Variable Rate Loans

Commonly referred to as adjustable-rate loans, the interest rate changes over time.

What are Variable Rate Loans?

Variable-rate loans, commonly referred to as adjustable-rate loans, let the interest rate change over time. This contrasts with loans with fixed interest rates, where the rate does not change during the loan's term.

Loans with variable interest rates may occasionally be helpful but also problematic, so borrowers should carefully weigh their choices before selecting this kind of loan.

One of the variable-rate loans' main benefits is that they frequently offer lower beginning interest rates than fixed-rate loans. As a result, they may be a captivating choice for borrowers looking to reduce their short-term interest costs.

Compared to fixed-rate loans, these loans may give borrowers more freedom. For example, some of these loans might not charge fees if the borrower makes extra payments or repays the loan early.

This will be advantageous for borrowers who desire to pay off their loans as fast as feasible or anticipate changes in their financial situation.

These loans can sometimes put borrowers in peril. Because of this, setting long-term goals and creating a budget for loan payments may be difficult for borrowers.

Another problem with these loans is the potential for interest rate limitations, which would cap the amount the interest rate can rise over a set period.

Although these limitations may offer some protection to borrowers, they could not be enough to stop an abrupt and considerable increase in interest rates.

Note

It’s important to note that some borrowers may be tempted to take out variable-rate loans simply because they offer lower initial interest rates. However, it’s crucial to remember that the interest rate on these loans can change rapidly, especially in a volatile market.

These loans result in borrowers choosing such loans and must be prepared for the possibility of an increase in their interest rates in the future.

Despite these concerns, variable-rate loans might still be a viable choice for some borrowers. For instance, borrowers who anticipate making short loan payments or relatively steady interest rates may find these loans to be wise.

These loans may also be a viable choice for borrowers prepared to assume some risk in exchange for possible cost savings.

When considering a variable rate loan, borrowers need to research and understand the terms and conditions of the loan.

For assistance in deciding if such a loan is the best option for their financial position, borrowers can also consult with a financial counselor or lender.

Note

It’s worth noting that the interest rate of a variable rate loan is usually tied to an index, such as the prime rate or the London Interbank Offered Rate. This means the loan's interest rate will change as the index changes.

A margin, i.e., a percentage added to the index rate, may also be used by some lenders to establish the loan's interest rate. Therefore, borrowers should be aware of the index and margin their lenders use and how they can affect the loan's interest rate.

Variable-rate loans can provide borrowers with flexibility and potential cost savings, but they also come with risks. Therefore, before selecting whether to take out such a loan, borrowers should carefully assess their unique financial condition and aspirations.

They may then decide wisely and select a loan that suits their requirements and financial situation.

- Variable-rate loans are loans in which the interest rate can fluctuate over time based on changes in an underlying benchmark or index, such as the prime rate, LIBOR, or the federal funds rate.

- The interest rate on a variable rate loan is composed of two parts: Base Rate, which is an established index rate that serves as the benchmark. And margin, which is a fixed percentage added to the base rate by the lender.

- Variable-rate loans are affected by broader economic conditions and monetary policy. Changes in interest rates by central banks, inflation, and economic growth can all impact the benchmark rates that variable-rate loans are tied to.

- Variable-rate loans often have interest rate caps that limit how much the rate can increase or decrease at each adjustment period and over the life of the loan. These caps protect borrowers from extreme fluctuations.

