Currency Swap Contract

A derivative agreement between two parties that calls for the exchange of principal amounts and interest payments.

What is a Currency Swap Contract?

A currency swap contract or a cross-currency swap is a contract between two entities that have to exchange the principal amount and the interest payments of a loan in a different currency at a pre-agreed price.

The ‘swap’ in currency swap contract here means to exchange something in return for something on similar lines. Here, to exchange currencies at predetermined terms and conditions listed under a contract entered by the two parties.

Under normal circumstances, global banks operate as mediators or facilitators in a currency swap deal. Still, they can also act like counterparties to hedge against their exposure to the global market, particularly foreign exchange risks.

Note

Usually, currency swap contracts are primarily to transfer principal amount payments. It is also sometimes used for only interest payments as well.

This financial instrument is deemed part of the derivatives class but is not used for speculation. Now, what is speculation? It is the transaction of a commodity or an asset with the hope that it will get more valuable in the near future.

Therefore, the swaps are employed to lock the fixed exchange rate and to hedge against the probable change in the foreign exchange rate fluctuations. The payable interest rates are very customizable. They could be fixed, variable, or both.

Such contracts were originally started to bypass exchange controls and governmental limitations implied on the purchase and sale of currencies.

Exchange controls are the government's restrictions on any trade with foreign exchanges. Developing countries usually levy these constraints to safeguard their currencies against speculation.

However, most developed economies have removed such constraints. As a result, swap contracts are now entered into to hedge long-term investments and alter the two parties' interest rate exposure.

Hence, companies borrow money from a bank in a country that may be offered at a favorable interest rate rather than from a bank where they currently operate.

- A currency swap contract is a financial agreement between two parties to exchange cash flows in different currencies over a specified period.

- Currency swaps are primarily used to hedge against currency risk or obtain cheaper foreign currency financing. They allow parties to access different currencies without directly engaging in the foreign exchange market.

- In a currency swap, each party agrees to exchange interest payments and principal amounts denominated in different currencies based on an agreed-upon exchange rate.

- Currency swaps are widely used for managing currency exposure in international trade, foreign currency funding, and maintaining exchange rate stability.

How Do Currency Swap Contracts Work?

Under such a contract, the parties involved agree on the terms and conditions prior to whether they will exchange the principal amount in the two currencies at the beginning of the transaction. The two principal amounts involved create an exchange rate.

To understand how exactly the swap contracts work, let us comprehend it through the help of an illustration.

There is Company X which is a US-based company and is planning to expand its business in India. It has been estimated that the company needs Rs. 25,00,00,000 for its expansion project in India.

In another country, say Europe, Company Y is planning its Merger and Acquisitions project with two companies, its new emerging competitors in the USA. For the same, it requires US $100 million.

Neither of the companies has enough funds residing with them to finance their projects. Therefore, they now seek to borrow funds in terms of foreign exchange through debt financing.

Company X and Company Y will prefer to borrow in their domestic currency, that is, dollars and euros, respectively, and enter into a currency swap contract.

These companies prefer to borrow in their domestic currencies because of the lower interest rates. Now let us see how these companies go along designing the contract between them.

Now Company X will acquire a US $100 million loan from Bank X at a fixed interest rate of 2.7%, and Company Y will borrow Rs. 25 crores from Bank Y with a floating interest rate of 12-month LIBOR. Thereon, the two companies enter into a swap agreement.

According to any swap contract, the two companies will have to exchange the principal amount of Rs. 25 crores and $100 million at the beginning of the contract. Moreover, the interest payments are to be exchanged annually.

Company X will pay Company Y interest payments according to the floating interest rate in rupees. Company Y will have to pay interest payments at the fixed interest rate of Company X in dollars.

On the contract's maturity date, the companies will exchange the principal amounts at Re.1= $2.5.

