Variable Overhead Spending Variance

The metric which measures the difference between the actual and budgeted or expected overhead costs.

What is Variable Overhead Spending Variance?

The variable overhead spending variance is a measure used in cost accounting to assess the difference between the actual indirect variable costs incurred by a company and the expected or variable budgeted overhead costs for a particular period.

It helps evaluate the efficiency of a company's indirect variable cost management. Variable overhead costs are indirect manufacturing costs dependent on production activity, such as indirect labor, supplies, utilities, and maintenance.

The budgeted overhead represents the estimated costs a company expects to incur during a specific period, while the actual overhead represents the real costs.

Calculating this variance is essential for budgeting and benchmarking purposes, but it also provides upper-level management insight into how well certain department managers meet standards.

When interpreting their overhead variance, managers must understand why certain costs are up or down.

Overhead variable spending variance is the difference between the budgeted indirect variable costs and the actual overhead costs incurred. These numbers are calculated based on the standard rate and actual activity.

The result is a favorable variance if the actual costs are lower than expected. Vice versa, if the actual costs exceed the expected, it leads to an unfavorable variance. We will dive deeper into these terms and how they occur later in the article.

The variable overhead spending variance is significant in managerial accounting because it helps managers make informed decisions on costing activities. Managers will heavily monitor this variance over time to increase efficiency or profitability.

This variance also provides insight into whether a company’s budget is relevant enough if they find that their indirect variable costs consistently differ in significant values.

A consistent unfavorable variance can tell a manager something significantly wrong with the budget or that they have not done a good enough job controlling costs.

- The variable overhead spending variance measures the difference between the actual and budgeted or expected overhead costs. It includes indirect labor, supplies, utilities, and maintenance.

- The variance is calculated by subtracting the expected overhead costs (based on a standard rate and actual activity) from the overhead costs.

- Favorable Variance occurs when the actual variable overhead costs are less than the standard variable overhead costs. Indicates efficient control over variable overhead spending.

- Unfavorable Variance occurs when the actual variable overhead costs exceed the standard variable overhead costs. Indicates inefficiencies or higher-than-expected spending on variable overheads.

Components of Variable Overhead Spending Variance

The overhead spending variance consists of several components that help break down the factors contributing to the overall variance. These components are essential in understanding the calculation and application of the variance.

Here’s a breakdown of the components of Variable Overhead Spending:

- Standard Costs: Standard costs should be incurred under a facility's efficient operations.

- Standard costs include quantity and price standards, such as standard costs for direct material, direct labor, and the predetermined overhead rate.

- These Standard costs are a budgeting measure based on past performance and research-based studies.

- Variable Manufacturing costs: Manufacturing costs depend on the level of activity or amount of material used.

- Direct Materials: Variance consists of the direct material price variance and the direct materials usage variance.

- The direct materials price variance is the difference between the money you planned to spend on direct materials and the amount you did.

- Direct materials usage variance is the difference between the number of materials you plan on using for certain products and the amount used.

- Direct Labor: Variance consists of the direct labor rate variance and the direct labor efficiency variance.

- Direct labor rate variance is the difference between the actual cost of labor and the budgeted cost of labor.

- Direct labor efficiency variance assesses the difference in quantity between budgeted hours worked and actual hours worked.

- Direct Materials: Variance consists of the direct material price variance and the direct materials usage variance.

- Variable manufacturing overhead variance: Manufacturing overhead costs depend on the level of activity or amount of material used. Overhead is when a cost is indirect.

- Variable overhead rate variance is the difference between the actual and standard overhead rates times the activity level.

- Variable overhead efficiency variance is the difference between the time it takes for a job to be completed and the budgeted time.

Companies can calculate their overall overhead spending variance by considering both the variables of the overhead rate variance and the overhead efficiency variance.

The overhead rate and efficiency variance are necessary for how companies analyze costs and gain insights into different aspects of their overhead cost performance.

These components help identify areas for improvement, whether related to cost management, pricing, resource utilization, or productivity.

Understanding the Variable Overhead Spending Variance

In simple terms, the variable overhead spending variance is how much the overall variable overhead spending costs the company subtracted by the budgeted amount of money the company expected to spend on variable overhead.

Why do companies care about this measure? Companies care about calculating their overhead spending variance because it provides insight into how well they control costs, perform, and aid in decision-making.

By comparing their actual costs with their budgeted costs, they can identify areas they should cut costs or areas they have room to spend more on. Therefore, they can make informed decisions on how much they should or should not spend on overhead.

In general, costs can be linked back to a specific department. For example, a direct materials price variance would be the cause of the purchasing department since they are in charge of buying the products.

However, this is typically not the case for variable manufacturing overhead variances because they are linked to multiple managers and departments.

