Solvency Ratio

A financial measurement is used to assess a company's capacity to satisfy long-term obligations.

What Is a Solvency Ratio?

Solvency ratios, often known as leverage ratios, are financial measurements used to assess a company's capacity to satisfy long-term obligations.

These ratios show if a company has sufficient assets to cover its long-term liabilities, such as loans, bonds, and other debt, with terms longer than one year.

These ratios are critical for investors because they reveal a company's capacity to satisfy long-term financial commitments and help investors estimate the financial risk associated with a particular investment.

For instance, consider a firm with an exceptionally high D/E (debt-to-equity) ratio. An informed investor would avoid investing in such a company since it might signal that the company is overly leveraged and has taken on large debt compared to its equity.

Furthermore, a company's solvency also affects its capability to generate future gains and pay dividends. If it's unfit to pay its long-term fiscal obligations, a company may be impelled to reorganize or even file for bankruptcy, which might mean losses for investors.

Leverage ratios are also essential for creditors. Creditors use leverage ratios to analyze a firm's creditworthiness and estimate the amount of risk involved with lending money to a borrowing company since these ratios give insight into the firm's level of debt and capacity to repay its obligations.

A high D/E ratio, for example, may suggest that a firm has taken on too much debt, increasing the danger of default on its financial commitments. This might result in the company's credit rating being reduced and its borrowing expenses increasing in the future.

The leverage ratios give useful information to creditors that may help them make loan decisions and manage risk.

- The solvency ratio is a financial metric used to assess a company's ability to meet its long-term debt obligations. It measures the proportion of a company's assets that are financed by equity rather than debt.

- This ratio indicates the extent to which a company's assets cover its long-term liabilities, providing insight into its financial stability and risk of insolvency.

- A higher solvency ratio indicates a greater proportion of equity relative to debt, suggesting a stronger financial position and a lower risk of insolvency.

- Investors and creditors use the solvency ratio to evaluate a company's financial health and risk profile before making investment or lending decisions.

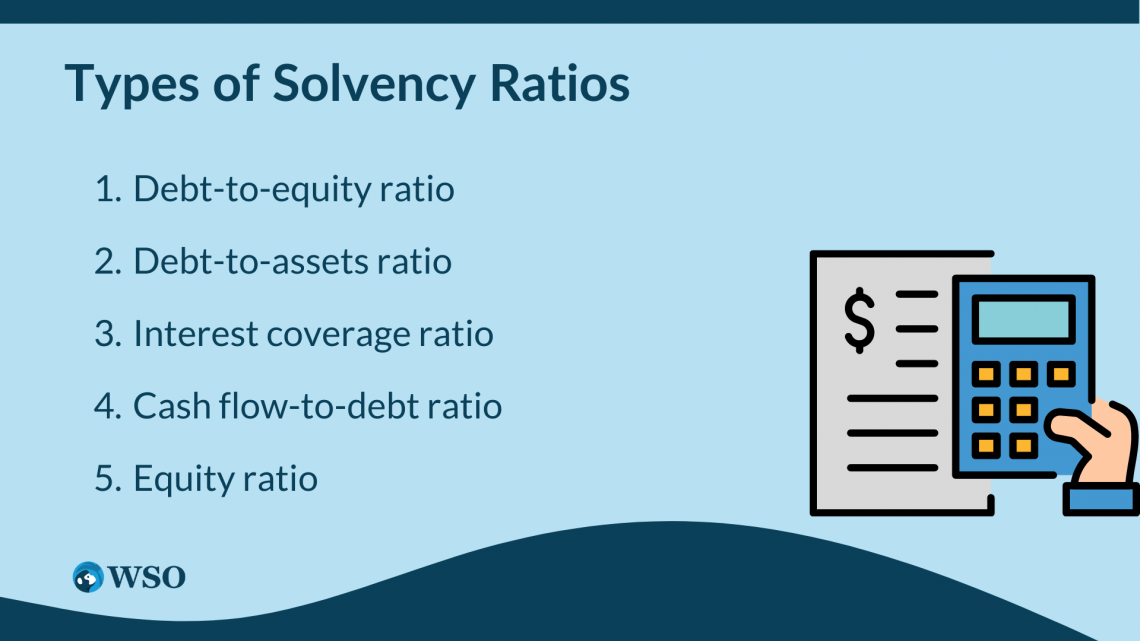

Types of Solvency Ratios

A firm's capability to repay its long-term financial commitments can be examined using various solvency ratios. The most popular among these are:

Debt-to-Equity Ratio

This ratio measures the amount of debt a company has in relation to its equity or the value of its assets that are owned outright. A greater debt-to-equity ratio shows a company's financial leverage, which can increase risk and volatility.

