Business Life Cycle

It depicts the progression of a firm from its early start-up phase

What Is A Business Life Cycle?

A business cycle depicts the progression of a firm from its early start-up phase to its maturity over a period of time.

Every firm goes through these phases, but the exact duration of the stage cannot be determined.

Each phase is identifiable by looking at certain variables like:

- Cash flows

- Profits

- Margins

- Dividends

Management strategies and priorities change along with the phases of business cycles.

While evaluating a company from an investment perspective, it is essential to identify at what stage of its business life cycle the company is in, as it will directly affect the forecast inputs.

-

Business cycle progresses through startup, growth, shake-out, maturity, and decline phases.

-

Each phase's characteristics, financials, and management strategies vary, impacting investment decisions

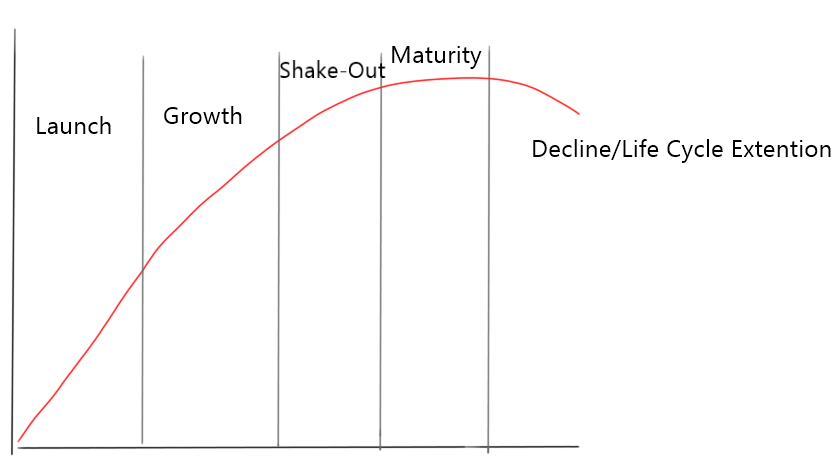

Phases of Business Life Cycle

The business cycle of any company can be categorized into five stages:

- Launch/Start-Up

- Growth

- Shake-out

- Maturity

- Decline

- Life-Cycle Extension

Each stage has its unique characteristics and challenges, which can be used to identify at what stage the company currently stands at.

The phases of the business life cycle are compared organizations to the life cycle of living organisms.

A vital feature of the organizational life cycle is that there is no specific duration allotted to each phase of the corporate life cycle, unlike the life cycles of organisms.

This comparison originated as early as the 1890s by the economist Alfred Marshall. Almost 60 years later, American economist Kenneth E. Boulding also suggested that organizations pass through a life cycle largely similar to organisms.

After this, there has been constant research and development in identifying and interpreting an organizational life cycle.

Understanding the organizational life cycles of a company can help us understand the management's thought process and make a better investment call.

Phase 1: Start-up/Launch

The start-up phase is the very initial stage of the firm. At this stage, the business can be in various positions financially.

NOTE

For startups, creating a Minimum Viable Product (MVP) is essential to test the product idea's viability and gather feedback from early customers. Further, while developing it the MVP cost can significantly impact the startup's overall budget and can play a major role in the startup's success or failure.

There are a few common factors in all the start-up phases. First, the businesses have very high expenses, and most expenses are focused on operating and customer acquisition, like advertising.

Another factor is that most of the capital raised is equity capital, as the companies are not creditworthy enough for bank loans or only eligible for high-yield debt.

The firm is not profitable at this stage, and the cash flow is negative.

There are a few ways to categorize the life cycle of the start-up/launch phase, as explained below.

Pre-Seed Funding Stage

The pre-seed funding round, also known as the pre-seed capital or pre-seed money, is the first instance of capital raising for a start-up. The amount required is relatively low as the business model is the only thing being developed.

At the pre-seed stage, the start-up has only raised non-institutional funding to fund its operations. At this stage, friends, family, and own equity is the only type of capital that has been infused into the firm.

