Effective Annual Rate

The actual return on investment or payment on debt rate after considering the compounding periods.

What Is The Effective Annual Rate?

Effective Annual Rate is the actual return on investment or payment on debt rate after considering the compounding periods.

Banks attract investors or debtors to supply them with capital by sweetening the offer using a high interest rate. Similarly, creditors are attracted to banks offering a lower interest rate on their loans.

The interest rate offered in the terms is called the nominal rate. It is only the advertised or quoted rate. Most importantly, this rate does not include the compounding periods.

The Effective Annual Rate, or EAR, is the interest rate derived from the nominal rate and provides the actual yield earned after including compounding effects.

It accurately represents the return on investment by considering the effects of the nominal interest rate and the compounding frequency.

Compounding is the continuous process by which the interest is added back to the principal, forming a base for the new interest to be calculated.

- The Effective Annual Rate (EAR) is a financial metric that reflects the true annual interest rate on an investment or loan, accounting for the effects of compounding over a year.

- EAR is used to compare the annual interest rates of financial products with different compounding periods, providing a standardized measure to evaluate the true cost of borrowing or the true return on investment.

- For borrowers, EAR reveals the actual cost of a loan, enabling better comparison of loan offers. For investors, it indicates the true yield on investments, helping to assess the profitability of different investment options.

- More frequent compounding periods result in a higher EAR compared to the nominal rate, as interest is calculated and added to the principal more often, leading to "interest on interest."

Understanding the Effective Annual Rate

The Effective Annual Rate represents the interest rate when there is more than one compounding period yearly. Therefore, it can also be called the Effective Interest Rate (EIR), Annual Equivalent Rate (AER), or Annual Percentage Yield (APY).

EAR calculates the real interest rate for investments like fixed deposits and loans like mortgages when the interest is compounded multiple times.

It gives investors the exact interest rate depending on the number of payments. The compounding periods can be semi-annually, quarterly, monthly, weekly, daily, or continuous.

The nominal interest rate and compounding frequency are included in the calculation of the effective annual rate. However, it works independently of the principal, so the analysis does not consider it.

The nominal interest rate can also be known as the Annual Percentage Rate (APR). The APR is a specific rate that uses simple interest where the principal remains constant throughout the period.

Note

It is not helpful for loans or deposits that state that the interest is compounded.

An effective annual rate accurately represents the annual interest as it caters to the different compounding periods. It facilitates comparing loans with varying compounding periods by accurately estimating the yearly interest.

The EAR would be higher than the nominal rate for investments or loans with more than one compounding period. The difference between the effective annual rate and the nominal rate increases as the number of compounding periods increases.

How to Calculate the Effective Annual Rate?

The EAR can be calculated using the formula below.

Effective Annual Rate = (1 + (i/ n))n - 1

Where,

- i is the nominal interest rate or APR

- n is the number of compounding periods.

Continuous compounding is a type of compounding that happens for an infinite number of periods. When the interest is compounded continuously, it is calculated using the below formula.

Effective Annual Rate = ei - 1

The resultant EAR should be multiplied further with the principal to assess the interest to be paid or received aptly. One can also deduct the fees to refine the results further and make comparison easier.

The effective annual rate also increases when the number of compounding periods increases. Let us understand this better using an example. Suppose Bank A has been offering a fixed deposit with a 5% annual interest.

Here, the interest is compounded annually. We get the results below if we calculate the EAR at different compounding periods.

- Annual compounding = (1 + (5% / 1))1 - 1 = 5%

- Semi-annual compounding = (1 + (5% / 2))2 - 1 = 5.06%

- Quarterly compounding = (1 + (5% / 4))4 - 1 = 5.09%

- Monthly compounding = (1 + (5% / 12))12 - 1 = 5.116%

- Weekly compounding = (1 + (5% / 52))52 - 1 = 5.125%

- Daily compounding = (1 + (5% / 365))365 - 1 = 5.127%

- Continuous compounding = e5% - 1 = 5.127%

It can be observed that the interest rate is gradually increasing with a greater number of compounding periods.

How does the Compounding Period affect the Effective Annual Rate?

