Original Issue Discount (OID)

The original issue discount is the difference between the face value and the issue price of a bond.

What Is An Original Issue Discount (OID)?

Original issue discount (OID) refers to the difference between a bond’s par value (or “face value”) and its issued price.

Face value is the amount the borrower will pay at the bond’s maturity, in addition to regular interest payments throughout the bond’s life. The issue price is the price at which the bond is sold initially.

An original issue discount occurs when a borrower issues a bond at a price lower than its face value (also known as par value or redemption price).

This discount is the difference between the bond's face value and its issue price. For example, if a bond has a face value of $1,000 but is issued for $900, there is a 10% discount. Any bond can be sold at a discount, meaning the bondholder may sell it below its face value to increase yield and attract buyers.

"Original issue" discounts specifically refer to debt securities initially issued at a discount from their face value.

- The original issue discount is the difference between the face value and the issue price of a bond.

- An original issue discount increases a bond's yield, making it more attractive to investors.

- Original issue discounts happen on the primary market, whilst discount bonds are exchanged on the secondary market.

- Companies use original issue discounts as tools to manage interest payments, a crucial factor in cash flow management.

How an Original Issue Discount (OID) Works

In a typical bond sale, the issuer periodically pays an interest rate, called a coupon, to the buyer for the duration of the bond. When the bond reaches maturity, the buyer receives the face value paid for the bond on top of the coupon payments.

However, with an Original Issue Discount (OID) bond, the bond is issued at a price lower than its face (par) value, often with little or no coupon.

The difference between the purchase price and the par value represents the investor’s earnings, which are treated as interest income. When the bond matures, the investor receives the full par value, resulting in a return that reflects both the implied interest from the discount and any stated coupon payments.

OID is common in zero-coupon bonds and certain corporate or Treasury instruments.

Formula and Calculation of OID

The OID is the difference between the par value of the bond and the actual price at which it was issued.

OID = Redemption Price - Issuance Price

Where

Redemption Price: The face or par value of the bond

Issuance Price: The price at which the bond was initially sold

Example of How to Calculate OID

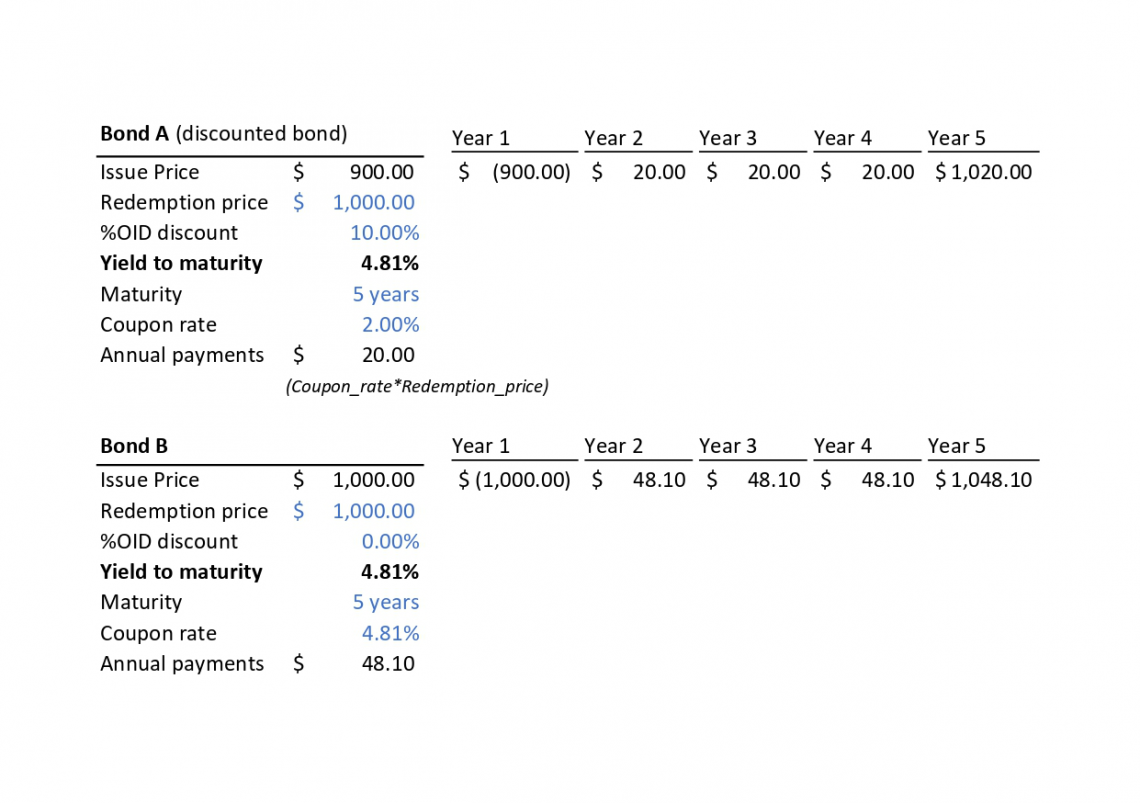

A company issues 10 bonds at a $100 face value for a total redemption price of $1,000, but is willing to accept only $900 in capital, creating an OID of $100 (1,000 - 900) (or a 10% discount). At maturity, the company will pay back the investor $1,000.