Timing is essential at this stage. If the time taken is too much, the start-up will not survive in the long run.

The pace of the pre-seed funding depends on the start-up's initial expenses. At this stage, the company is still pre-revenue and focuses most of its cash on developing the product or idea.

The amount of pre-seed capital will decide the further goal of the firm. In the majority of the cases, the only investors in a pre-seed round are the founders themselves.

Seed Funding Stage

This is the first official stage of funding that the start-up raises. The term "seed funding" refers to sowing a seed to help grow the company. At this point, the company is too young to get debt funding.

At this point, start-ups usually dilute their equity in exchange for seed capital. Angel investors, Venture Capitalists (VCs), and equity-based crowdfunding are usually the types of investors funding this stage.

The seed-funding VC involves a higher level of risk than regular VC funding rounds as the company is still at a very early stage.

The proceeds from the seed round are used in:

- Product development

- Market research

- Testing

This is essentially the R&D phase: trying to find the product-market fit and fine-tuning the product to the inputs obtained through market research and product testing. Funding is also spent on fine-tuning the business model.

This stage is also usually pre-revenue but depends on the industry, sector, the vision of the founders, and, most importantly, the available funding.

Early Stage

At the early stage, the firm finally has a product that it can roll into the market.

In this stage, the operating costs drastically increase as new expenses like more salaries and advertising start to add up.

At this stage, a start-up also needs strategic investors who do not just contribute equity but also bring value to the organization, like connections and expertise which will help them expand.

Before this stage, all the funding was for:

- Operational

- Product development

- R&D expenses

Still, the start-ups will require funds to roll out products into the market and other allied activities at this stage.

This is the most crucial stage for a start-up as inflows other than funding start to come in. An early-stage start-up is no longer pre-revenue.

At this stage, the founders must be prepared for aggressive marketing and expansion, and if this stage is successful, then only the start-up will be able to function as a business.

It is rare for the company to be profitable at this stage.

Growth Stage

The growth stage is when there is a certain level of product recognition and brand value. At this stage, the start-up still requires funding raised at very high valuations.

The firm will still require outside funding to fule large-scale CAPEX.

Series B and Serie C funding are raised at this stage.

1. Series B Funding:

Series B round is done once the start-up has grown past its developmental stage. The product has some market visibility, and the company has no obligations to meet the market demand.

Series B funds are used to increase market presence and coverage through supply chains and marketing spending and to improve and expand the workforce.

2. Series C Funding:

At this stage, the start-up already has a successful product and established a user base with empirical growth.

The Series C funds are used for the expansion of the firm. Inorganic growth, like acquisitions, is usually funded by Series C capital. This is the most mature and capital-intensive stage for a start-up.

Usually, after this stage, the business stops being a start-up as they start showing profits and positive cash flows.

Phase 2: Growth

The growth phase of the business cycle is when companies start to become profitable, and small amounts of free cash flows begin to show.

The growth can be fielded by internal accruals or by raising debt. It all depends on the firm's profitability and the set capital structure. Usually, at this stage, it is a combination of both internal accruals and debt funding.

As the product/service starts to gain traction, the sales growth is very high and is usually followed by margin expansion. However, the growth in profits always lags behind the growth in sales.

It is counter-intuitive for a company in the growth stage to have a lot of free cash flow in hand, as most of the profits should be reinvested to fuel more growth.

The company balance sheet starts to look a little stronger but still has a lower net cash balance due to high investing cash outflows. As a result, the firm can appear weaker on the liquidity and current ratios.

Debt is usually used to fund significant CAPEX as they still need to spend a lot on advertising and hiring better talent.

In growth, stage management is entirely focused on fueling growth.

-

Example:

Royal Caribbean Cruises (RCL) is a luxury tourism company providing holiday cruise services and is in the growth stage of its business cycle.

RCL reinvests 100% of its profits, pays no dividends, and has a high level of debt; they have lower free cash flows.

Phase 3: Shake-out

The shake-out phase of the business cycle is also known as the consolidation phase. In the consolidation phase, the business becomes one of the market leaders and takes away market share from the smaller players.

