I taught the first session of my valuation class, that I previewed in my last post, today. As part of that class, I do what I call a “valuation of the week”, where I pick a company and value it and then post both my valuation (with the spreadsheet and the raw data that I used) and a shared Google spreadsheet for anyone who wants to take my valuation and make it their own (by changing the assumptions).

I do this for two reasons. First, I believe that you learn valuation by valuing real companies in real time, not by talking about valuation or reading about it. Second, from a purely selfish standpoint, I pick the companies that I find interesting as potential investments or as real world case studies for my valuations of the week. I find the “crowd valuation” that emerges from this process to be useful in reassessing my own valuations.

As my first valuation of the week, I picked Tesla, for three reasons. First, as a technology company in an otherwise capital-intensive, mature business (the automobile manufacturing business), it stands out. Second, the company has a

charismatic CEO, Elon Musk, an ambitious man (and I don’t mean that in a negative sense) with a great deal of imagination.

Third, the stock has taken off in the last year, up more than 500%, fueled by both positive news on the product front as well as on the financial front (increasing revenues, declining losses, paying down of debt).

At its current stock price of $168.76/share, the

market capitalization for the company is more than $20 billion. The question for investors, both in and out of the stock, is not whether the company was a good investment over the last year (of course, it was) but whether it is a good investment today. You can download the most recent

annual and

quarterly reports for the company.

Using the standard metrics, the company seems over valued. With revenues of $1.33 billion and an operating loss of -$217 million over the last twelve months, it seems absurd to attach a value of more than $20 billion to the company. At close to 15.4 times revenues, Tesla is being valued more like a young technology company than an automobile company. However, these standard metrics are also often misleading with young companies, since value should be driven not by revenues and earnings today but by expectations for these values in the future.

Expected Revenues

For Tesla to be able to deliver value as a company, it is clear that it has to scale up revenues. On the good news front, the company has had a good year, with the revenues in the first six months of 2013 of $956 million representing a surge from revenues of $41 million in the first six months of 2012. While growth will get more difficult as the company continues to become larger, the question of how difficult cannot be answered until we define the potential market for the company.

If we define it narrowly as electric/hybrid cars, the market is small (even though it is growing) and the potential revenues will have to reflect that. If we define it more broadly as the automobile market, the market is a huge one and Tesla’s potential revenue expands accordingly.

Since the line between electric, hybrid and conventional automobiles is a fuzzy one, which will get fuzzier over time, I will take the view (optimistic, perhaps) that Tesla is an automobile company that happens to specialize in electric cars and measure its potential revenues by looking at the biggest automobile companies today.

Based on revenues, the biggest companies are those that offer the full range (from luxury to mass market) of automobiles. It is true that BMW and Daimler make the top ten list, but they sell far more than just luxury cars. In valuing Tesla,

I am going to assume (and I am sure that some of you will disagree) that success will bring them revenues close to those delivered by a company like Audi ($64 billion).

While it is conceivable that Tesla’s revenues could approach those of the auto giants ($100 billion plus), I think the revenue growth required to get to those levels would be incompatible with the high operating margins that I will be assuming for Tesla. Assuming that Tesla stays making just electric cars, this forecast is an optimistic one, insofar as it assumes a rapid expansion in the electric car portion of the automobile market.

Profitability

The second piece of the puzzle in Tesla becoming a valuable company is that it has to become profitable. Based on the reported loss of $216.72 million over the last twelve months, the pre-tax

operating margin for the company is -16.31%. It is true that this paints too dire a picture of the company because the company did spend $306 million in R&D over the same twelve month period. Assuming a three-year lag, on average, between R&D expenditures and commercial payoff, and

capitalizing R&D does reduce the operating loss to about -$21.86 million (resulting in an after-

tax operating margin of -1.64%).

To get a sense of what the Tesla's operating margin will be, assuming it makes it as a successful company, I estimated the pre-tax operating margins of all publicly traded automobile companies globally,

dividing the operating income from the most recent 12 months by the revenues over that period for each company.

