Prepaid Lease

An agreement to get the use of tangible assets, such as machinery, equipment, and real estate

What Is Prepaid Lease?

A prepaid lease (or operational lease) is an agreement to get the use of tangible assets, such as machinery, equipment, and real estate. The long-term usage of the assets is often a contractual requirement of the deal.

It is common practice to give the party leasing the asset (the lessee) the option to purchase the asset immediately following the conclusion of the lease period.

If an upfront rent payment is made, the lessor will normally get between 80% and 90% of the market value of the leased item. The prepaid lease can cut the lessor's present value tax burden by around 50% if the asset is planned for long-term usage.

A prepaid lease must meet some fundamental criteria. The lease period comes first. It shouldn't exceed 80% of the asset's remaining useful life. The residual value, which is the anticipated fair worth of the asset after the lease period, is the next prerequisite.

20% of the asset's original cost should be represented by the residual value. The opportunity to purchase is the final prerequisite. If the lessee decides to buy the asset, the price must be reasonable. There can be no choice for a cheap buy.

The lease will be regarded as a capital lease and will be handled differently for accounting reasons if these conditions are not satisfied.

Using a prepaid lease has many advantages. Lessors may get up to 80% to 90% of the asset's fair market value. Assets with a long usable life can have their worth maximized. Additionally, the rental revenue may be amortized over the lease duration.

While there are advantages, there are drawbacks as well. For instance, until the option to purchase is used after the lease, the lessee does not have legal ownership of the particular item.

The lessee may also wish to compare the values to discover how much the tax depreciation differs from the value of the rental deductions. The danger that the lessor would file for bankruptcy is another significant problem with prepaid leases.

- A prepaid lease involves long-term use of assets, with an option to purchase, typically requiring a reasonable purchase price.

- Lessors can receive 80-90% of the asset's value, amortize prepayments, deduct depreciation, and enjoy steady rental income.

- Prepaid leases are often cheaper, don't entail property ownership, and offer a purchase option.

- Lessees can't recognize the asset until the lease end, can't benefit from asset depreciation, and face bankruptcy risks.

- Prepaid rent is advanced payment for future benefit, while rent expenses affect income statements when incurred, impacting financial performance.

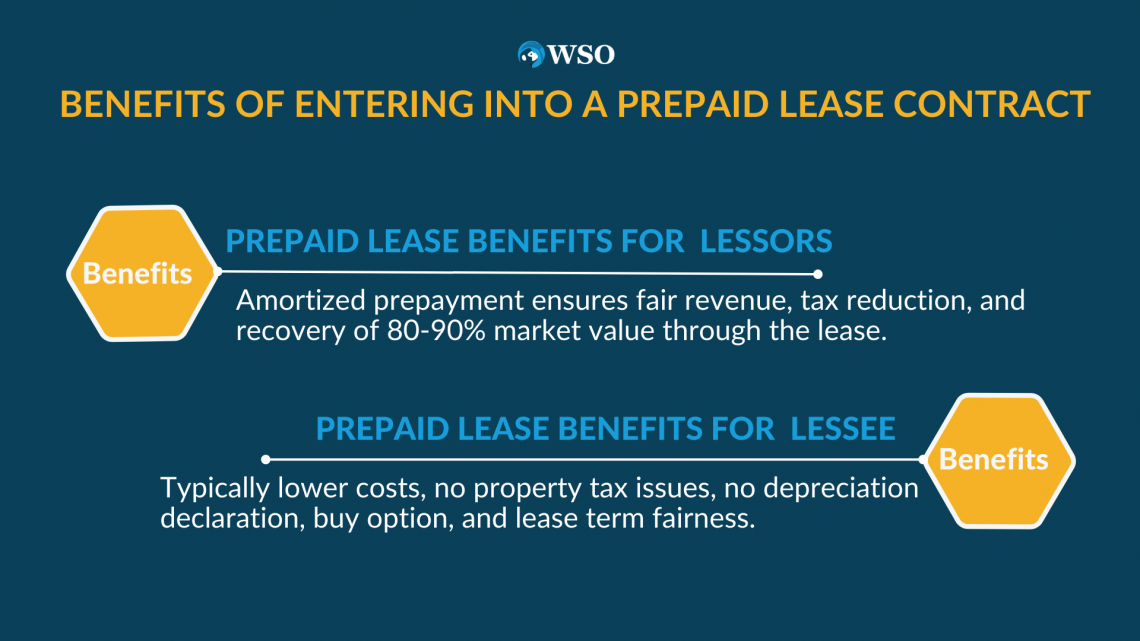

Benefits of entering into a prepaid lease contract

While it may look like a prepaid lease contract only benefits the lessor, it benefits both parties.