At this stage, the free cash flow generation increases as the company become more efficient.

Debt levels start to go down significantly, but that entirely depends on the industry; e.g., a steel manufacturing company, even in its shake-out stage, will have a high debt because that is how the industry operates.

There still is a high level of sales growth, but the bottom line outgrows the top line. As the firm becomes more efficient, the margins start expanding while the expenses begin to decrease.

As more scale is achieved, brand recognition, an established efficient framework, and supply chains are established. The efficiency ratios like asset turns and inventory turnovers also improve drastically, making the balance sheet very strong.

As the company's balance sheet strengthens, the short-term and long-term debt gets better rated as they have more cash to service that debt.

If the company is publicly listed, multiple expansion also happens at this stage as a further effect of re-rating. Multiple expansion is when the valuation multiples like the Price-to-earnings (P/E), Price-to sales (P/S), and Price-to-book value (PB) start to swell up.

The multiples start to increase because buying volumes go up for higher-quality companies.

The profitability ratios like ROE and ROIC also start to grow, indicating the business is generating a higher return on its invested capital.

The dividend payout also starts to grow as the firm keeps generating more cash than its reinvestment needs.

The primary focus of the management at this stage is to fule growth but also, at the same time, focus on making its operations more efficient.

-

Example:

Amazon (AMZN) is an excellent example of a firm in its consolidation phase.

Even though Amazon is one of the biggest companies in the world, due to the sheer size and growth of the e-commerce industry and its new business vertical of Saas through AWS, Amazon is still in the consolidation phase of its life cycle.

Phase 4: Maturity

The maturity phase is very self-explanatory. Growth slows down, and the sales grow at a very steady level closer to the industry or economic growth rate.

The margins and free cash flow are at their highest. The major reason for the rapid growth in free cash flows is because the CAPEX stabilizes, which is a significant cash outflow.

The dividend payouts are at their highest, attracting many buyers. A mature firm usually trades at a premium multiple.

At this stage, the growth cannot come from organic elements, so inorganic expansion like M&A is the only way for the firm to grow at a higher rate than the industry or economy.

The majority of the capital allocation of a mature firm either happens in Mergers and Acquisitions or for enhancing shareholder value through buybacks and dividends.

Mature firms usually have low levels of debt, and the debt they have on their books is of the highest quality, usually AAA or AA rated.

The major focus of the management is to keep their market share stable while growing at a sustainable rate.

-

Example 1:

Sherwin-Williams (SHW) is the world's most extensive paints & coatings company. It is an excellent example of how a mature company fuels growth.

The majority of its capital is allocated towards buybacks and M&A, which is the only way for a mature firm to grow.

Please refer to the following article by Marcellus to understand how a firm grows in its mature vs. consolidation phase. Sherwin Willams vs. Asain Paints

-

Example 2:

Walmart (WMT) will serve as an alternative example to Sherwin-Williams. Walmart cannot fuel inorganic growth with M&A as its business model is not structured to support acquisitions.

The only way for Walmart to grow organically is if it chooses another geographical area with no presence or a lower level of market penetration.

Phase 5: Decline/Life Cycle Extension

This is the final phase of the business life cycle. At this stage, profits, cash flows, and sales of a business start declining as a company begins to lose its competitive advantage.

The company starts losing clients as its product becomes more commoditized or redundant due to changing trends.

If a company is listed at the decline stage, a PE rerating happens as it starts losing its competitive advantage and market share to its competitors.

The main focus of the management at this stage should be on changing the firm's positioning to adapt to the current scenario. Innovation is the critical element necessary for a life cycle extension to happen.

Innovation can usually come in several ways. It can be through product innovation, where the firm can either introduce a new product or change the existing product to fit the current market demand.

-

Example:

Nokia is right now at the decline stage of its business life cycle.

The reason for the decline of Nokia is that the management was unable to accept the changing environment; thus, the firm went into a decline phase, still struggling for life cycle extension.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?