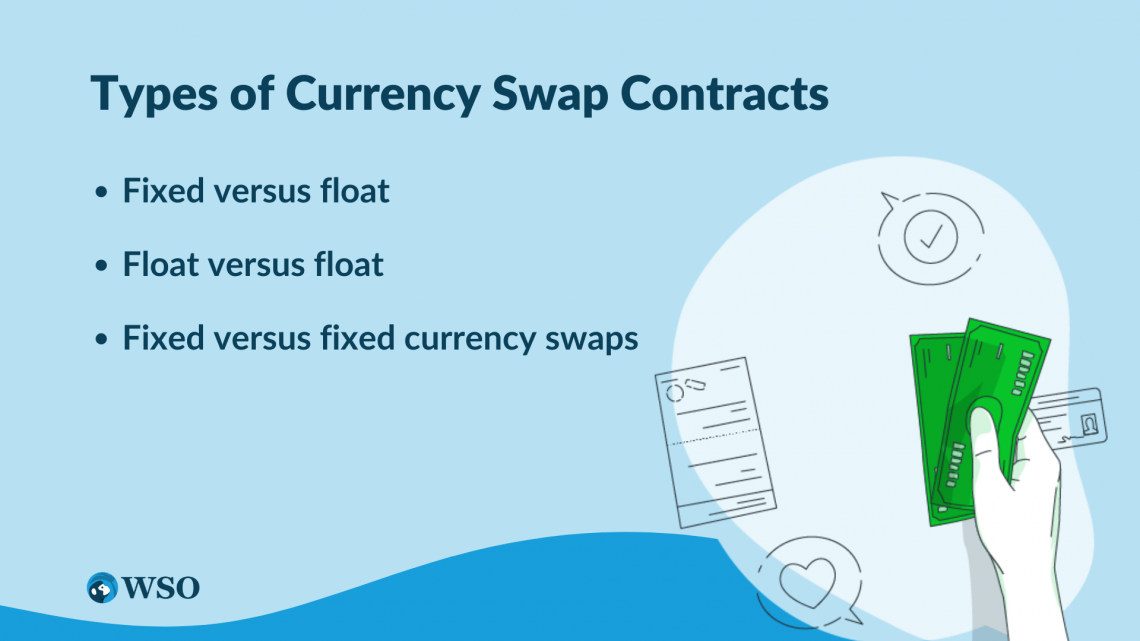

Types of Currency Swap Contracts

These kinds of contracts could be bifurcated into three major categories, pivoting on the legs involved in the contract. The most common ones are fixed versus float, float versus float, and fixed versus fixed currency swaps.

- The fixed versus float indicates that one of the two legs involved in the contract is the source of the fixed interest rate payments, whereas another leg is the one that makes payments at the floating interest rate.

- The second category, i.e., float versus float, also known as the basis swap, represents that both the legs make payments at the floating interest rate.

- The third category, fixed versus fixed, denotes that both contract legs involve payments made at fixed interest rates.

One example could be when a party is willing to convert the Indian rupee to Canadian dollars to pay a loan at a fixed interest rate in CAD can. Exchange that for a floating interest rate in INR. This can happen and vice versa as well.

These contracts have always been very suitable while dealing in the international market. Furthermore, its characteristic of redenomination makes it favorable for organizations to deal in different currencies worldwide.

Large corporations benefit from raising funds in one currency and saving funds in another.

Not only are these contracts beneficial, but they also carry minimal risk factors. Moreover, they are highly liquid, allowing the two parties involved in the contract to settle their agreement throughout the contract.

Conclusion

As discussed earlier, "swap" in the currency swap contract means "exchange." To recapitulate, it is a contractual agreement between the two legs of the contract that have agreed upon exchanging currencies under a few predetermined terms and conditions.

These contracts are also used by the central banks and the governments of a few countries to deal with short-term foreign exchange liquidity requirements and to keep a minimum level of foreign exchange sustained to dodge a Balance of Payments (BoP) crisis.

Since the terms of transactions are determined before the proceedings, the possible market risks are avoided in these contracts.

The currency risks occur due to the shifts in the value of the base currency in the agreement about the foreign currency in which the other leg of the contract has its assets and/or liabilities.

The swap contract for the currencies is priced through the LIBOR +/- spread. It accounts for the exchange risk between the two legs of the contract.

LIBOR or London Interbank Offer Rate refers to the internet rate banks in the UK charge for short-term loans by financial institutions. It is used as the benchmark for many securities' short-term interest rate prices, one being the currency swaps.

What is the spread? The spread refers to the credit risk based on the party's probability of paying back the borrowed debt at a particular interest rate.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?