Accrued Liability

An accounting concept is a business expense incurred in a given period but not yet billed for.

What Is Accrued Liability?

Accrued Liability is an accounting concept that is a business expense that is incurred in the given period but not yet billed for.

Accrued liabilities are used when a company adopts the accrual accounting method. They stand for the firm's expenses that have not been billed yet but must be displayed in financial statements.

These expenses correspond to the accounting period in which they were incurred, and the supplier did not bill the firm at any point during that period.

It matters when the supplier bills the firm for the provided goods or services. This aspect is critical because once the expense is billed, it becomes account payable.

Suppose the firm is billed during the corresponding accounting period. In that case, the company will display an account payable, whereas if the firm is billed in any other accounting period, the firm will display an accrued liability until billing.

Accrued liabilities are recorded to help investors better understand a firm's financial position and operating costs.

This accounting term can be seen in the balance sheet predominantly under the current liabilities section. However, in some cases, it could be a non-current liability.

Accrued liabilities cannot be due or overdue because they are not billed. Once that happens, they become accounts payable. Accounts payable, in turn, can be anticipated or overdue.

Accrued liabilities and accrued expenses are the same things. Therefore, they are adjusted at the end of every accounting period.

When this liability is fully paid, it gets reversed, or perhaps more intuitively, it is eliminated from the liabilities section of the balance sheet.

The firm might be obligated to record accrued liabilities depending on the accounting method.

The accrual accounting method uses the matching principle, which states that expenses must be recorded on the day or period they were incurred to reflect financial performance better.

We will get to the accrual accounting method later.

- An accrued liability refers to an obligation that a company has incurred but has not yet paid or recorded through the standard accounts payable process.

- Accrued liabilities arise due to the accrual basis of accounting, which requires expenses to be recognized when incurred, regardless of when payment is made.

- Accrued liabilities appear as current liabilities, affecting the company’s working capital and liquidity ratios and increasing the total expenses recognized, reducing net income for the period.

- Challenges with Accrued Liabilities include requiring careful estimation and judgment to record liabilities that have not yet been billed or paid accurately. Incorrect estimation can lead to misstated financial statements and affect decision-making.

Types of Accrued Liabilities

Accrued liabilities are split into two types. They are discussed below.

Recurring or Routine

These accrued liabilities are generally part of the daily operations of a firm.

One example that would perfectly fit in this category is accrued wages. The firm benefits from working hours, and in exchange, it will have to pay its personnel an agreed sum of money.

Because earnings reports have a predetermined date which doesn't necessarily have to be the exact day on which all employees are paid monthly, the owed money represents accrued wages.

In addition, employees are not required to bill the firm for their work; hence, it fits the definition of accrued liabilities.

Imagine that a firm's Q2 (15th of April - 15th of July) is announced, and employees are paid each month's end.

In the balance sheet, accountants will account for the owed money earned by employees since the beginning of July.

The balance sheet must reflect the firm's financial position as of the end of the latest accounting period, in this case, July 15th; therefore, accountants must report the accrued wages.

Infrequent or Non-routine

In this case, the accrued liabilities are not part of the daily operating activities. Instead, they are relatively large orders or service requests for which the company was not billed yet.

Since these orders do not regularly occur, they go under infrequent or non-routine.

Accrued Liabilities examples

Companies accrue liabilities in several instances.

These liabilities will be displayed in the corresponding accounting period's financial statements. Below you have some common examples:

- Accrued services: The firm received services and is yet to be billed by the supplier, but in the meantime, it must release the quarterly earnings report or financial statements

- Accrued wages and bonuses: The firm pays salaries and bonuses on a predetermined schedule, and the reporting date sits between the date of work commencement and payday

- Accrued pension liability: Employee's benefits earned under a pension plan will be paid in the future after the reporting day

- Accrued interest expenses: Accountants must report the firm's financial position before interest owed to a lender is billed.

- Accrued taxes: Taxes incurred by the firm which will be paid in the future after the reporting date

- Accrued rent: Incurred rent that will be paid in the future after the reporting date

reversing Accrued Liabilities

Accountants use journal entries to record and deduct accrued liabilities. The process requires three account types: an expense account, an accrued liability account, and a cash account.

Initially, when the good or service is incurred, the expense account is marked with a debit (which means an increase), and the accrued liability account is marked with a credit (which means a decrease).

In this manner, accountants account for this liability when reporting quarterly earnings releases or financial statements.

Once payment is made, the accountants reverse the transaction meaning they debit the accrued liability account and credit the cash account.

Let's understand this process using an example.

