Allowance for Doubtful Accounts

An estimate made by a business for the amount of its accounts receivable (money owed to the company by its customers) that will not be collected.

What is the Allowance for Doubtful Accounts?

Allowance For Doubtful Accounts is an estimate made by a business for the amount of its accounts receivable (money owed to the business by its customers) that will not be collected.

It provides a more accurate picture of the company's financials by including the expected level of uncollectible accounts.

This estimate is based on the business's experience with uncollected accounts and any specific information about individual accounts suggesting that payment may not have been received.

Doubtful accounts are considered contra assets because they reduce the account receivables amount.

This allowance tries to predict the percentage of receivables that may not be collectible, but actual customer payment behavior can vary greatly from the estimate.

Here is a quick recap about contra assets:

Contra assets are accounts used to reduce the value of a related asset account on the balance sheet. They are recorded with a credit balance, opposite to asset accounts' normal debit balance.

Examples of contra-asset accounts include:

- Accumulated depreciation is a contra-asset account that records the total amount of depreciation for a fixed asset over its useful life.

- Contra inventory accounts are used to adjust the value of inventory on the balance sheet to account for factors such as damage, obsolescence, or loss.

- Allowance for doubtful accounts

Contra assets are used to reflect the decline in value or the expected reduction in the value of the related asset and provide a more accurate picture of the company's finances.

- The allowance for doubtful accounts is a contra-asset account on the balance sheet that represents the amount of receivables a company does not expect to collect.

- This account is used to estimate and account for potential losses due to uncollectible accounts receivable.

- The four most common methods for estimating an allowance are the Percentage of Sales, the Percentage of Receivables, the Aging of Accounts Receivable, and the Other Factors Method.

- The purpose of allowance for doubtful accounts is to ensure that the company’s financial statements present a realistic view of its financial position by accounting for potential losses.

Definition of Allowance for Doubtful Accounts

Companies use this contra-asset to manage their accounts receivable balances. In accounting, accounts receivable details the money that a company is owed by its customer base and has yet to receive payment.

While businesses expect their customers to pay for the goods and services they provide, some will not be able to partially or fully pay their dues. This can happen for many reasons, including bankruptcy or financial difficulties, and it leads to uncollectible accounts.

To address the risk, companies establish a contra-asset account that reduces the gross accounts receivable balance.

The allowance for doubtful accounts is calculated as a percentage of the accounts receivable balance the company expects to become uncollectible.

The percentage is determined by management's estimate of how much of the accounts receivable balance will eventually become uncollectible.

Companies typically use historical data, industry trends, and their experience with individual customers to make this estimate.

Let’s see an example:

Company XYZ has $2,000,000 in receivables. The company estimates that 5% of those accounts will become uncollectible, so the allowance for doubtful accounts will be $100,000.

The allowance reduces the gross accounts receivable balance to $1,900,000, providing a more realistic representation of what the company expects to receive.

Note

The allowance for doubtful accounts is a management estimate and may not always be accurate. If the actual amount of uncollectible accounts receivable exceeds the estimated allowance, the company may need to adjust for the future.

Purpose of Allowance for Doubtful Accounts

The purpose of allowance for doubtful accounts is to manage the risk of uncollectible accounts. Companies often extend credit to customers and allow them to pay at a later date. This creates an account receivable section in the balance sheet.

However, not all customers will pay their bills on time or at all. If a company does not estimate the number of uncollectible accounts, it will overstate its assets, revenue, and net income.

The overstatement can mislead investors and other stakeholders, leading to incorrect business decisions.

By creating an allowance for doubtful accounts, a company can anticipate the loss due to bad debt and account for it in advance.

This allowance helps companies avoid overstating their assets, revenue, and net income, making their financial statements more accurate and reliable. It also helps companies manage their cash flow and plan for future expenses and investments.