An investment could be paying interest, or interest payments could be due for a loan frequently in a year. The frequency could be either annually, semi-annually, quarterly, or monthly.

The compounding period is an essential factor in calculating the effective annual rate. This is because the EAR increases with the number of compounding periods. Therefore, when the interest compounds more frequently, the investor will earn or pay a higher interest rate on the investment or loan.

For example, a fixed deposit provides a compounded interest of 5% annually on a $1,000 principal.

In the first year, the interest earned is $50. This interest is added to the principal, bringing the new total to $1,050. The interest would be $52.5 for the second year, which is 5% on $1,050. Therefore, the new investment is increased to $1,102.5.

In this way, the investor earns interest on the reinvested interest previously accrued. It is a helpful tool to grow your investments exponentially.

Suppose the compounding period in the above example has increased semi-annually. The investor would earn $1050.625 in the first year and $1103.81 in the second.

- Y1 - 1,000 * (1 + (5% / 2))2 = $1,050.625

- Y2 - 1,050.625 * (1 + (5% / 2))2 = $1,103.81

Thus, the EAR for the semi-annually compounded deposit is 5.063%, higher than that for the annually compounded deposit.

How to compare using an Effective Annual Rate?

An increased EAR indicates that the investment produces higher returns or that the loan entails higher interest payments. In contrast, a lower EAR may suggest that the investment will provide lower returns or that the loan will require lower interest payments.

Investors will only choose a venture if it offers a high return on investment. Similarly, investors will be more inclined to select the venture whenever the EAR is higher.

Let us understand this better using a hypothetical situation. An investor can fund two different ventures, A and B, with a principal of $1,000. Venture A offers a compounded interest of 15% quarterly, while Venture B offers a 14% interest compounded monthly.

The effective annual rate would be calculated as follows:

- EAR (Venture A) = (1 + (15% / 4))4 - 1 = 15.865%

- EAR (Venture B) = (1 + (14% / 12))12 - 1 = 14.934%

After one year, the investor would get the below return on investments:

- Return (Venture A) = $1,000 * 15.865% = $158.65

- Return (Venture B) = $1,000 * 14.934% = $149.34

The investor would get higher returns with Venture A and must invest in it.

On the other hand, the borrower would likely choose a venture if the interest payments were lower. Therefore, it would be more appealing for the borrower to select that venture when the EAR is lower.

Let us assume, for example, that a borrower is looking for funds amounting to $1,000. Loan A offers an interest of 10% compounded quarterly, while loan B offers a 12% interest compounded monthly.

The EAR would be calculated as follows:

- EAR (Loan A) = (1 + (10% / 4))4 - 1 = 10.381%

- EAR (Loan B) = (1 + (12% / 12))12 - 1 = 12.683%

After one year, the borrower would have to pay the interest calculated below:

- Return (Loan A) = $1,000 * 10.381% = $103.81

- Return (Loan B) = $1,000 * 12.683% = $126.83

The borrower would select Loan A as they have to pay lower interest for the loan term.

Uses of Effective Annual Rate

Calculating the effective annual rate increases the accuracy of payment plans and investment opportunities, ultimately enhancing financial decision-making. The EAR has benefits for borrowers and investors.

Loan Borrowers

It is common for banks to quote only the APR on loans with compounded interest. Therefore, the borrowers will be enticed to select the loan plan as the APR is lower than the EAR.

The borrower could estimate the total bank loan cost with this tool's assistance. In addition, borrowers can determine their loan's exact fees and future cash flow amount.

Borrowers can decide between two or more loans by selecting the lowest annual interest rate. They could obtain a loan at a low-interest rate and with convenient payment terms.

Investment Lenders

Lenders service their capital with investment opportunities that attract a high rate of return. For example, banks offer investments with compounded interest by stating the EAR.

Since it provides a more accurate representation of the annual return, the investor is influenced to fund the opportunities with a high investment growth rate.

Investors can easily understand the effects of different interest rates on their investments. In addition, the estimates help investors compare investments like deposits, saving accounts, or bonds.