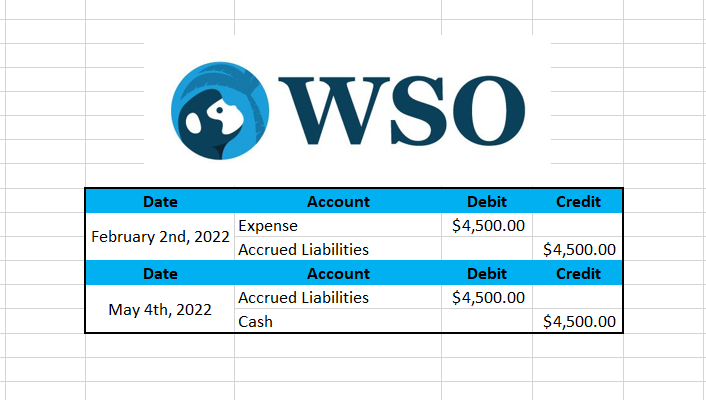

WSO requested the services of a finance icon to mentor people of all ages, answer their questions, and help them reach their goals. WSO will pay after services are delivered.

The two parties shook hands, and the results were terrific. The total amount for the services provided is $4500.

Being a busy businessperson, the finance icon did not bill WSO once the services were delivered on the 2nd of February, in WSO's Q1 (WSO's first accounting period/quarter of 2022).

Instead, WSO was billed on May 4th, in Q2 (WSO's second accounting period/quarter of 2022), and completed payment in Q2.

Because this expense is not billed in the corresponding accounting period, Q1, it will be displayed as an accrued liability.

The accountants working for WSO must use the accrual method of accounting. Therefore, they first debited the expense account by $4500 and credited the accrued liabilities account by $4500 on the 2nd of February.

On the 4th of May, WSO received the bill and completed payment to the finance icon. The accounting team debited the accrued liabilities account by $4500 and credited the cash account by $4500 on the 4th of May.

The accrued liability account can be seen as the middleman between the expense and cash accounts. The need for this middleman is to justify the time in between transactions.

As you can see, it is firstly credited and then debited with the same amount once payment is made. Hence, it is effectively net-zero and canceled in the accounting period payment happened.

That leaves the expense account debited and the cash account credited with the same amount.

Accrued Liabilities vs. Accounts Payable

When the company received the goods or services it was looking for. Still, the supplier has not billed the company yet, and accountants must release financial statements immediately; the owed amount goes under the term accrued liability.

If the supplier bills the company before the reporting date, the owed amount will become an account payable, and accountants will record it in the financial statements or reports.

For future reference, the reporting date is the same as the end of an accounting period.

For example, let's assume a start-up received the WSO Accounting Foundations Course on the 24th of June to equip its staff better to deal with all the financial statements requested by an investor.

The investor wants the statements at the end of the financial quarter that ends on June 30th. WSO will bill the start-up two weeks after it provides the course, on July 8th.

Therefore, the start-up will record the owed amount for the course as an accrued liability on the balance sheet. The investor received the financial statements and was impressed by the performance.

After two weeks, WSO bills the start-up; however, it cannot afford to pay immediately. As a result, the owed money, which was once presented to the investor as an accrued liability, is now account payable.

From this example, you can tell that the day the goods or services were received, the reporting date, and the billing date determine whether the owed amount is an accrued liability or an account payable.

Since the reporting date is between the receiving date and the billing date, the amount will be shown on the balance sheet as an accrued liability.

Had the investor requested the financial statements after WSO billed the start-up, he would have read an account payable.

Both accrued liabilities and accounts payable are liabilities to the company. Accounts payable typically come with a due date for payment.

Accrued liabilities accounting methods

Accrued liabilities are only used when the company adopts the accrual accounting method. There are two methods of accounting:

1. Accrual accounting

2. Cash accounting

Accrual accounting

It is an accounting method under which expenses are recorded as soon as the good or service is received, not on the day the costs were paid.

Similarly, revenue is recorded on the day you finished delivering the good or service, not on the day you got paid for it.

Let's say you are an accountant for a large company specializing in making donuts. The company purchased a robot to increase its production. But unfortunately, it will take five months for the supplier to bill the company.

As soon as the delivery of the robot is confirmed, your next thought is whether the supplier will issue the bill before the end of the accounting period you are currently in.

Days go by with nothing happening, and you are one day shy of the reporting date. It would be best if you recorded this incurred expense since the donut company must use the accrual accounting method.

Therefore, you must release your account for this expense in the books, statements, or reports rather than wait to receive the bill and fulfill payment then act.