All else being equal, a discount can create an equivalent yield for two bonds with different coupon rates, thus making it (in theory) equally as attractive to an investor:

In this example, Bond B has a higher coupon rate, which increases monthly returns. However, Bond A uses a discount of 10%, which increases the yield (IRR of bond cash flows).

Note

In practice, OIDs tend to be between 1-3%, and companies issue them alongside a strong plan for the future that will generate clear returns.

Why Issue a Discounted Bond?

So, why would a bond issuer (a company or government) willingly accept less money while having to repay the full par value amount?

Investors generally try to maximize their yield in the bond market, where companies and governments issue bonds.

Therefore, when a company or government cannot offer a coupon rate comparable to current market rates for similar bonds, it attracts investors by lowering the purchase price of its bonds, thus increasing yield.

Typically, discount bonds fall into the below-investment-grade category because their issuers have higher default rates, greater risk, and less stable operating performance.

Note

If we consider the bond coupon rate from the issuing company’s perspective, it represents an interest payment.

Managing interest payments is crucial as it often represents a large part of the company’s cash outflow (especially for Private Equity firms); therefore, issuing bonds at lower coupon rates frees up cash. This can be worth receiving less money upfront from some highly leveraged companies.

Conversely, companies are cautious about issuing bonds at high interest rates due to the burden of high-interest payments.

If a company anticipates that bond market interest rates will decrease but needs funds immediately, it can issue bonds at a discount (with a low interest rate) in the short term. Later, the company can issue lower-rate bonds, thereby minimizing its overall interest payments.

OIDS and Bonds Issued at a Discount

Bonds issued at a discount are debt securities sold in the bond market, also known as the fixed-income market. These bonds are initially offered at a price lower than their face value to attract investors. Here’s a closer look at the process and implications.

Primary Bond Market

Leveraged finance teams guide corporations and governments in raising debt to fund projects. Investment bankers may advise clients to issue debt at a discount to face value, based on current market rates, market conditions, and the company’s financials, to incite investors to buy the bond.

This means that retail investors are not typically invited to invest in bonds with OID, as they are often part of large transactions involving several banks and institutional investors, led by a “bookrunner” bank.

Secondary Bond Market

Investors trade bonds to build their portfolios. When a bond is sold below (or above) its face value in this market, it is called a "discount” (or “premium”) bond.

It is essential to distinguish between discount bonds and original issue discounts, as the latter are reported on the issuer’s financial statements and provide information about its credit rating and solvency.

Retail investors can access these bonds on the secondary market as discount bonds, but remember: discount does not mean bargain, as these bonds do come with higher default risks.

Real-World Example of an OID

An OID occurred in March 2024 when REC Ltd (Rural Electrification Corporation), an Indian civil engineering company, issued $601 million in bonds at an OID of around 20%.

REC is a state-run investment vehicle that provides financing for energy-related infrastructure projects to state-owned and private companies. 20% is considered a “deep discount” as OIDs rarely go above 3%.

It raised bonds to continue its usual activity (financing infrastructure projects). An interesting point is that the Indian government (regional authorities) granted a tax benefit to bondholders who would buy into REC’s issue.

Bondholders will not pay any interest on the discount value (see below on tax considerations of OIDs). This further incentivizes investors and is part of the Indian government's strategy to attract investors to develop the country.

OIDs and Zero-Coupon Bonds

If you are familiar with zero-coupon bonds, you could be asking yourself what the difference is, and in some cases, there isn’t any.

Indeed, zero-coupon bonds are bonds that don’t pay a coupon to investors, who make returns from the difference between the redemption and issue prices.

Example

An Investor buys a Zero-coupon bond for $98 and receives $100 at maturity.

So there are two types of bonds with OIDs:

- Zero-Coupon Bonds

- Coupon Bonds

Zero-coupon bonds tend to have deeper discounts as they don’t pay a coupon and tend to have long maturities.

OIDs and yield

As we’ve discovered, discounts correlate with yields. The higher the discount, the higher the yield.

Yield is the internal rate of return an investor earns by holding a bond to maturity, and it is the main metric that bond market investors consider before making an investment decision. In practice:

- Investors will look at a corporate bond index such as the S&P 500 Bond Index, choosing to invest in bonds with yields equal to or above the relevant maturity yield.