Here are some of the benefits of a prepaid lease:

For the lessor

-

The prepayment may be amortized by the lessor during the life of the lease. Both the revenue and the tax burden are spread fairly in this way.

-

Additionally, by doing it in this manner, the lessor's annual income can be sufficiently decreased to move into a reduced tax rate, resulting in additional money saved.

-

The lessor is allowed to deduct depreciation costs since they still own the rented property. This further lowers the lessor's taxable income, which also results in a smaller tax obligation.

-

The lessor can recover between 80% and 90% of the market value of the leased property through the lease alone. If the lessee chooses to exercise the purchase option, the proceeds represent an extra gain.

-

By amortizing the prepayment over the lease term, the lessor can have a consistent inflow of income instead of sporadic sales.

For the lessee

-

Typically, prepaid leases are less expensive than leases with periodic payments. This alone helps the lessee save money.

-

Property taxes won't be an issue for the lessee because ownership of the leased property isn't transferred to them.

-

The lessee won't be required to declare depreciation expenditure, which is also relevant to the earlier argument.

When a lease is prepaid, the lessee is given a buy option; if they choose to exercise it, they can eventually become the owner of the leased property.

Emphasis is placed on "remaining," which might be construed to mean the leased property's whole usable life. For instance, the useful life of a piece of equipment was predicted to be 5 years.

When you were allowed to lease it, it had been in use for three years. Its usable life is therefore limited to the next 2 years. The 2 years of remaining usable life will therefore be used as the 80 percent cutoff point for the lease term.

The smallest term shall be 1.6 years, or 1 year and 7.2 months.

Prepaid Lease Advantages

The advantages of Prepaid Lease are:

-

Only via leasing does the seller get between 80 and 90 percent of the asset's market worth. Another addition is the money he receives when he sells the item after the lease.

-

Throughout the lease, the lessor may amortize the tax obligation as income. In doing so, he will be able to pay less in taxes.

-

It enables the seller to keep the profitability of the firm steady. When a lease is paid in advance, the seller transforms a one-time gain into recurring rental revenue throughout the lease.

-

It may be advantageous for businesses for a variety of reasons. First off, it is clear that the seller can recoup between 80 and 90 percent of the asset's worth. As a result, the value of assets with a long lifespan may be maximized.

-

Similarly, prepaid lease agreements save the lessor a lot of money on taxes. Prepaid leasing agreements may therefore be quite valuable in assisting firms in maintaining their financial performance.

Prepaid Lease Disadvantages

The disadvantages of a Prepaid Lease includes:

-

Until the lease period is up and the lessee decides to purchase the asset, they cannot recognize the asset on his balance sheet. Even if they (the lessee) have made an advance payment, they don’t get to raise the asset column.

-

The lessee cannot profit tax-wise from the asset's depreciation. Since they are the owner of the asset for the duration of the lease, only the lessor should take asset depreciation into account.

-

The lease rent payment is the only thing the lessee may include as a cost on his income statement.

-

The lessee also faces the possibility of the lessor's insolvency. Even after paying the lease rent in full, upfront, the buyer may still run the danger of losing the leased item if the lessor declares bankruptcy and his assets are taken by lenders.

-

Prepaid lease agreements' biggest drawback is that they prevent the lessee from recording the item as an asset on the balance sheet. This lasts until the lease term expires and the lessee decides to purchase the asset.

-

Thus, even if the lessee has already made an advance payment, he cannot report it as an asset until the term's conclusion.

-

Second, the lessee would not be able to use depreciation to obtain the required tax savings.

-

It must thus be included as an expense on the income statement. Finally, if the lessor declares bankruptcy, the lessee is equally in danger of having their assets taken by creditors.

-

It must thus be included as an expense on the income statement. Finally, if the lessor declares bankruptcy, the lessee is equally in danger of having their assets taken by creditors.

-

Regardless of the terms of the contract between the lessor and the lessee, the lenders will have the right to repossess the asset if the lessor declares bankruptcy.

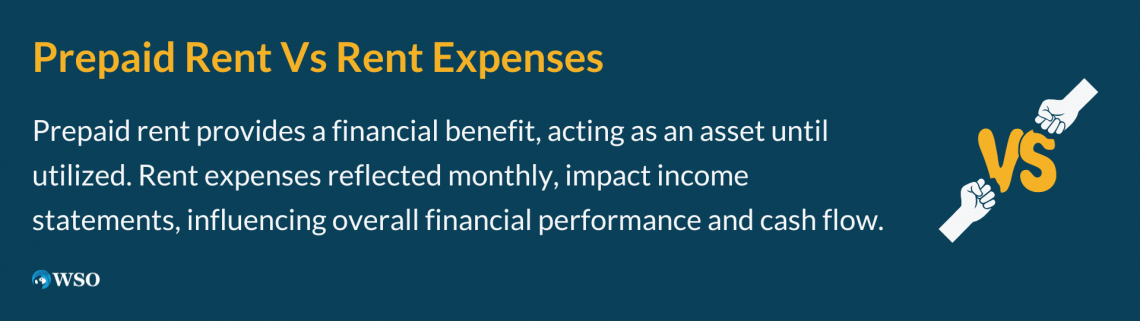

Prepaid Rent Vs Rent Expenses

When you lease instead of buying a property, you pledge to pay the landlord's rent, maintenance costs, and other costs. A rent expenditure is the amount of money you fork over each month or quarter.