It is still helpful in performance evaluation by declaring the favorable or unfavorable variance. A favorable variance is generally good; a negative variance is generally a sign of overspending or over the budget.

Regardless, company executives look to this variance to decide pricing, production volume, resource allocation, and more. When the accountants know what factors contributed to favorable or unfavorable variance, they can decide to improve it.

One of the most important factors is the accountability and transparency aspect of managerial accounting.

These variances create accountability among employees to take responsibility for any unfavorable variances and find opportunities for improvement.

Note

Monitoring this variance within an organization allows for explanations of cost deviations and opportunities to refine their cost measures. Understanding this variance is crucial to enhancing cost practices and overall profitability.

Variable Overhead Spending Variable Formula

The variable manufacturing overhead variance formula calculates the difference between the actual manufacturing overhead costs and the standard manufacturing overhead costs.

The formula provides the basis for discerning how to interpret variable overhead and what it means. Understanding what the pieces of the formula mean individually, like standard variable OH rate and Actual DL hours, can help when looking at variances.

There are several different ways to calculate this formula, but the one provided below is the more typical format.

The formula is as follows:

Variable Manufacturing Overhead Spending Variance = Actual DL hour quantity * (Actual variable OH rate per hour - Standard Variable OH rate per hour)

Now, let's break down the formula into steps:

- Calculate the Actual overhead cost: This information can be obtained through accounting records or financial statements. If not, it can be calculated by dividing the total overhead costs by the direct labor hours.

- Calculate the Standard Overhead Cost: The budgeted rate is typically given to you through accounting records or financial statements.

- Calculate the Variable Manufacturing Overhead Variance: Subtract the standard overhead cost from the indirect variable cost and multiply by the direct labor hours used to calculate the variance. The resulting variance indicates the difference between the actual manufacturing overhead costs incurred and the expected or budgeted overhead costs.

The variance is unfavorable if the overhead cost exceeds the standard, indicating that costs exceed expectations. Conversely, if the actual cost is lower than the standard cost, the variance is favorable, indicating cost savings.

Note

Knowing how to interpret the favorable and unfavorable variances is essential to making investment decisions and deciding the cost-cutting measures of a company.

Stick around because we will dive deeper into an example and favorable and unfavorable variances towards the end of this article.

Variable Overhead Spending Variance Example

Interpreting and calculating variable overhead rate variance is the most helpful and valuable part of the variance.

By knowing how to do this, the variance is rendered functional. Let's work through an example: ABC Inc. produces widgets. ABC Inc. has a budget of $50,000 based on an expected activity level of 11,000 direct labor hours for a specific period.

However, at the end of the period, the company incurred indirect variable costs of $55,000 based on actual direct labor hours of 11,000.

To calculate the variable overhead spending variance, follow the same steps from the above section:

- Determine the Actual Variable Overhead Cost per unit: Divide the actual variable overhead cost by the actual direct labor hours incurred. The actual per unit variable overhead cost incurred by ABC Inc. is:

$55,000/11,000 =$5

- Determine the Standard Variable Overhead Cost per unit: Divide the standard variable overhead cost by the budgeted direct labor hours. The actual per unit variable overhead cost incurred by ABC Inc. is:

$50,000/11,000 =$4.54

- Calculate the Variable Overhead Spending Variance: Subtract the standard overhead variable cost per unit by the actual cost per unit, then multiply it by the direct labor hours incurred. The variable overhead spending variance is:

($4.54 - $5.00) * 11,000 = -5060

In this example, the overhead spending variance is ($5,060). The variance is unfavorable since the actual overhead cost exceeded the budgeted overhead cost.

This indicates that ABC Inc. incurred $5,060 more indirect variable costs than anticipated based on the budgeted activity level.

The unfavorable variance suggests that there might have been cost increases in any variable manufacturing overhead items.

This variance provides valuable information for management to investigate the reasons behind the higher costs and take appropriate actions to control overhead expenses in the future.

What causes an Unfavorable Variable Overhead Spending Variance?

An unfavorable variable manufacturing spending variance occurs when the actual manufacturing overhead costs exceed the budgeted or standard overhead variable costs.

A negative connotation is associated with unfavorable variances because it usually means that a purchasing manager is not doing their job correctly and overspending. However, this is only sometimes the case.

A knowledgeable purchasing manager should be able to discern the cost and benefits of creating an unfavorable variance and, therefore, do what's best for the company.

An example of an unfavorable variance creating more profitability for the company will be if a manager decides to either pay their indirect workers more or give out a more significant percentage of sales commission.

When workers have a greater monetary incentive to perform better, their work will typically reflect this. So if the sales worker knows they will gain more money if they sell more, that's typically the route they will take.