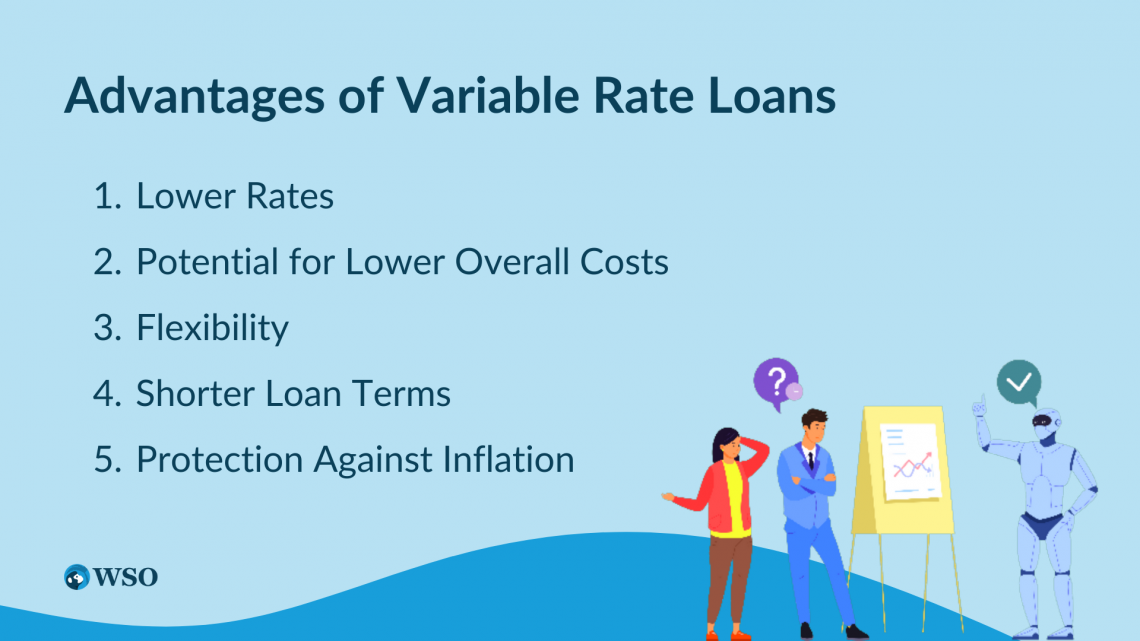

Advantages of Variable Rate Loans

Variable rate loans are a type of loan in which the interest rate charged changes over time, depending on changes in an underlying benchmark rate.

Variable-rate loans provide a variety of advantages that may make them a better alternative in some situations, even though fixed-rate loans are more usually chosen.

Here are some of the advantages of these loans:

1. Lower Rates

Adjustable interest rates sometimes have lower starting interest rates than fixed-rate loans. As a result, these loans may be more reasonable due to these reduced rates, particularly for borrowers on a tight budget or who want to pay as little each month as possible.

2. Potential for Lower Overall Costs

These may offer lower overall costs compared to fixed-rate loans. If interest rates decrease over time, the borrower's payments will also decrease. Conversely, if rates increase, the borrower's payments will also increase.

But if the borrower can make extra payments when rates are low, they can reduce their principal balance and save money in the long run.

3. Flexibility

Such loans offer greater flexibility than fixed-rate loans because borrowers can take advantage of changes in interest rates. For example, if interest rates decrease, borrowers can refinance or pay off their loans early to take advantage of lower rates.

Conversely, if rates increase, borrowers can make extra payments to pay off their loans faster and avoid paying more interest over time.

4. Shorter Loan Terms

These loans are often associated with shorter loan terms, which can help borrowers save money in interest charges.

Shorter loan terms also mean that borrowers can pay off their loans more quickly, which can be especially beneficial for borrowers who want to become debt-free as soon as possible.

5. Protection Against Inflation

These loans can protect borrowers against inflation, which can erode the value of a fixed-rate loan over time. As interest rates rise with inflation, borrowers will pay more in interest, but the value of their loan will remain stable in real terms.

Something to consider: While variable-rate loans offer several advantages, borrowers should carefully consider their circumstances before choosing this type of loan.

These loans may be subject to higher rates and payments over time, so it is always advisable to consult a financial advisor to determine which type of loan best suits one's needs.

These loans offer several advantages that may make them a better choice than fixed-rate loans in certain situations. For example, these loans offer lower initial rates, flexibility, shorter loan terms, and protection against inflation.

However, borrowers should be aware of the potential risks and consult a financial advisor before choosing this type of loan. With careful consideration and planning, variable-rate loans can be an excellent choice for many borrowers.