Rent payment is reflected on your income statement in the month that the rent was for. Rent that has been paid in advance of the due date is known as prepaid rent. You will register it as an asset for the corporation since it is an advance payment for a future benefit.

Simply put, prepaid rent is any rent expenditure that you pay in advance of the due date. A rent expense is an amount that you are required to pay under a lease agreement. The situation becomes a little more challenging in accounting terms.

The selling, general, and administrative expenditures subcategory (SG&A), which appears on the income statement, typically includes rent charges.

Other SG&A costs include a variety of outlays, including wages, office supplies, insurance, and legal fees. Because a firm requires its real estate to function and generate revenue, rent expenditures are included as SG&A.

Manufacturing enterprises may handle their rent costs significantly differently. These businesses incorporate rent costs as part of production overhead considerably more frequently.

Because there would be no product without a plant, rent for manufacturing space is correlated with production.

Rent unrelated to production, such as office space, is billed to SG&A. But in the end, it doesn't matter which category the rent expenditure falls under because the overall result is the same.

What is the overall impact? You should debit the rent expenditure/SG&A account and credit the cash account whenever you incur a rent expense.

The SG&A costs are shown as revenue on the income statement and are grouped with other costs like depreciation and the cost of goods sold. Your gross profit is calculated as total revenues minus the cost of products sold.

Operating income is calculated as gross profit minus SG&A or operating expenditures. Operating income is a metric used to determine how much of your revenue will ultimately turn into a profit after accounting for factors like taxes.

Therefore, your operational income will be smaller the higher your rent expenditures. Rent costs directly affect the quantity of money in your company's vault.

You must be aware that a rent expenditure item will reflect the cost of occupying space during the time specified on the revenue statement - even if the rent was not paid within that period - to comprehend how prepaid rent fits into this analysis.

Therefore, if the rent for June is $5,000 and ABC Company is compiling its income statement for June, ABC would record a $5,000 rent charge. Regardless of whether it paid the rent in May or June, the corporation makes the same entry.

The corporation must record the amount of advance rent paid that has not yet been utilized to cope with this temporal discrepancy. This is done in the balance sheet's current assets column.

If ABC paid the rent in May, for instance, it would record the $5,000 advance as current assets until the expense was incurred. Prepaid rent is a benefit that the firm will eventually get but has not yet received for accounting reasons. It benefits the business.

Why Businesses Use Prepaid Rent

Prepaid rent is typically used by businesses out of need. The due date for the rent payment is one of the crucial provisions of a business contract. The annual rent is often payable in 12 equal installments on the date specified in the lease or four equal payments.

The lease will indicate the four rent payment dates, such as January 1, April 1, July 1, and October 1, if the rent is paid quarterly. These dates are simply the result of tradition; they don't have any special significance.

However, you'll discover that you'll always be required to pay rent one or three months in advance, creating a prepaid rent scenario.

Since there is a better chance that the mortgage payment will be covered by the rental income, banks and mortgage lenders typically require landlords to have the rent payments coming in before the mortgage payment is due for the same period.

Therefore, it will be difficult to locate a landlord who would allow you to pay your rent in arrears. In some situations, you may opt to pay more than one rental payment in advance.

For instance, in situations when there is intense competition, you can offer to pay a full year's rent in advance to get a specific apartment. You may even agree to pay a portion of the rent in advance for another incentive, like a 10% rent discount.

Each company will have a commercial driver who will place an envelope of money on the table.

Prepaid rent is the one thing you cannot utilize to increase your tax deductions. Most of the time, a firm will deduct an item in the same year it pays it. Therefore, you would claim the deductible in 2018 if you paid a $2,000 insurance premium.

Consider for a moment that you had a multi-year insurance agreement with a $2,000 yearly premium. If you want, you could pay the premiums for 2018 and 2019 at once and subtract the $4,000 payment from your 2018 taxes.

Depending on your tax status, this can be favorable. Sadly, the "deduct when you pay" principle does not apply to prepaid rent. If you pay $50,000 for a year's rent in June, you may only deduct seven months from your taxable income on December 31.

or Want to Sign up with your social account?