Since automobile companies have volatile earnings, I also computed a normalized pre-ta operating margin for each company by looking at the aggregate operating income over the last decade, as a percentage of aggregate revenues over that period. The distribution of the both measures of operating margin (the 2013 value and the average from 2003-2012) is shown below:

Note that the sector has low pre-tax operating margins, with the median value of less than 5%. Companies at the 75% percentile generate margins of between 7.5% and 8.5% and there are a few companies that generate double digit margins. One of the outliers is Porsche which reported a pre-tax operating margin of close to 16% in 2013, though its ten-year aggregate margin is closer to 10%. You can

download the dataset that includes the key numbers for all auto companies by clicking here.

For Tesla, we will assume that its focus will continue to be on high-end automobiles and that is margins will converge towards the higher end of the spectrum. In fact, I am assuming that the technological and innovative component that sets Tesla apart will allow it to deliver a pre-tax operating margin of 12.50% in steady state, putting it in the 95th percentile of auto companies (and closer to the margin for technology companies).

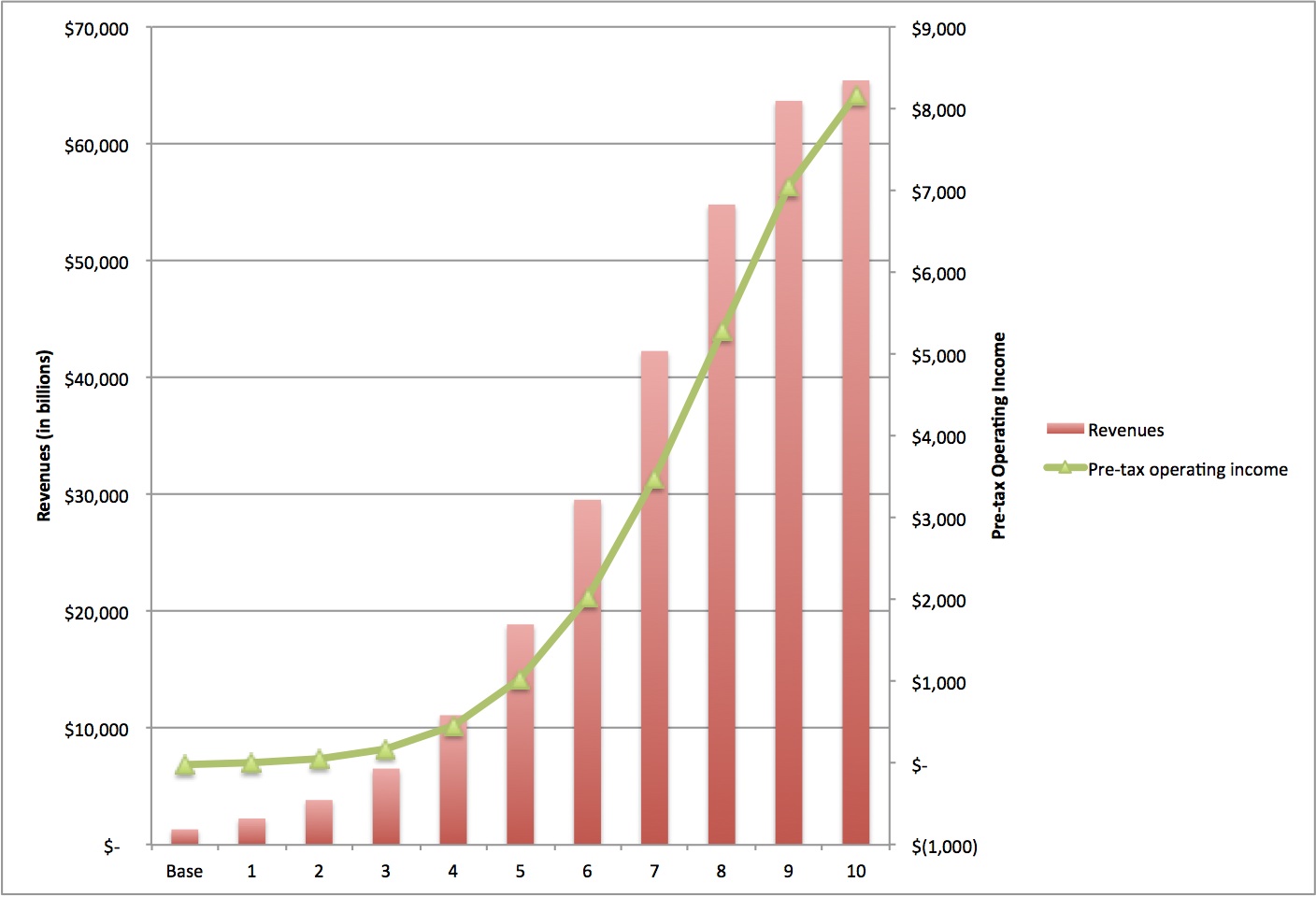

I will assume that the margin improvements occur over time, with the biggest improvements happening in the near years. The figure below captures the forecasted operating income and margin, by year, in my valuation of Tesla:

Based on my estimates, Tesla will generate more than $8 billion in operating income by year 10, making it more profitable than all but three other automobile companies today (Toyota, Volkswagen and BMW).

Investment Requirements

Growing revenues roughly sixty fold and improving operating margins to match the most profitable companies in the sector will require reinvestment. Some of it will take the form of additional R&D, as Tesla tries to keep its competitors at bay, and some of it will have to be in more conventional assembly lines and factories, as production gets ramped up. Over time, I believe that the latter component will come to dominate the former.