Debt-to-Equity Ratio = Long-Term Debt / Shareholder’s Funds

Or

Debt-to-Equity Ratio = Total Liabilities / Shareholders’ Equity

Debt-to-Assets Ratio

This ratio calculates the proportion of a company's total assets financed by debt. A higher debt-to-assets ratio indicates that a greater portion of the company's assets is financed through borrowing, which can increase risk and affect the company's creditworthiness.

Debt-to-Assets Ratio = Total Debt / Total Assets

Interest Coverage Ratio

This ratio assesses a firm's capacity to cover its interest payments with Earnings Before Interest and Taxes (EBIT). A higher interest coverage ratio implies that a company's earnings are sufficient to cover its interest expenses, lowering the danger of default.

Interest Coverage Ratio = Earnings Before Interest and Taxes (EBIT) / Interest Expense

Cash flow-to-Debt Ratio

This ratio evaluates a company's capacity to produce enough cash flow from operations to pay down its debt.

A high cash flow-to-debt ratio indicates that the firm relies less on external funding to pay its debt commitments and is less likely to default.

Cash Flow-to-Debt = Total Debt / Cash Flow From Operations

Note

A high cash flow-to-debt ratio is frequently regarded as a favorable indicator by investors and creditors, showing that the firm is financially secure and has a strong ability to handle its debt.

Equity Ratio

The equity ratio is a financial statistic determining how much of a company's total assets are financed by equity or shareholder cash. The equity ratio compares the capital shareholders supply with the company's total assets.

A high equity ratio suggests a firm is in good financial shape and relies less on debt funding, whereas a low equity ratio indicates the reverse.

Equity Ratio = Shareholders' Equity / Total Assets

Example of Solvency Ratios

Let’s consider BJ Appliances, a manufacturing company that produces and sells a range of consumer goods. After reviewing its financial statements, we can examine several key ratios to assess the company’s solvency.

In 2022, BJ Appliances had a total debt of $2,500,000 and a total equity of $1,000,000. Therefore,

Debt-to-Equity Ratio = Total Debt / Total Equity

Debt-to-Equity Ratio = $2,500,000 / $1,000,000 = 2.5

A debt-to-equity ratio of 2.5 indicates that the company has more debt than equity. This could be a concern for solvency if the company experiences financial difficulties and cannot meet its debt obligations.

Note

A high debt-to-equity ratio indicates that the company has taken on a lot of debt, increasing the risk of bankruptcy.

Debt-to-Assets Ratio = Total Debt / Total Assets

In 2022, BJ Appliances had a total debt of $2,500,000 and total assets of $5,000,000. Hence,

Debt-to-Assets Ratio = 2,500,000 / 5,000,000 = 0.5

A debt-to-assets ratio of 0.5 indicates that 50% of the company's assets are financed through debt. This means that the company is moderately leveraged and has a lower risk of default than a company with a higher debt-to-assets ratio.

Interest Coverage Ratio = Earnings Before Interest and Taxes (EBIT) / Interest Expenses

In 2022, BJ Appliances had an EBIT of $250,000 and interest expenses of $100,000. Therefore,

Interest Coverage Ratio = $500,000 / $100,000 = 5

An interest coverage ratio of 2.5 means the company's earnings before interest and taxes are 2.5 times greater than its interest expense. This indicates that the company has enough earnings to cover its interest payments and suggests a lower risk of defaulting on its debt.

Current Ratio = Current Assets / Current Liabilities

In 2022, BJ Appliances had current assets of $2,000,000 and current liabilities of $1,000,000. Hence,

Current Ratio = $2,000,000 / $1,000,000 = 2

A current ratio of 2 indicates that the company has twice as many current assets as current liabilities. This suggests the company has sufficient liquidity to meet its short-term financial obligations.

Overall, the financial ratios suggest that BJ Appliances has a moderate level of solvency. Although the firm has more debt than equity, its debt-to-assets ratio and interest coverage ratio indicate enough profits to pay its debts.

According to the current ratio, the corporation may have enough cash to cover its immediate obligations.