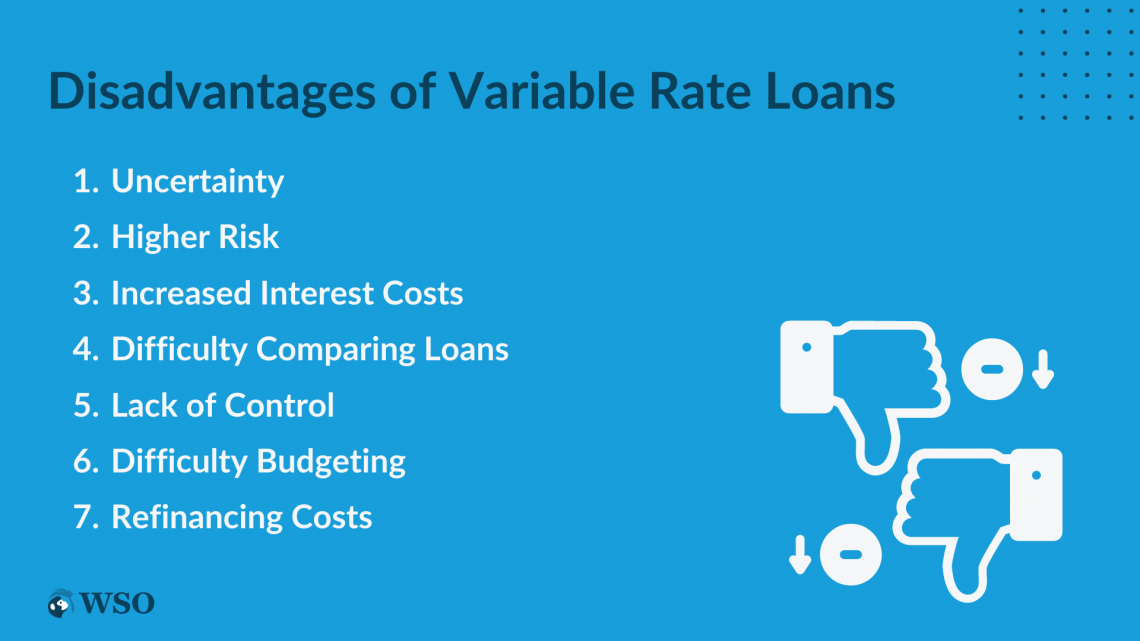

Disadvantages of Variable Rate Loans

A variable-rate loan, also known as an adjustable-rate loan, features an interest rate that changes over time. These loans have some significant drawbacks that consumers should be aware of. Some of the drawbacks are listed below.

1. Uncertainty

Borrowers may find it difficult to set aside money for a budget and develop long-term financial plans due to the unpredictability around variable-rate loan interest rates. Borrowers who take up such loans consent to an interest rate that might alter over the loan's term.

This suggests that the monthly sum might change based on how their interest rate changes. As a result, borrowers may find it challenging to save money for the future, plan for unforeseen needs, or simply make ends meet due to this volatility.

2. Higher Risk

These loans cost more than fixed-rate loans since the interest rate may change over time. As a result, borrowers may struggle to make timely payments if interest rates increase.

The likelihood of default rises when borrowers take out loans that are more expensive than they can pay or when their income is erratic.

3. Increased Interest Costs

When borrowers take out a variable-rate loan, they are typically attracted to the low introductory interest rate. However, these low rates are often just temporary and might rise sharply during the course of the loan.

Even slight interest rate rises can build up over time and cost the borrower much more money.

4. Difficulty Comparing Loans

Deciding whether a loan is the best bargain might be challenging because the interest rate on variable-rate loans is subject to vary.

Note

Borrowers might not completely comprehend all of the conditions and terms of the loan, such as interest rate ceilings and how frequently rates will be adjusted. Because of this ignorance, it may be challenging for borrowers to arrive at wise loan choices.

5. Lack of Control

Borrowers have little control over the interest rate on such a loan. This implies that their interest rate is subject to the market's and the lender's whims.

Even if borrowers are attentive to completing their loan payments on schedule, market movements may still cause their interest rates to rise. Due to this lack of control, borrowers may find preparing for their financial future stressful and challenging.

6. Difficulty Budgeting

Borrowers may find it difficult to successfully plan their budgets because the interest rate on a variable-rate loan is subject to alter over time. As a result, they could find it difficult to pay other bills on time or be obliged to cut other costs if the amount they pay each month rises.

