What Is The Form 8-K?

An 8-K is an SEC filing that companies are required to complete and submit in the event of any situation that may be important to either shareholders or the US Government and SEC.

The 8-K form will include a summary of the event in question as well as any relevant information (i.e., financial statements, press release, the letter from the CEO, etc.).

Important events can include:

- Bankruptcy

- The departure of a key employee (i.e., CEO)

- Change in the Board of Directors

- Corporate activity, such as the acquisition or sale of assets

It must be filed by public companies with the SEC per the Securities Exchange Act of 1934, as amended.

The SEC reports are available through the Electronic Data Gathering, Analysis, and Retrieval (EDGAR) platform.

- Form 8-K is used by public companies to disclose major events to investors in a timely manner. It must be filed within 4 days of a material event.

- Important events that require an 8-K include changes in management, bankruptcy, mergers and acquisitions, changes to the Board, and more.

- The 8-K provides transparency for shareholders by outlining significant events and includes relevant financial statements or press releases.

- There are specific SEC requirements on when an 8-K must be filed, such as for changes in auditors, control, fiscal year, and unregistered security sales.

- By reading 8-Ks, investors can stay informed on material events affecting companies they are invested in that may impact share prices.

Understanding Form 8-K

Form 8-K is a periodic report that publicly listed companies file to disclose material changes. Unlike Form 10-K and Form 10-Q, filed annually and quarterly, a public company files an 8-K whenever a material event occurs.

After any significant event like bankruptcy or the departure of a senior manager, any publicly listed company needs to file a current report on an 8-K within four business days to provide an update.

Stakeholders can count on the information in an 8-K to be timely.

The company must determine if the information is material and submit the report to the SEC.

The form instructs that the following events, among others, require the public company, referred to as the registrant, to file a Form 8K outlining the event:

- Financial statements and exhibits

- Bankruptcy

- Amendments to articles of incorporation or bylaws

- Completion of acquisition or disposition of assets

- Results of operations and financial condition,

- Regulation FD disclosure

- Unregistered sales of equity securities

- Changes in control of a registrant

- Changes in the registrant's certifying accountant

- Changes in or election of directors and senior officers

- Submission of matters to a vote of security holders

- Entry into or termination of a material definitive agreement

Benefits and Criticism of Form 8-K

First and foremost, an 8-K provides investors with timely notification of significant changes at the publicly listed companies defined explicitly by the SEC.

Other events necessary to report in an 8-K are those that the firm considers to be sufficiently noteworthy.

The form provides a way for companies to communicate directly with their stakeholders. The information provided is fair, free, and accurate from being filtered or altered.

It also provides substantial benefits to listed companies. By filing an 8-K quickly, the firm's management can meet specific disclosure requirements and avoid allegations like insider trading.

An 8-K is a highly valuable record for economic researchers. For example, academicians/researchers might study various events' influence on stock prices.

It is possible to study and estimate the impact of these events using regressions, but researchers need reliable data. Because the disclosures in these forms are legally required, they provide a complete record and prevent sample selection bias.

Like any other legal paperwork, the form imposes costs on businesses, such as the cost of preparing and submitting the forms and possible fines for failing to file on time.

Although this is only one small part of the problem, the mandate to file 8-Ks also deters smaller companies from going public in the first place.

Mandating companies to provide information helps stakeholders make wise choices. However, it reduces their investment options when businesses' burdens become too high.

Requirements for Form 8-K

The SEC requires disclosure from publicly listed companies for numerous changes relating to a registrant's business and operations.

The bankruptcy of an entity or changes to a material definitive agreement must be reported. Other financial information disclosure requirements include:

- Substantial impairments

- The completion of an acquisition

- Changes in the firm's financial condition

- Disposal activities

The SEC mandates filing an 8-K for the delisting of stock, failure to meet listing standards, unregistered sales of securities, and material modifications to shareholder rights.

An 8-K is required when a company changes accounting firms used for certification.

Changes in corporate governance, such as amendments to articles of incorporation or control of the registrant, must be reported.

Changes concerning the fiscal year and modifications of the registrant's code of ethics must also be disclosed. The SEC also requires a report upon a director or senior management's appointment, departure, or election.

The form must also be used to report changes related to asset-backed securities.

8-K reports may be filed based on the company's discretion and what it considers to be "material" to relevant stakeholders. This form may also be used to meet Regulation Fair Disclosure (Reg FD) requirements.

When is Form 8-K required?

