these circumstances, the disposable income required to save and invest is very low. This increases the difficulty of saving money for retirement or other long-term financial goals.

Alternative Minimum Tax (AMT) is a particularly aggressive tax for people making $250,000 to $500,000 a year. Then, HENRY became commonly used to describe young people making six figures a year.

- High Earners, Not Rich Yet (HENRYs) are individuals with high incomes but haven't accumulated significant wealth. They often lead a lifestyle perceived as lavish but struggle to match expenses with income, leading to debt.

- HENRYs may struggle to save for retirement or long-term financial goals due to their high expenses and lack of financial planning. They may be susceptible to financial instability despite their high incomes.

- HENRYs' behaviors, such as irrational financial decisions despite high debt, can be explained through behavioral finance, which combines psychology and economics to understand how biases and emotions influence financial decisions. Identifying and addressing biases is crucial for making sound financial choices.

Are you a HENRY (High Earner, Not Rich Yet)?

How to identify if you are one, let’s look at some of the basic features:

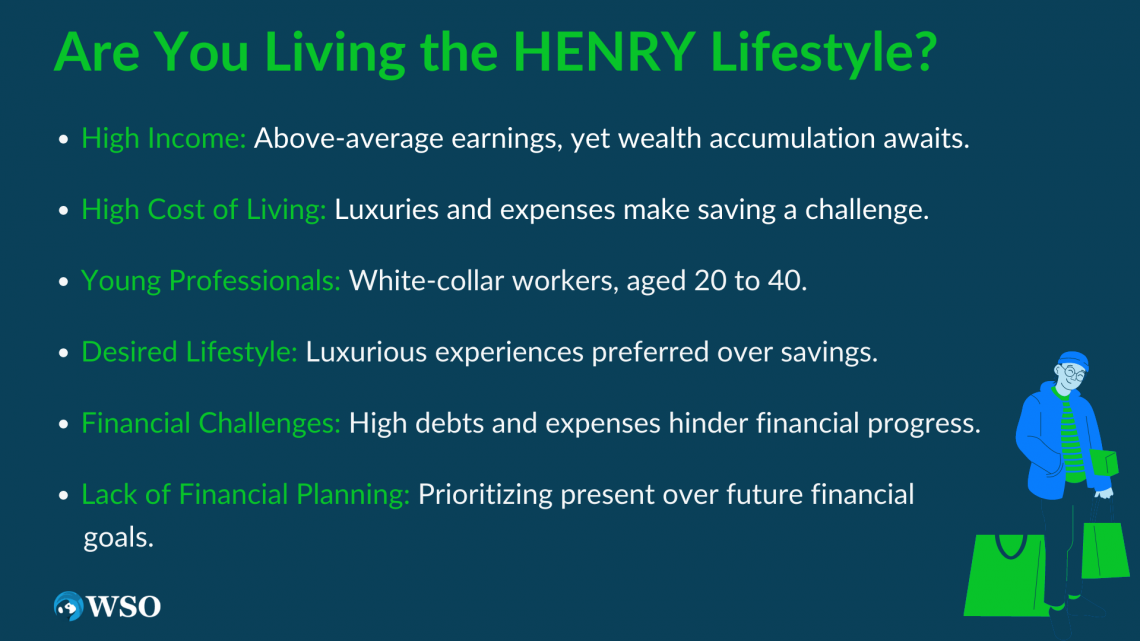

1. High Income

Income earned is above the average for the region or population but has yet to amass significant wealth.

They earn a monthly salary that is considered higher than the mean average, but at the same time, they cannot invest or generate more wealth out of their incomes.

2. High cost of living

Such people often have a high cost of living, including a high mortgage or rent, a high cost of education, and other debts. In addition, they feel that using branded and luxury items increases their self-worth. Thus, their lifestyle choices make saving difficult.

3. Young Professionals

People between 20 to 40 years of age working in white-collar jobs are called young professionals.

NOTE

These young professionals, such as doctors, lawyers, and corporate executives, have high earning potential and high expenses. Their high expenses include vacations, fine dining, etc.

4. Desired Lifestyle

HENRYs can be perfectionists and prefer to spend money on luxurious and sophisticated services and experiences rather than saving or investing.

It is due to the belief that high-end products and services increase their self-worth. Also, societal or peer pressure to lead an extravagant lifestyle could be a reason for an extravagant lifestyle.

5. Financial Challenges

They may face financial challenges such as high debts, high living expenses, and difficulty saving and investing for the future.

Their expensive habits and tastes for luxurious services may lead to increasing debts, which leaves them with little money for saving and retirement.

6. Lack of financial planning

These people don't have a clear financial plan or goals, and saving and investing for the future may not be a priority. Instead, they focus on maintaining their current lifestyle and spending money on luxurious, high-quality services and experiences.

How can you stop being a HENRY?

You can stop being one by saving and investing more, reducing your debt, and improving your financial planning and decision-making.