On the other side, a multinational corporation reached out to your roofing firm to build a roof for one of their warehouses. The employees completed the project, and your firm will bill the corporation in the next accounting period.

Your firm's accountants will record the accrued revenue in the reports and statements issued for the current accounting period when the job got done.

Again, the accountants will not wait until the bill is issued and payment is made to record the revenue because your firm must use the accrual accounting method.

The timing of financial transactions is crucial since it is much easier for an investor to get a holistic image of the company's financial position and a more realistic idea of expenses and income during an accounting period.

Revenue is earned once the good or service is transferred to the customer.

Taxes are deducted for the tax year in which the income is earned regardless of when payment is received. So, for example, let's assume a firm uses the calendar year (1st of January - 31st of December) as the tax year.

If the firm earned one million dollars in December of 2022 and receives payment in May of 2023, it will pay taxes corresponding to the 2022 tax year, not the 2023 tax year.

Depending on the tax scenarios, this can favor or disadvantage the firm.

One downside to this method is that the balance on the bank account does not perfectly reflect the performance in the accounting books.

The revenue or liability was recorded, but cash has not yet exchanged hands, and only the latter affects the bank account.

This method is used more than the cash accounting method.

Cash accounting

It is an accounting method under which expenses are recorded when payment is made, and revenues are recorded when payment is received.

For example, as the accountant for the same company that makes donuts, you will record the expense when payment for the robot has been completed.

On the other side, your roofing firm's accountants will record the revenue when payment for the project by the multinational corporation is received.

This method does not accrue liabilities or revenue and does not use accounts receivable and accounts payable, so it is less cumbersome.

Another benefit is that income is not taxed until the money hits the bank account.

Usually, this method is adopted in the United States of America by small businesses that qualify according to the IRS's criteria to opt for such a method.

Accrual accounting vs. cash accounting

Businesses must record their financial transactions in a ledger to file taxes or claim tax deductions. This activity is called bookkeeping and requires one of the two accounting methods.

The critical difference between the two methods is the day the expense or revenue is recorded.

The accrual accounting method does not require payment to be made or received for the financial activity to be recorded, whereas the cost accounting method requires this.

A firm can use the cash accounting method and pay professionals to convert its books to the accrual accounting method to file taxes.

The cash accounting method has some major flaws that are absent in the accrual accounting method.

Before mentioning the flaws, it is essential to understand that the cash accounting method creates a lag between the activity and payment for the activity.

If someone wants to know a firm's financial position using such an accounting method during the lag period, that person will likely get a false view of the position.

For example, on July 1st, a company using the cash accounting method received millions of dollars worth of wood as part of a large order.

It will pay for the wood in a month because the supplier allowed for a due date one month after delivery.

On July 15th, the company will speak with an investor about raising capital in exchange for equity.

The investor will require the latest financial information, but this liability will not appear on paper since the company wants to pay for it on August 1st.

It is a due liability that is not recorded and therefore hidden from the investor. This is a big problem, given that the investor wants to know everything about the company.

The company can overstate its financial position by not shedding light on the due liability.

Conversely, a company could have finished a project worth millions in revenue while conversing with an investor to raise capital in exchange for equity.

If the customer can not pay shortly, the company can not record the revenue since it uses the cash accounting method. This will result in the company understating its financial position to the investor.

It is true, however, that these problems can be solved through communication and providing legitimate proof of any claim.

However, they can also be resolved using the accrual accounting method instead.

In the United States of America, the IRS lays down whether a firm has the freedom to choose which method to use for tax purposes or whether it must comply with the decision of the IRS in a specific way.

To change from one accounting method to another in the United States of America, firms have to file Form 3115 and receive approval from the IRS.

Conclusion

An accrued liability is a payment obligation, which must be displayed at the end of the corresponding accounting period, that a company incurs in exchange for goods or services received from a supplier who has not billed the company before the end of the related accounting period.

An accrued liability becomes an account payable once the supplier bills the firm, so it matters when the supplier manages to do that.

Timing of financial events or transactions is essential because it allows people from outside the firm to get a clear view of how the business runs.

Furthermore, the timely display of incurred expenses in financial statements or other documents provides an accurate image of the firm's financial position or health.

The account is credited when the expense is incurred and then debited when payment is made, thus, bridging the expense account to the cash account.

This term can be seen in the balance sheet typically under the current liabilities section, although in some cases, it could be found under the non-current liabilities section.

It is adjusted at the end of every accounting period.

Researched and authored by Bogdan-Remus Pintilie | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?