In my forecasts, I have assumed that Tesla will have to invest about a dollar in capital (in either R&D or plant/equipment) for every additional $1.41 in revenues. That matches the industry average of the sales to capital ratio of 1.41 for US companies. Since the sales to capital ratio for technology companies is higher (2.66), it is possible that I am over estimating Tesla's reinvestment in the early years.

However, the return on invested capital that I obtain for Tesla in steady state (in year 10), based on my estimates of operating income and invested capital, is 11.27%, putting it again at the top decile of automobile companies.

Risk

Tesla is undoubtedly a risky investment and there are three components of risk that I attempted to incorporate in the valuation:

a. Business/ Operating risk: Tesla is exposed to substantial business risk, some coming from macro economic sources (the strength of the

economy, inflation, interest rates), some resulting from technological shifts (the winning technology in the electric/hybrid auto business is still to be determined) and still more emanating from the sector (with every major automobile company staking out its claim on this segment of the business). To capture the risk,

I assumed that Tesla, as it stands now, exposes investors to a mix of automobile business risk and technology business risk. While I assumed a 60% auto/40% technology mix in arriving at a cost of capital of 10.03%, the value per share that I obtain is not very sensitive to this assumption:

Treating Tesla as a purely automobile company increases its value to about $74.73, whereas treating it as a technology company lowers the value per share to $60.84.

b. Geographic risk: While it is likely that as Tesla grows, it will have to look to emerging and more risky markets, I will assume that its risk exposure for the next decade will come primarily from mature markets, allowing me to use my current estimate of the equity risk premium for the US of 5.8% for the

cost of equity/capital computations.

c. Truncation risk: Tesla, in spite of its lofty market capitalization and recent successes, is still a young, money-losing company. A large shock to its business (from a legal setback, a

recession or a sector-wide slowdown) could put the company's survival at risk.

While that risk has declined substantially over the last two or three years, I think that it still exists and will attach a probability of 10% to its occurrence. If the company does fail, I will also assume that it will lose a significant portion of its value in a distress sale (receiving only 50% of estimated value).