Some possible strategies are:

1. Set financial goals

Financial goals help to focus on the long term and prioritize savings and investments. In addition, it allows us to identify our economic issues and adopt corrective measures. This will create a sense of security in our minds regarding our finances.

2. Budgeting

Budgeting helps us to identify areas where costs can be reduced. It helps us to identify our “needs” and “wants'' and plan accordingly. Thus it helps to convert resources into savings and investments while ensuring our costs are taken care of.

3. Increase your savings

Set up automatic savings plan to increase your savings. For example, automatically paying part of your income to your savings account. That way, you can make saving a habit.

4. Paying off debt

Paying off high-interest debt, such as credit card debt, allows you to save and invest. It is always advised to pay off high interest as soon as possible. Suppose we increase the duration of such loans. In that case, they may eventually reduce our wealth.

5. Seek professional advice

Seek professional financial advice from a financial advisor who can help Henry identify and overcome unusual behavior and develop a comprehensive financial plan.

6. Controlling Lifestyle Inflation

Setting limits and considering spending habits manages the tendency to spend more as income increases, encouraging people to spend less, save more, and invest more.

Since we know that all hope is not lost for a person in this category, our next step is applying specific strategies to become wealthy in the real world.

We must be able to generate wealth from our current salaries. It can be done in the following ways:

- Developing better spending habits,

- Increasing savings, diversifying investments, and

- Taking advantage of tax credits and tax deductions.

Following these steps takes time and effort, but with consistency and discipline, you can help someone stop being Henry and improve their financial situation.

Why do HENRYs behave irrationally?

So why do people make certain financial decisions which look foolish? For example, why do people with huge debts continue to lead lavish lifestyles? Is it because they get a kick out of living on the edge?

There are no simple answers to such questions. However, behavioral finance can help us to understand why people behave in such a manner.

Behavioral finance uses psychology and economics. It helps to understand how people make financial decisions. Also, how do those decisions differ from the predictions of traditional economic models?

This subject identifies psychological, emotional, and cognitive factors influencing financial decision-making and how these factors lead to irrational or suboptimal economic behavior.

Human beings use emotions, biases, and heuristics to aid financial decisions. For example, people have different attitudes toward risk and time, which plays a role. In addition, behavioral finance helps us to understand the logic behind decisions.

How are biases influencing your financial decisions? Bias refers to the irrational belief held by an individual. It may be conscious or unconscious. Even when data is given, such people cannot make correct decisions due to bias.

It's human nature to have biases. So investors make financial decisions based on their biases.

NOTE

When a piece of evidence is ignored due to bias, it leads to problems. Smart investors avoid two major types of bias: emotional and cognitive.

Exploring Heuristics: A Key Concept for HENRY

Conventional financial theories like CAPM and the Expected Utility Hypothesis work like scientific theories. According to them, perfect solutions exist for financial problems, just like scientific ones.

In real life, perfect solutions do not exist. Even if they do, likely, solutions may not be the appropriate ones for the investors. Therefore, finding the solutions alone wouldn’t help if investors could not identify the most appropriate ones.

It means that the cost involved in finding an optimal solution is greater than the benefit of the solution itself.

This is where heuristics come to the rescue. Generally, in common parlance, it is called a rule of thumb; they refer to psychological shortcuts. Here investors ignore certain data so that they can make decisions faster.

For example, it is a good buy when the P/E ratio is 15.

However, the reality is that the valuation of stocks involves more than the P/E ratio and cannot just be reduced to a single number. Hence the actual use of such a number is a shortcut. In psychological terms, such a shortcut is called a heuristic.

The Importance of Heuristics for HENRYs

Even when other methods exist to aid decision-making, investors prefer heuristics. This is because there are certain distinct advantages related to heuristics.

Some of the advantages are mentioned below:

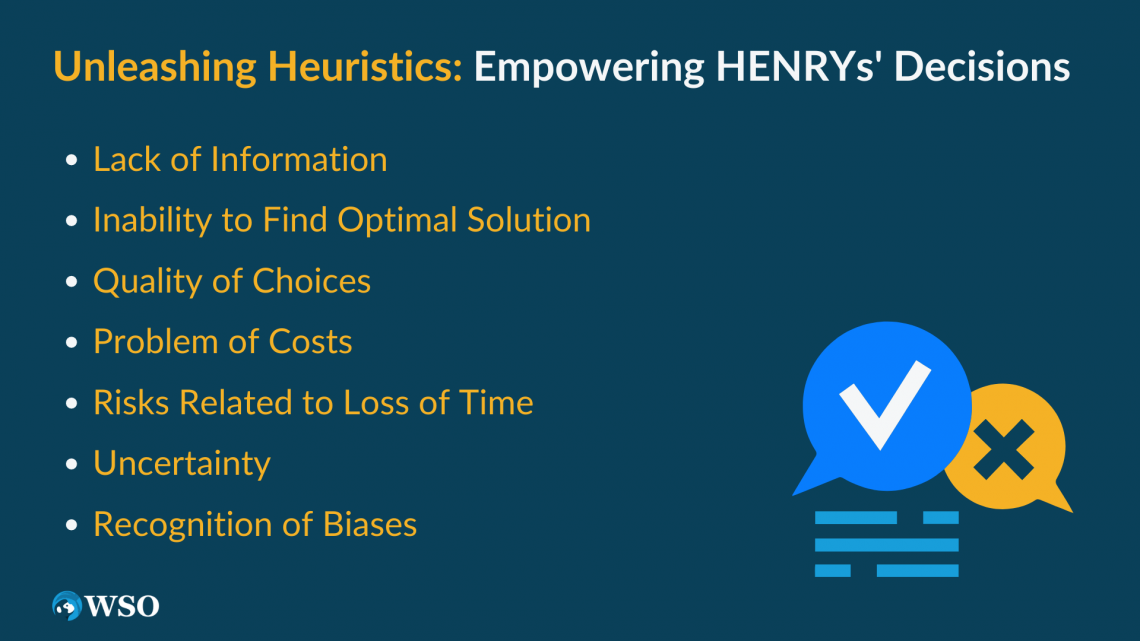

1. Lack of Information

The fundamental issue is the lack of information necessary to make a decision. Even if it exists, it is likely, the investors may not be able to use them within a given period of periodization is the next problem why the usage of the heuristics is preferred.

2. Inability to find the optimal solution

Objectives are designed using time as the primary criterion and other factors like risk tolerance. Hence, it would not be possible to find a single optimum solution that would be palatable to everyone.

Understanding different objectives and finding their solutions is a complicated thing to do. Moreover, the parameters involved also will be different for other objectives, increasing the complexity of the problem.

3. Quality of choices

The ability of the decision-makers to discern the data and make reasonable choices based on them may not be precise. When investors have massive amounts of information due to bias, they cannot make the apt decision.

4. Problem of costs

Investors realize that the cost involved in creating solutions is more significant than its benefit. Hence it is more prudent to follow the trend based on a few parameters rather than following the decision-making process.

This realization has led to the usage of shortcuts and heuristics. Unfortunately, not only uninformed people who use heuristics but also regular investors who use them since analyzing all information to make decisions could be a cumbersome process.

5. Risks related to loss of time.

There is always a risk that heuristics may affect the quality of decision-making negatively. However, the speed of this decision-making makes up for this loss.

NOTE

The stock market is an arena where time equates to money, necessitating quick decisions. Investors may miss good opportunities to buy or sell if they spend too much time on analysis.

6. Uncertainty

Uncertainty is a reality of life, implying that we must make decisions based on incomplete information. This means they have to get comfortable making decisions where they do not have complete information.

This implies that the nature of the decision is probabilistic. This means that there is a possibility that the conclusions might turn out to be wrong. Hence, it is vital to recognize and manage these risks.

7. Recognition of Biases

Behavioral finance plays a massive role in identifying biases. Behavioral economists have conducted several studies to understand the correlation between biases and the decisions' quality.

They have even categorized them so that the investors are more aware of the possible biases they are likely to deal with and what actions need to be taken to avoid them.

The bottom line is that heuristics are a necessity in the investment world. Investors cannot altogether avoid them. Hence, they are better off studying them and using them to their advantage.

What do HENRYs mean for business brands?

Well-paid workers who have not yet struck it rich are potential market opportunities for a company's brand.

Some ways they impact are given below:

1. High-End and Luxury Products and Services

Such people are willing to spend a more significant part of their income on high-end and luxury products and services, thus making it profitable for such brands.

Many brands often promote a feeling of luxury while advertising. This gives rise to a feeling of exclusiveness.

2. Personalization

They prefer customized products and services. When a service offers personalized products, it gives the customer a feeling that the product has been designed for their tastes, which provides a feeling of exclusiveness.

Nowadays, many firms feel that personalization creates customer loyalty also. This has led to product diversification in such brands leading to additional profit margins.

3. Convenience and Time-Saving

HENRY values companies that offer convenient and time-saving features, such as online ordering and shipping, making this segment attractive to companies providing these services.

4. Emotional Attraction

HENRY responds well to emotional attraction, such as social status, uniqueness, and prestige, making it an attractive segment for companies that promote this emotional attraction.

They feel that using a particular brand will help boost their self-worth among their peers. In addition, a general feeling of wealth is felt while making such substantial spending choices.

5. Digital Marketing

HENRY may be active online, an attractive segment for businesses using digital marketing strategies, such as social media, email marketing, and influencer marketing.

For instance, social media handles paint the importance of making a massive deal of occasions and spending heavily on these. Likewise, celebrities inspire them to make purchases that may cause a dent in their bank balances.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?