The indirect workers also affect your business more than you think. Customers may prefer to avoid visiting your store because it is dirty and unpleasant.

Now look at a janitor, for example. Let's say you pay them more, and they decide to clean the store much better. These customers will now be more likely to come to your store and buy your products.

The manager who decides to increase these costs would have weighed the extra revenue those workers will bring against the extra costs.

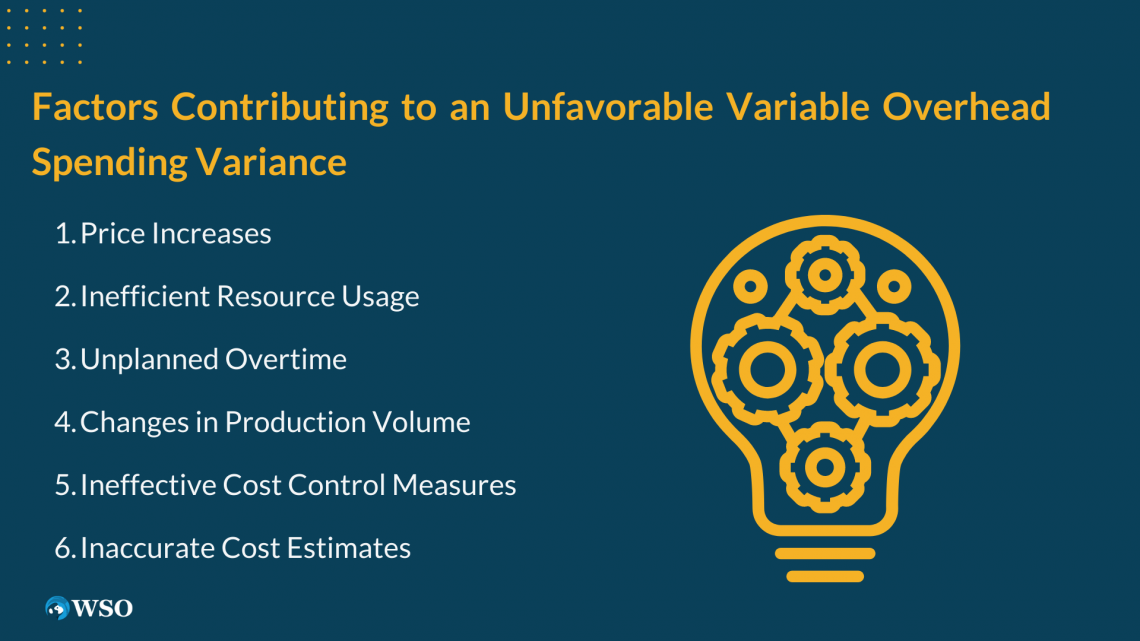

Factors Contributing to an Unfavorable Variable Overhead Spending Variance

There can be several factors that contribute to an unfavorable variance:

- Price Increases: If the prices of any overhead inputs increase during the production period, it can lead to higher variable manufacturing overhead costs. This can be due to factors like inflation or changes in supplier prices.

- Inefficient Resource Usage: Inefficient utilization of resources can result in higher variable manufacturing overhead costs. For example, if there are equipment breakdowns, it can lead to increased costs associated with indirect labor or equipment maintenance.

- Unplanned Overtime: If there is a need for additional direct labor hours beyond regular working hours, it may result in overtime payments or shift premiums.These extra labor costs can contribute to an unfavorable variance in variable manufacturing overhead spending.

- Changes in Production Volume: If the actual production volume is higher or lower than the budgeted level, it can lead to higher or lower overhead variable costs.

- Ineffective Cost Control Measures: Poor management, such as inadequate monitoring or ineffective cost control measures, can contribute to unfavorable variances. This may result from a failure to identify control cost overruns in the production process.

- Inaccurate Cost Estimates: If the initial cost estimates used for budgeting variable manufacturing overhead costs are inaccurate or do not reflect the actual cost drivers, it can result in unfavorable variances.

Businesses must analyze and understand the causes of unfavorable variable manufacturing spending variances.

Management can take corrective action and implement cost-saving measures by identifying the factors contributing to the variance.

What causes a Favorable Variable Overhead Spending Variance

A favorable variable manufacturing spending variance occurs when the actual manufacturing overhead costs are less than the budgeted or standard overhead variable costs.

A variance being favorable is usually a good thing. It provides insight into how well that specific department is cutting costs compared to what the company expected it would spend.

However, favorable variances only sometimes mean the company is doing something right. If a purchasing department decides to buy production supplies to manufacture their goods, this could be a significant cost-cutting measure.

But, it could also lead to lower quality goods that could break easily, tarnish a company's reputation, and turn customers away from this product.