SEC Form 8-K is used to notify investors of a current event. These types of events include:

- Changes in fiscal year

- Material impairments

- Change in control

- Director elections and departures

- Change in accountants

- Asset acquisition or sale

- Modifications to shareholder rights

- Senior officer appointments and departures

- Consummation of a material

- Costs associated with exit plans or disposal plans (layoffs, shutting down a plant, or material change in services or outlets)

- Mine shutdowns

- Violations of my health and safety laws

- Certain financial obligations (such as incurrence of material debt)

- Events that accelerate material obligations (defaults on loans)

- Failing to satisfy listing requirements or delisting from a securities exchange

- Unregistered equity sales (private placements)

- Determinations that previously issued financial statements are not reliable.

- Amendments to articles/certificates of incorporation or bylaws

- A trading suspension under employee benefit plans

- Amendments or waivers of the code of ethics

- Changes in shell company status

- Results of shareholder votes

- Disclosures applicable to issuers of asset-backed securities

- Disclosures necessary to comply with Regulation FD

- Certain financial statements and other exhibits.

- Other material events

Investors should always read any 8-K forms filed by companies in which they have invested. These reports are material to the company and frequently contain information that will affect the share price.

How to read the form 8-k Items

An 8-K filing typically will only have two major parts: the name and description of the event and any relevant exhibits.

The name and description of the event carry all the information that the company considers material to shareholders and the Securities and Exchange Commission (SEC).

It is important to read this, as it has been deemed "material" by the company.

Any relevant exhibits may include financial statements, press releases, data tables, or other information referenced in the event description.

The SEC outlines various situations requiring filing an 8-K, which contains nine sections within the Investor Bulletin, each of which may have anywhere from one to eight subsections.

The 8-K items are defined in the following table:

| Section 1 | Registrant's Business and Operations |

|---|---|

| Item 1.01 | Entry into a Material Definitive Agreement |

| Item 1.02 | Termination of a Material Definitive Agreement |

| Item 1.03 | Bankruptcy or Receivership |

| Item 1.04 | Mine Safety - Reporting of Shutdowns and Patterns of Violations |

| Section 2 | Financial Information |

| Item 2.01 | Completion of Acquisition or Disposition of Assets |

| Item 2.02 | Results of Operations and Financial Condition |

| Item 2.03 | Creation of a Direct Financial Obligation or an Obligation under an Off-Balance Sheet Arrangement of a Registrant |

| Item 2.04 | Triggering Events That Accelerate or Increase a Direct Financial Obligation or an Obligation under an Off-Balance Sheet Arrangement |

| Item 2.05 | Costs Associated with Exit or Disposal Activities |

| Item 2.06 | Material Impairments |

| Section 3 | Securities and Trading Markets |

| Item 3.01 | Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard; Transfer of Listing |

| Item 3.02 | Unregistered Sales of Equity Securities |

| Item 3.03 | Material Modification to Rights of Security Holders |

| Section 4 | Matters Related to Accountants and Financial Statements |

| Item 4.01 | Changes in Registrant's Certifying Accountant |

| Item 4.02 | Non-Reliance on Previously Issued Financial Statements or a Related Audit Report or Completed Interim Review |

| Section 5 | Corporate Governance and Management |

| Item 5.01 | Changes in Control of Registrants |

| Item 5.02 | Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain Officers; Compensatory Arrangements of Certain Officers |

| Item 5.03 | Amendments to Articles of Incorporation or Bylaws; Change in Fiscal Year |

| Item 5.04 | Temporary Suspension of Trading Under Registrant's Employee Benefit Plans |

| Item 5.05 | Amendment to Registrant's Code of Ethics, or Waiver of a Provision of the Code of Ethics |

| Item 5.06 | Change in Shell Company Status |

| Item 5.07 | Submission of Matters to a Vote of Security Holders |

| Item 5.08 | Shareholder Director Nominations |

| Section 6 | Asset-Backed Securities |

| Item 6.01 | ABS Informational and Computational Material |

| Item 6.02 | Change of Servicer or Trustee |

| Item 6.03 | Change in Credit Enhancement or Other External Support |

| Item 6.04 | Failure to Make a Required Distribution |

| Item 6.05 | Securities Act Updating Disclosure |

| Section 7 | Regulation FD |

| Item 7.01 | Regulation FD Disclosure |

| Section 8 | Other Events |

| Item 8.01 | Other Events (The registrant can use this Item to report events that are not specifically called for by Form 8-K, that the registrant considers to be of importance to security holders.) |