If an investor is at a crossroads between two investments with different compounding periods, it is always advisable to calculate the EAR. Generally, investments with more frequent compounding periods are better as they allow the interest to grow over time.

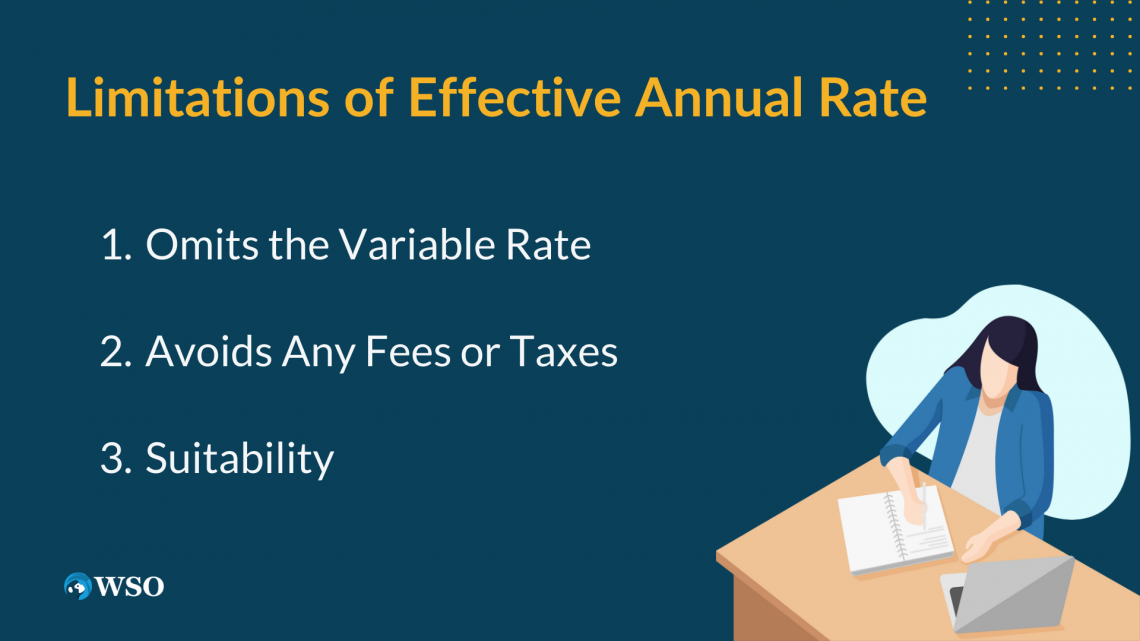

Limitations of Effective Annual Rate

The benefits of this tool are plenty; however, it has disadvantages.

Omits the Variable Rate

Loans or investments could be taken with a fixed or floating (variable) rate. The floating rate is the interest rate that changes based on market fluctuations. The most common type of variable rate is the London Interbank Bank Offer Rate (LIBOR).

Calculating the EAR assumes that the interest rate is fixed and would be consistently applied for the entire term of the loan or investment. However, whenever the interest rate changes, it heavily impacts the returns and payments. Thus, the EAR is not a good tool for loans or investments assuming a variable rate.

Avoids Any Fees or Taxes

The impact of transaction fees is not considered while calculating the EAR. The other costs include any service or account maintenance fees.

Investors need to understand and account for such fees to reduce their returns. For borrowers, it increases their cash flow payments. A disadvantage can significantly impact the financial decision when comparing loans and investments.

Note

The EAR should not be the sole consideration for investors or borrowers when evaluating an offer. Sometimes, a loan may offer a lower EAR but have high borrowing costs. Additionally, taxes are not considered while evaluating the EAR. Taxes, similar to fees, reduce the returns on investments and increase borrowing costs.

Suitability

Estimating an effective annual rate when multiple compounding periods exist in a year is valuable. The EAR is the same as the nominal rate when interest is compounded once a year. When the compounding period crosses once a year, it is practical to calculate the EAR.

It is not suitable for short-term investments as it is not compounded often. At the same time, it would be appropriate for long-term investments as compounding has a more significant impact on the value of the investment.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?