This can be particularly challenging for debtors whose ability to pay their debts depends on steady cash flow or for those whose earnings are fixed.

7. Refinancing Costs

Borrowers might need to refinance their loans if interest rates drastically increase to lock in a reduced interest rate. However, refinancing can be pricey since customers may be responsible for fees and other costs related to the new loan.

Refinancing may not always be possible if the borrower's credit rating has declined after they take out the first loan.

While variable-rate loans have several significant drawbacks, they can be advantageous in some situations. However, before obtaining such a loan, borrowers should carefully assess their financial status and long-term objectives.

It's critical to comprehend the loan's terms and conditions, including interest rate limitations, how frequently rates are adjusted, and any prepayment penalties.

By doing this, borrowers may decide on their loans with knowledge and steer clear of any monetary trouble in the future.

Types of Variable Rate Loans

There are many different types and structures of variable-rate loans, each with special characteristics and advantages. Below are some types of variable-rate loans.

1. Adjustable Rate Mortgages

An adjustable-rate mortgage loan is one in which the interest rate varies over time. The interest rate is typically based on a financial index, such as the LIBOR or Treasury Bill rate, plus a margin determined by the lender.

ARMs are an appealing alternative for homeowners who intend to sell or remortgage before the interest rate changes since they frequently feature lower beginning interest rates than fixed-rate mortgages.

2. Home Equity Lines of Credit

Homeowners can borrow money using a home equity line of credit, a loan that permits them to do so. A HELOC's interest rate is normally determined by a financial index plus a margin and is subject to change over time.

HELOCs can be used for various purposes, such as home renovations, debt consolidation, or other large expenses.

3. Personal Lines of Credit

A personal line of credit enables borrowers to access money as needed up to a pre-authorized credit limit. Its interest rate is frequently variable, based on a financial index plus a margin, and subject to change over time.

Personal credit lines can be utilized for many things, including home repairs, medical fees, and other unforeseen needs.

4. Business Lines of Credit

A business line of credit is a loan that allows businesses to access funds as needed, up to a pre-approved credit limit. Its interest rate is frequently variable, determined by a financial index plus a margin, and subject to change over time.

Payroll, inventory purchases, and other company costs are just a few examples of the many uses for which business lines of credit may be put to use.

5. Student Loans

The interest rate is typically based on a financial index plus a margin and can be adjusted annually or at other intervals.

Borrowers who anticipate paying off their loans fast may find that variable-rate student loans are a suitable choice since they can benefit from reduced interest rates in the near future.

6. Credit Cards

Numerous credit cards feature variable interest rates, which may change over time. A credit card's interest rate is normally determined by a financial index plus a margin and is subject to change at any time.

Note

Carrying a balance on a credit card with a variable interest rate has the potential danger of interest charges quickly accumulating if the rate increases; therefore, cardholders should be aware of this risk.

It’s important for borrowers to carefully consider the loan type, as each type has its unique benefits and risks.

Borrowers should also pay close attention to the loan’s terms and conditions, including the interest rate structure, adjustment period, caps, and any fees associated with the loan.

Variable Rate Loans FAQs

A fixed-rate loan implies that payments from the borrower won't change over time. However, a borrower's payments may rise or fall over time due to the variable interest rate.

A variable-rate mortgage may start with a cheaper rate of interest than a fixed-rate loan, which is one advantage. In the near run, this can lower the cost of the loan. Furthermore, if interest rates fall gradually, the borrower's payments could too.

A variable-rate loan has the drawback that its interest rate may rise over time, increasing its overall cost. This can make it harder for the borrower to budget for their payments.

Borrowers who expect interest rates to decrease over time may benefit from this loan. Likewise, the initial reduced interest rate may be advantageous for borrowers who want to repay the loan soon.

It may not be advantageous for borrowers with little financial resources or who cannot afford to make higher payments should the interest rate rise. Furthermore, risk-averse borrowers might choose the security of a fixed-rate loan.

By comprehending the conditions of the loan and keeping an eye on interest rates over time, borrowers may control the risk associated with these loans. For example, if interest rates rise over their comfort level, they may also consider refinancing the loan into a fixed-rate loan.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?