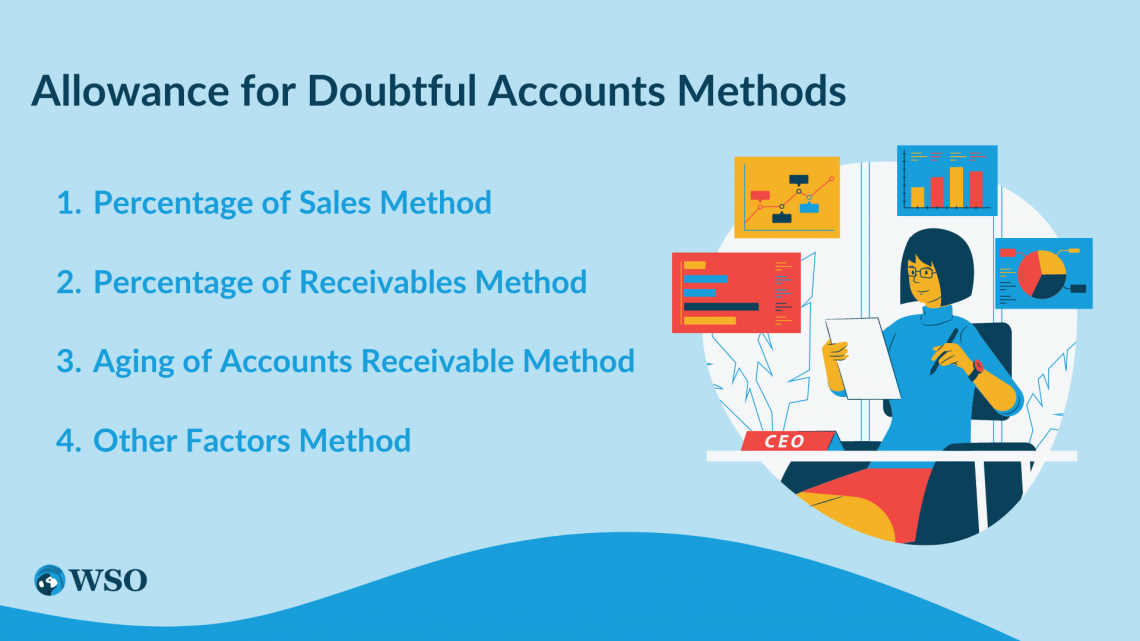

Estimating an allowance for doubtful accounts is an essential aspect of company accounting. To do this, companies use various methods to calculate the estimated number of uncollectible accounts that need to be reserved.

The four most common methods include the following:

Percentage of Sales Method

The allowance for doubtful accounts is estimated as a percentage of total sales, useful when sales and bad debts are strongly correlated.

The estimation may not be suitable for businesses experiencing significant fluctuations in sales or bad debts.

Percentage of Receivables Method

The allowance for doubtful accounts is estimated as a percentage of the accounts receivable balance, useful when the collection history is consistent.

Inconsistent collection history may affect the accuracy of using the percentage of accounts receivable balance to estimate the allowance for doubtful accounts.

Aging of Accounts Receivable Method

The allowance for doubtful accounts is estimated based on the age of each account, which is useful when there are many accounts with varying collection histories.

When the age of accounts varies significantly or inconsistent payment histories are present, using the age-based estimation method to manage accounts may not be effective.

Other Factors Method

The allowance for doubtful accounts is estimated based on other factors, such as customer creditworthiness and economic conditions, which is useful when a more nuanced estimate is needed.

Considering customer creditworthiness and economic conditions when estimating the risk of bad debts can provide a more nuanced estimate, which helps companies identify potential problem areas and adjust their credit policies accordingly.

Note

Companies can choose the best method for their business needs and customer experience.

By estimating the allowance for doubtful accounts, companies can accurately reflect their financial position and ensure they have enough reserves to cover potential losses from uncollectible accounts.

What is the guiding standard for the estimation of this allowance?

Since it’s an estimate, thus it’s very important to have clear standards and models to estimate this figure.

As per IFRS 9, a company needs to estimate the “Expected Credit Losses” based on clear and objective evaluation criteria, which need to be documented by the management.

For what kind of accounts is the allowance to be made?

- Trade Receivables

- Employee Receivables

- Bills Receivables

Journal Entries for Allowance for Doubtful Accounts

Companies use a double-entry accounting system to record the allowance for doubtful accounts.

Let’s explain it with an example:

Suppose a company, ABC, estimates that 3% of its total sales will be uncollectible. For 2023, the company's total sales for the period were $100,000, and the estimated allowance for doubtful receivables would be $3,000 ($100,000 x 3%).

The company would then record a journal entry at the end of the accounting period that includes a $3,000 debit to the bad debt expense account and a $3,000 credit to the allowance for doubtful accounts.

| Debit | Credit | |

|---|---|---|

| Bad Debt | $3,000 | |

| Allowance for Dubious accounts | $3000 |

Later, if a customer fails to pay their account balance and the company deems the account uncollectible, they would record another journal entry to write off the bad debt. The customer owes $500, and the company writes off the debt as uncollectible.

The company would record a journal entry that includes a debit to the allowance for doubtful accounts for $500 and a credit to the accounts receivable account for $500.

| Debit | Credit | |

|---|---|---|

| Allowance for Dubious accounts | $500 | |

| Accounts Receivable | $500 |

Adjusting uncollectible accounts

Adjusting the estimated amount for uncollectible accounts is a significant process that businesses carry out to ensure the accuracy of their financial statements.

Changes in credit policies, the aging of accounts receivable, and economic conditions can influence this adjustment.

If a company alters its credit policies, such as extending credit to riskier customers, it would have to increase the estimated amount to cover the higher probability of uncollectible accounts.

Another factor in adjusting the estimated amount is the aging of accounts receivable. As accounts receivable age, they become less likely to be collected, so the estimate may need to be increased accordingly.

Economic conditions, such as high unemployment and interest rates, can also affect the estimated number of uncollectible accounts. As a result, businesses may need to increase their estimated amount to account for the higher risk.

Adjusting the estimated amount for uncollectible accounts is continuous to ensure that the financial statements accurately represent the company's financial position and reflect the level of risk from uncollectible accounts.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?