Loose Ends

As with any young company, there are loose ends to tie up that affect value. In particular, I would point to the following:

a. Subsidized debt: Tesla was the beneficiary of subsidized loans from the DOE, amounting to roughly $465 million. While this loan loomed large two years ago, when Tesla was a smaller company with more default risk, it has faded in importance partly because of Tesla's success (and the resulting access to capital markets). Since Tesla has paid down the loan, it no longer has any effect on value.

b. Net Operating Loss carry forward: At the end of 2012, Tesla had a net operating loss of just over a billion that it is carrying forward. I

used the NOL to shelter income from taxes in the early forecast years, pushing up cash flows in those years. As a consequence, Tesla's income is sheltered from taxes for the first six years of forecasts.

c. Management/Employee Options: Of larger import are the management/employee options that Tesla has been generous in granting in the last few years. As of the

most recent 10K, the company had approximately 25 million options outstanding, with an

average strike price of $21.20 and 7 years left to expiration. Since there only 121.45 million

shares outstanding, the value of these deep in-the-money, long term options represents a significant drag on value.

The Bottom line

The ingredients that make a young, money-losing company into a valuable, mature company are no secret: small revenues have to become big revenues, operating losses have to turn to profits, there has to be enough reinvestment (but not too much) to make these changes and the risk has to subside. I am assuming all of these at Tesla but my estimated value per share of $67.12 is well

below the market price of $168.76. You can

download my valuation spreadsheet by clicking here.

Is the value sensitive to my assumptions? Of course, and especially because Tesla is a young company in transition. In fact, replacing my point estimates for the input variables (revenue growth, target operating margin, sales/capital, cost of capital) with

distributions yields a distribution of value for Tesla that reflects my uncertainty about the future:

Note that there are scenarios where the value per share exceeds the current market price ($168.76), but I would add two cautionary notes. First, at least based on my estimates, the probability that the value exceeds the price is small (less than 10%) Second, the combination of outcomes (high revenue growth, high margins and low risk) that would yield these high values are difficult to pull off.

You can accuse me of being too pessimistic in my assumptions, but the narrative that underlies my valuation is an optimistic one. I am assuming that Tesla will grow to be as large as Audi, while delivering operating margins closer to Porsche's. Even with these assumptions, I cannot see a rationale for buying the company at today's market price but that is just my personal judgment. You are welcome to disagree. In fact, if you download my valuation and change the key assumptions, please take a minute to report your estimate of value per share in this

Google shared spreadsheet. Let's see how the crowd valuation plays out!

Exercitationem quisquam dolores et consequatur. Incidunt corporis consequuntur labore magnam.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Nobis quidem velit libero corporis velit perferendis. Nulla quas aliquam quas doloremque. Cum ut voluptate placeat saepe. Veniam quo alias excepturi provident aut. Qui voluptatem doloribus facilis quam.

Saepe debitis optio eum quibusdam et commodi voluptate cum. Adipisci distinctio atque recusandae occaecati omnis enim libero. Quidem eos eos voluptatibus alias nulla ducimus eos.

Voluptatem vel eum sit. Quam neque optio quia sed et eos quas neque. Natus nesciunt nobis vero consequatur. Aut iure eveniet reiciendis ipsum fugit. Necessitatibus labore asperiores itaque omnis fugit quidem sed. Accusantium beatae nulla magnam sit alias ea vitae natus.

Et est impedit autem rerum. Esse quod ducimus dolorum nostrum. Ipsam unde sunt quia beatae.

Placeat aut inventore dolor tempora enim ea. Earum iure voluptatem veniam eum et velit sit. Molestiae sint repudiandae sunt non ab.

Possimus adipisci quisquam eos est sit exercitationem expedita. Ea iste quo id nesciunt. Exercitationem magni doloremque voluptatem corporis eos quae ea. Deleniti nulla adipisci dolor eius consequatur possimus culpa. Minima nisi eos est sit. Ut quia quia labore aliquam quia. Reprehenderit et autem rerum quis odio aliquam aperiam.