- Companies will look at the same index and try to match the average yield on their issued bonds. This can be done by creating an OID, for example.

Famous bond indexes include:

- Emerging market bonds: JP Morgan Emerging Markets Bond Index

- High-yield bonds: S&P US issued High-Yield Corporate Bond Index

- Leveraged Loans: S&P Leveraged Loan Index

- Aggregate indexes: Bloomberg US Agg Total Return Value Unhedged USD

US bond investors closely watch the Bloomberg US Agg index as it gives the yield of the overall bond market. It takes into account U.S. Treasury bills, investment-grade bonds, fixed-rate non-taxable bonds, and others to provide a view of the safest bonds on the market.

Generally, if a bond’s yield is above this rate, it tends to be riskier, whilst if it is below, it is not on par with the market average.

OID in the Three Financial Statements

As OIDs happen on the primary market, the company raising capital will have to account for them.

They are amortized throughout the borrowing term (from issuance to redemption) and treated as a form of taxable interest. It is treated under the U.S. GAAP as non-cash interest, much like financing fees.

Balance Sheet

The bond is recognized at face value in a “Bonds Payable” account. The Discount (or Premium) is Debited (or Credited) in a Bond Discount (or Premium) account. On the Assets side, initially, the cash account increases (debited) by the discount amount.

Income statement

Annual OID amortization expense is recognized for each period. Usually, it is consolidated with the “interest expense” line item.

Like most amortization expenses, it reduces net income and pre-tax income (amortization is tax-deductible in most cases). Using the “Effective Interest rate” method, the interest expense for each period is:

Interest expense = Market rate of interest * Carrying value of bond

- Market rate of interest: The average yield of similar bonds or 10-year government bonds at the time of issuance. The effective interest method uses this as a fixed interest rate.

- Carrying value of bond: The Carrying value of the discounted bond is the discounted value with the period’s OID amortization added back. The market interest rate is fixed and determined at the time of bond issuance.

Cash flow statement

OID amortization is added to the cash from operations section as it is a non-cash expense. It increases the ending cash balance. The cash linked to the bond's issuing and repayment is part of the “cash from financing” section.

Example

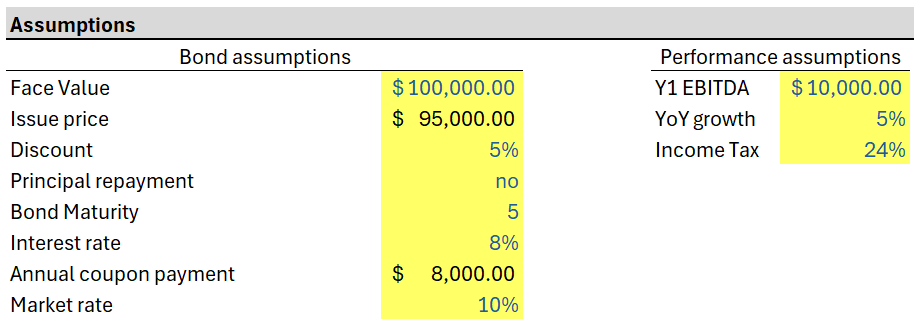

On January 1, Company ABC issued a $100,000 bond at an 8% discount with a maturity of 5 years and no principal repayment.

OID calculation

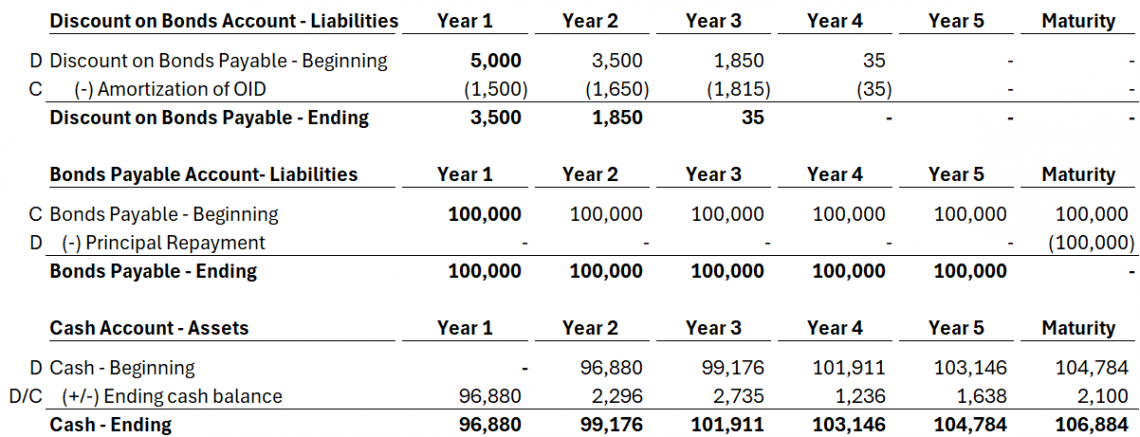

Balance Sheet: (“D” and “C” stand for Debit and Credit)

Note

The face value (“Bonds Payable” account) will be for the full amount of the bond and will never be affected by discounts, premiums, or issuance fees. In our simple model, we assume the initial cash balance in Year 1 is $ 0. It is then debited or credited by the ending cash balance from the cash flow statement.)