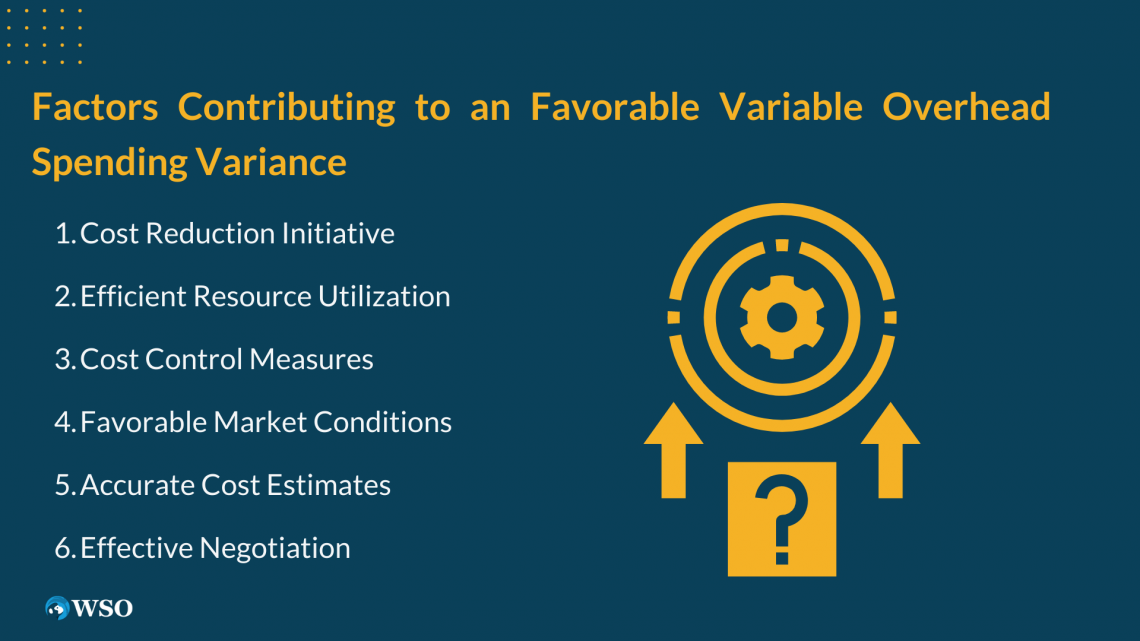

Factors Contributing to a Favorable Variable Overhead Spending Variance

Several factors can contribute to a favorable variance:

- Cost Reduction Initiatives: Implementing cost-saving measures and process improvements can lead to favorable variances. For example, finding more cost-effective suppliers or implementing efficiency measures can lower costs.

- Efficient Resource Utilization: Effective management of resources, such as minimizing downtime or improving labor productivity, can contribute to favorable variances.

- Cost Control Measures: Implementing strict cost control measures, such as regular monitoring, can help identify areas for improvement. Businesses can reduce unnecessary overhead expenses by actively managing and controlling costs.

- Favorable Market Conditions: External factors such as favorable market prices for inputs or lower costs of supplies with suppliers can contribute to favorable variances. These market conditions can result in lower variable manufacturing overhead costs.

- Accurate Cost Estimates: When the initial cost estimates used for budgeting overhead costs accurately reflect the cost drivers, it increases the likelihood of favorable variances. Accurate costing reduces the likelihood of cost overruns.

- Effective Negotiation: Skillful negotiation with suppliers can lower overhead costs.

By understanding the causes of favorable variable manufacturing spending variances, businesses can identify successful cost management practices, replicate them, and make informed decisions to optimize overhead costs.

Summary

Overall, the overhead spending variance is crucial to managerial and cost accounting. It contributes to how managers make costing decisions and the analysis of cost management practices.

Variable overhead costs are indirect manufacturing costs that fluctuate based on production activity. They are typically not directly tied to a specific product unit but necessary for the overall production process.

Some specific examples of overhead could be janitors or buildings that house multiple departments. These expenses aid in supporting the business but do not directly generate revenue.

The variance is calculated by subtracting the budgeted overhead costs from the actual variable manufacturing overhead costs.

A positive variance indicates a favorable variance, meaning that the actual costs were lower than the budgeted costs. An unfavorable variance indicated by a negative variance means that the actual costs exceeded the budgeted costs.

Analyzing the variable manufacturing overhead spending variance over time provides information for decision-making.

The variable manufacturing overhead spending variance is often analyzed with other variances, such as the manufacturing overhead efficiency variance and manufacturing overhead rate variance.

This manufacturing overhead spending variance helps businesses assess their performance in managing overhead costs and provides valuable insights to improve profitability in the manufacturing process.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?