Repudiandae odio sint corporis. Accusantium molestias autem voluptatem doloremque assumenda. Eligendi sit ut ratione libero voluptas dolore.

Ea nihil consequuntur omnis officia rem aut blanditiis. Beatae autem ut quam consequatur.

Et temporibus voluptas asperiores natus. Maxime esse a et voluptatem ut. Et hic perferendis quia a et nesciunt quos. Quaerat dolor illo magnam quia cum maiores.

Quia est assumenda qui minima officiis eligendi eveniet. Sed ut est dolores repudiandae quia rerum adipisci. Ratione repudiandae architecto mollitia illo est voluptas velit. Quis quibusdam quos qui et exercitationem omnis. Et et dignissimos aliquam aut.

Ut hic tenetur dolor. A ullam enim vitae asperiores.

Facilis accusamus repellat possimus consequuntur numquam aliquid. Qui magnam quia consequatur ut tenetur voluptatem. Et consectetur cumque pariatur. Libero impedit officiis atque fugiat dolores nihil.

Aut placeat exercitationem omnis sint sint facilis. Eveniet cupiditate iure occaecati tempore. Blanditiis quia aliquid aut. Voluptatem sequi nam similique numquam sed maiores iste. Enim ex eum pariatur quae quis. Consequatur repellat officia enim aut.

Provident earum explicabo iure qui. Illum non ea adipisci iusto ratione. Natus voluptatem laboriosam et enim quia dolorum.

Illo qui est mollitia qui ipsum tenetur natus. Et nostrum impedit voluptatem sed atque amet assumenda aut. Dolores non placeat quaerat cum earum.

Aspernatur doloribus asperiores et et magnam. Et est ab nulla voluptatem consequatur qui illo. Molestias ut repellendus cupiditate repudiandae explicabo non.

Odit et voluptatem omnis assumenda est tempore voluptatum. Et consequuntur dolor optio dolor molestiae tempore aspernatur. Ut dignissimos saepe perferendis voluptates est at. Soluta minus deserunt et eum. Officia ad voluptas quia exercitationem dolore iste. Maxime fugiat sunt ratione et sunt ut aut.

Quas non voluptatem est molestias velit perspiciatis et. Nemo deleniti nobis aut ut quam sit. Explicabo nobis perferendis et nam. Error soluta tenetur eius delectus recusandae dolorem.

Quam placeat consequuntur autem recusandae facilis doloribus. Adipisci nihil blanditiis quod et sed aut.

Beatae voluptatem autem dolore placeat possimus vero. Dolorem nulla voluptatem labore et libero. Ea numquam quia laborum aut. Consequatur quis voluptate ratione a. Vel sit laudantium sit corporis illo. Nostrum dolorum quo culpa praesentium. Fuga facilis voluptatibus dolores qui cum.

Tempore quaerat est earum iure. Facere assumenda velit id ex. Voluptates fuga aliquid dolor dolores molestiae. Minus enim dolorem accusamus fugiat.

Dicta eligendi sunt reprehenderit veniam. Impedit officia aut omnis et. Corporis et et sit neque. Similique non sapiente quia sed.

Et consequatur in accusamus delectus qui. Quam magni optio praesentium.

Animi inventore distinctio itaque in mollitia sed. Ipsam vero aut ipsam ipsam asperiores. Officiis voluptatem harum labore tenetur corrupti iure sed fuga.

Illum quia consequatur nam sunt reiciendis. Doloremque quis maiores molestias ipsa corporis. Accusantium dolorem consequatur impedit iure ut ut. Neque id dolor molestiae amet aut voluptatum pariatur. Et earum ducimus deserunt quia. Cum autem et itaque minus voluptatem voluptatum libero odit.

Sunt ab voluptatem ad. Minima ut perferendis quaerat aut iste cum. Aliquam nihil facere exercitationem voluptas earum quos sint. Distinctio iste quae animi eligendi qui provident. Quo inventore quae possimus. Quam rerum repellat repudiandae aliquam pariatur.