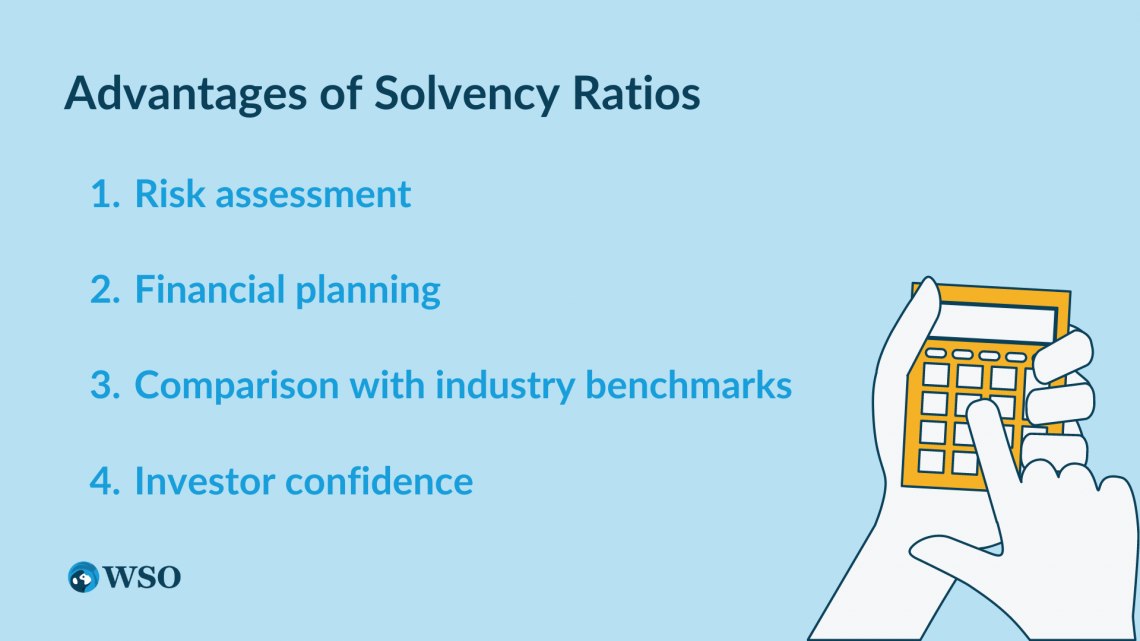

Advantages of Solvency Ratios

Solvency ratios are crucial financial indicators that give essential information about a company's long-term financial health and capacity to pay its debts. Some of the key advantages of using these ratios include

- Risk Assessment: Leverage ratios are an effective tool for determining a company's risk by gauging its capacity to service its long-term financial commitments. By analyzing a company's leverage ratios, investors and analysts can evaluate its overall financial stability and assess the risk of default or bankruptcy.

- Financial Planning: These ratios can help companies develop effective financial strategies and plans for managing debt and other long-term financial obligations.

- By monitoring their leverage ratios over time, companies can identify potential financial risks and make informed decisions about capital investments, debt management, and other financial priorities.

- Comparison with Industry Benchmarks: Leverage ratios can be compared to industry benchmarks to evaluate a company's financial performance relative to its peers. This can help investors and analysts identify companies performing well or struggling within a particular industry.

- Investor Confidence: Leverage ratios can be used to demonstrate a company's financial stability and creditworthiness to investors and lenders.

- A healthy leverage ratio can boost investor confidence and draw in new capital. On the other hand, a poor leverage ratio may raise questions about the firm's financial stability and the possibility of default or bankruptcy.

Limitations of Solvency Ratios

Although solvency ratios provide vital information about a company's long-term financial health, there are some limitations to consider.

- Limited Scope: Solvency ratios merely offer a momentary view of a company's financial situation. They don't always represent the company's overall financial performance or capacity to produce future cash flows.

- Furthermore, these ratios only provide a snapshot of a company's financial health at a particular time. They ignore additional elements that may impact a company's long-term viability, such as shifting economic conditions, modifications in the competitive environment, or unanticipated occurrences.

- Industry-Specific Factors: Different industries may have different levels of debt financing and capital requirements, which can affect the accuracy of leverage ratios.

- Manipulable: Accounting methods and financial reporting practices can manipulate solvency ratios. Firms can employ numerous accounting strategies to inflate or deflate their financial figures, making comparisons between firms or industries difficult.

- Lack of Predictive Power: While leverage ratios can give information about a company's capacity to satisfy long-term obligations, they do not always predict future financial success. When assessing a company's financial health, they are merely one of several elements to evaluate.

- No Consideration of External Variables: External variables that may affect a company's financial stability include changes in interest rates, market circumstances, and regulatory changes; however, solvency ratios do not consider these.

- Lack of Consensus: Financial professionals have not agreed upon the optimal solvency ratio, and different sectors and businesses may have different standards and needs.

Solvency Ratio FAQs

Liquidity ratios gauge an organization's capacity to cover its short-term debt commitments and cash flow requirements. They show how quickly and effectively a corporation can turn its assets into cash, which is critical for preserving financial stability and satisfying immediate financial requirements.

Solvency ratios, on the other hand, gauge a company's capacity to fulfill its long-term financial commitments and make debt payments. They provide indicators of a company's long-term viability and overall financial stability.

Solvency ratios measure a company's ability to meet its long-term financial obligations and debt payments. They show a business's overall financial stability and capacity for long-term operation.

Profitability ratios, on the other hand, gauge a business' capacity to make money through its activities. As a result, they provide insights into a company's operational efficiency, effectiveness, and competitiveness.

Solvency ratios measure a company's ability to meet its long-term obligations. These ratios assist investors and creditors in determining a company's capacity to produce sufficient cash flow to satisfy its debt commitments.

Earning ratios, on the other hand, assess a company's profitability and earning capability. These ratios assist investors in determining how well a firm generates profits and how efficiently it uses its resources.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?