| Section 9 | Financial Statements and Exhibits |

| Item 9.01 | Financial Statements and Exhibits |

Example of Form 8-K

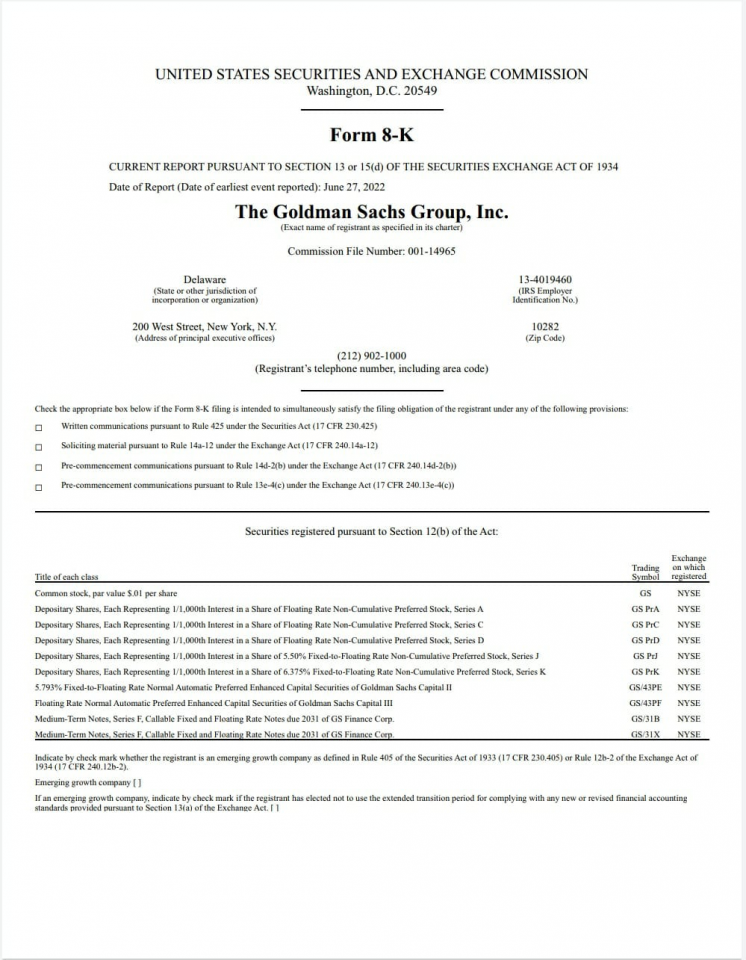

An example of Form 8-K is:

The Goldman Sachs Group, Inc. is an American multinational investment bank and financial services company headquartered in New York City. On 27th June 2022, it filed an 8-K with the SEC

Form 8-K FAQs

No, The company may include multiple items in a single 8-K, and any exhibit can be cross-referenced within the same form. Common instances when this is necessary include:

- Acquisitions (under Item 1.01 and Item 2.01 )

- Unregistered offerings of securities (under Items 1.01 and 3.02 )

- Changes to securities (under Item 3.03 and Item 5.03)

- Appointments of officers (under Item 5.02(c) and Item 1.01 )

- Additions of directors (under Item 5.02(d) and Item 5.03)

Yes, triggering events apply to both issuers and subsidiaries, such as an entry by a subsidiary into a non-ordinary course definitive agreement is material to the issuer. It is to be reported under Item 1.01.

Subject to certain exceptions, an SEC Form 8K must generally be filed within four business days of the triggering event.

Yes, once the notice of termination under the terms of the agreement has been received, an 8-K is required.

No, this situation is not covered under the “is removed” phrase.

If the director, upon receiving notice from the issuer that it does not intend to nominate them for reelection, then resigned their position as a director, then an 8-K would be required according to Item 5.02.

Suppose the director tells the issuer that they refuse to stand for reelection. In that case, an 8-K is required because the director chose a “refusal to stand for reelection,” whether or not in response to an offer by the issuer to be nominated.

- (Item 8.01) Voluntary disclosures have no deadline;

- Regulation Fair Disclosure (Reg FD) filings must be

(i) concurrently with the release of the material that is the subject of the filing (if such material information is intentionally released to the public) or

(ii) the next trading day (only if the release was unintentional);

- (Item 2.02(b)) Filing of earnings press releases must be completed before any associated analyst conference call;

- The announcement of officers until another public announcement of the appointment (e.g. press release, trade conference, etc.);

- (Item 4.02)The filing related to an issuer’s receipt of an auditors’ restatement letter must be completed within two business days;

- (Item 9.01) the financial statements of the acquired business must be filed within 71 calendar days after, the initial report on the 8-K must be filed (four business days plus 71 calendar days)

or Want to Sign up with your social account?