Quis atque voluptatem quidem doloribus harum. Sit impedit quasi veniam maiores nemo ea suscipit. Porro dolor omnis fugit ipsam. Tempore a fugiat quo pariatur. Laboriosam aspernatur illum ut.

Aliquid sed et deserunt voluptas accusamus dignissimos. Eos iste quae sint exercitationem sit sed numquam. Unde et sunt quia sint aliquam. Qui esse quae est sint aut.

Quidem est est atque nobis aperiam sunt voluptatem. Molestias nostrum nobis qui sed qui quos accusantium consectetur. Est quo sint error qui assumenda. Incidunt dolorem quibusdam omnis. Quia totam debitis neque consectetur recusandae aspernatur eligendi. Harum qui quasi autem exercitationem adipisci sed. Fugiat accusantium qui dolorem in nesciunt non numquam.

Et et dolor quia vel dolores pariatur facilis earum. Quidem facilis tenetur debitis porro sit ipsum qui voluptas. Commodi aut qui dolores aut. Dolore eos repellendus aperiam corrupti. Asperiores temporibus exercitationem doloribus earum.

Dolorem eos numquam ut hic. Praesentium similique deleniti est eos ipsum. Pariatur id rerum deleniti dolorem quidem tenetur qui. Voluptas dolor amet sunt.

Quasi aut ut illo labore. In est quas suscipit quas. Blanditiis expedita voluptatem molestiae harum perspiciatis sed. Voluptas mollitia debitis officiis delectus quisquam quisquam.

Dolor et dolor est placeat qui. Qui enim atque eveniet ipsa nostrum enim aperiam. Ad et aut asperiores error sed. Repellat et unde corporis nesciunt doloremque maxime quo. Ab eum et quia sed nemo nesciunt rerum exercitationem.

Voluptas eos porro provident provident excepturi. Dolorem aut vitae quia dolorum eos quaerat qui. Aperiam et id accusamus et.

Ut explicabo est ut voluptatem. Qui expedita voluptatem natus expedita ducimus nisi dolores. Quod placeat adipisci alias aliquid aut.

Laboriosam cumque vel aliquid accusantium qui odit. Ex in ipsum doloremque voluptatibus et qui similique id. Vitae consectetur voluptas aut quia dolorem cumque. Assumenda earum est dolorem quis voluptatem magni. Omnis maxime sit et quod fugit explicabo aut.

Velit sint mollitia vitae aut omnis iure minima. Est id et sit ipsam. Quo iure excepturi dolores qui est in explicabo.

Velit molestiae repellat tempora minus. Saepe eveniet et eligendi molestiae. Autem laudantium rerum voluptates incidunt.

Dicta quia optio reprehenderit. Rerum voluptas laborum similique necessitatibus odit.

Libero eum nobis eum veniam repellendus error dignissimos laborum. Esse aliquid blanditiis aperiam accusantium fuga reprehenderit in.

In iusto earum ea ut asperiores deleniti. Odio et assumenda numquam praesentium et non maiores. Voluptatum unde repudiandae consequatur rerum est velit blanditiis. Sint dolores et architecto. Sit ut eos ea repellendus. Dolor iure distinctio et in eos dolor. Id ut voluptatem expedita explicabo.

Dolorem reiciendis eum est facilis. Dolores quis porro corporis qui. Magni dignissimos repellat velit doloremque. Adipisci ea earum aut vel. Aspernatur ipsa aliquam deserunt.

Tempore non numquam harum non quas sit. Quia et ipsam iste et sint adipisci. Quis explicabo ipsa incidunt culpa. Sit accusamus ad ex consequatur quod.

Neque vel nesciunt commodi laudantium et. Aut aliquam optio totam incidunt. Et id nisi omnis ea voluptas. Laudantium eum ex impedit et itaque natus maiores.