Income Statement

Remember,

Bond interest expense = market rate of interest at issuance * carrying value

Since the carrying value increases each period and the market rate is fixed (market at the date of issuance), the interest expense increases each period. Still, it remains the same percentage of the Carrying bond value.

From Bond interest expense, we add the coupon payment (8% * 100,000 = 8000 annually) to get to “Amortization of OID” in the Balance sheet.)

Cash-Flow Statement

Note

The “Amortization of OID” gets added back to cash from operations as a “Non-Cash Expense”.

OIDs are rarely included in financial modeling tests, and even if you omit an OID, it won’t make a big difference in the free cash flow (used in the DCF). Therefore, it is important to understand and know what an OID is, but no need to obsess over how to model it.

OIDs and Tax Liability

As we’ve seen previously, OIDs are considered an interest expense in the financial statements and are taxed as such.

The discount amount is treated as interest income, similar to a loan interest payment. However, by nature, OIDs are not a cash inflow to the bondholder, hence the term “phantom” tax.

Bondholder’s perspective

According to U.S. GAAP, OIDs are considered a form of interest (“Total interest expense” line above). This means that bondholders have to pay taxes on interest as it accrues every year.

In our previous example, the bondholder receives $2 in non-cash interest, which he must report as income in his tax filings. Each year, the issuing company sends out a Form-1099 OID if the interest is accrued at $10 or more.

However, some bonds can be issued tax-free in exceptional circumstances as a way for the government to subsidize a company or industry.

Therefore, it is essential to consult a tax professional before purchasing a bond.

Company’s perspective

An OID allows the issuing company to increase its interest expense throughout the period of the bond’s life without an actual cash outflow. Interest expenses are tax-deductible, so OIDs decrease the pre-tax income, and it is commonly known as a “tax shield”.

However, unless the OID is “deep,” i.e, over 10%, the tax break will be relatively small and thus will not make a major difference in the company’s final tax amount.

Original Issue Discount FAQs

Form 1099-OID is for bondholders who receive a $10 or more discount on their purchase of a bond lasting over a year. The OID is reported as taxable interest income on Schedule B, Line 2, or Form 1040. Boxes 1 through 11 of Form 1099 disclose various information and cases.

Essentially, as an OID bondholder, you pay taxes on interest that you don’t receive in cash payments.

However, the IRS and different government jurisdictions can create tax benefits for discounted bonds by canceling the need for taxable interest. This can be an exceptional benefit for an issue, an industry-wide benefit, or a periodic benefit.

Historically, the US oil industry has benefited from tax-free bonds. Today, tax benefits on credits are used to incentivize the purchase of “green bonds”.

A zero-coupon bond does not pay any coupon interest (annual or semiannual interest payments); hence, the only return an investor gets is from the discount to face value. Hence, a zero-coupon bond, at issuance, is an example of an OID.

However, bonds that pay a coupon can still be issued at a discount (to increase yield). So, a zero-coupon bond is a type of OID.

Issuing a bond at a discount to face value, all else being equal, increases its yield. Companies that need to raise capital through the bond market have two levers to impact yield: the coupon rate and the OID percentage.

During high-interest-rate periods or for companies in tight cash-flow situations, matching the market's coupon rate can be a strain. Hence, issuing bonds at a discount keeps them competitive for investors.

Market discount and OID work in the same way: the bond is sold at a discount to face value. The difference lies in the market in which they are sold.

Original Issue Discounts occur in the primary market, where they are issued directly to bond investors by companies seeking to raise capital. Market discounts happen when bond investors exchange bonds amongst themselves on the secondary market.

As a retail investor, you typically do not have access to the primary bond market, as large transactions are typically conducted there. The “bookrunner” bank, the financial institution brokering the deal, is looking to secure funding for its client (the issuing company).

Hence, the bank is seeking to sell a significant portion of the debt to a select group of well-established investors.

However, retail investors can buy bonds at a market discount on the secondary market. However, beware: discounts do not necessarily mean bargains, as discounted bonds typically carry considerably more risk.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?