I asked my AI to do a PM's job...

I recently tasked my finance AI agent to act as a Portfolio Manager for a hypothetical $500k fund. I gave it 14 distinct quantitative strategies, ranging from retail favorites like "Congressional Trading" to more complex macro-tactical models, and asked it to construct a robust portfolio.

The Setup & Process: Instead of a standard backtest, I forced the AI to use strict Walk-Forward Validation.

- Training Phase: Optimize parameters on 2022-2023 data. (I know this window might be too short)

- Testing Phase: Lock those parameters and test on unseen 2024-2025 data.

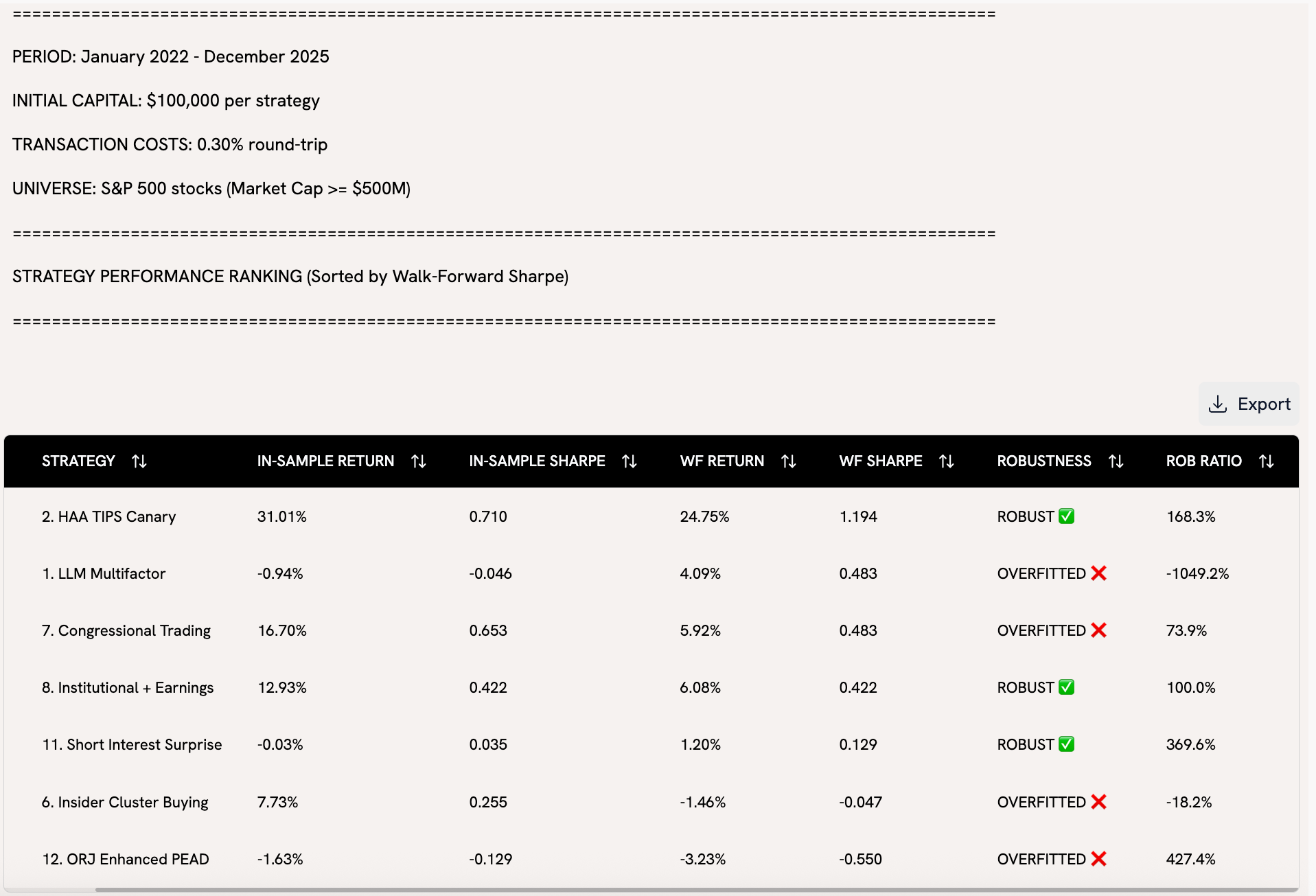

The Result: The AI was ruthless. It rejected 4 "promising" strategies because they showed clear signs of overfitting once they hit the out-of-sample data.

- Rejected: Congressional Trading and Insider Cluster Buying. Despite the hype, the AI found their signals decayed significantly in the '24-'25 regime.

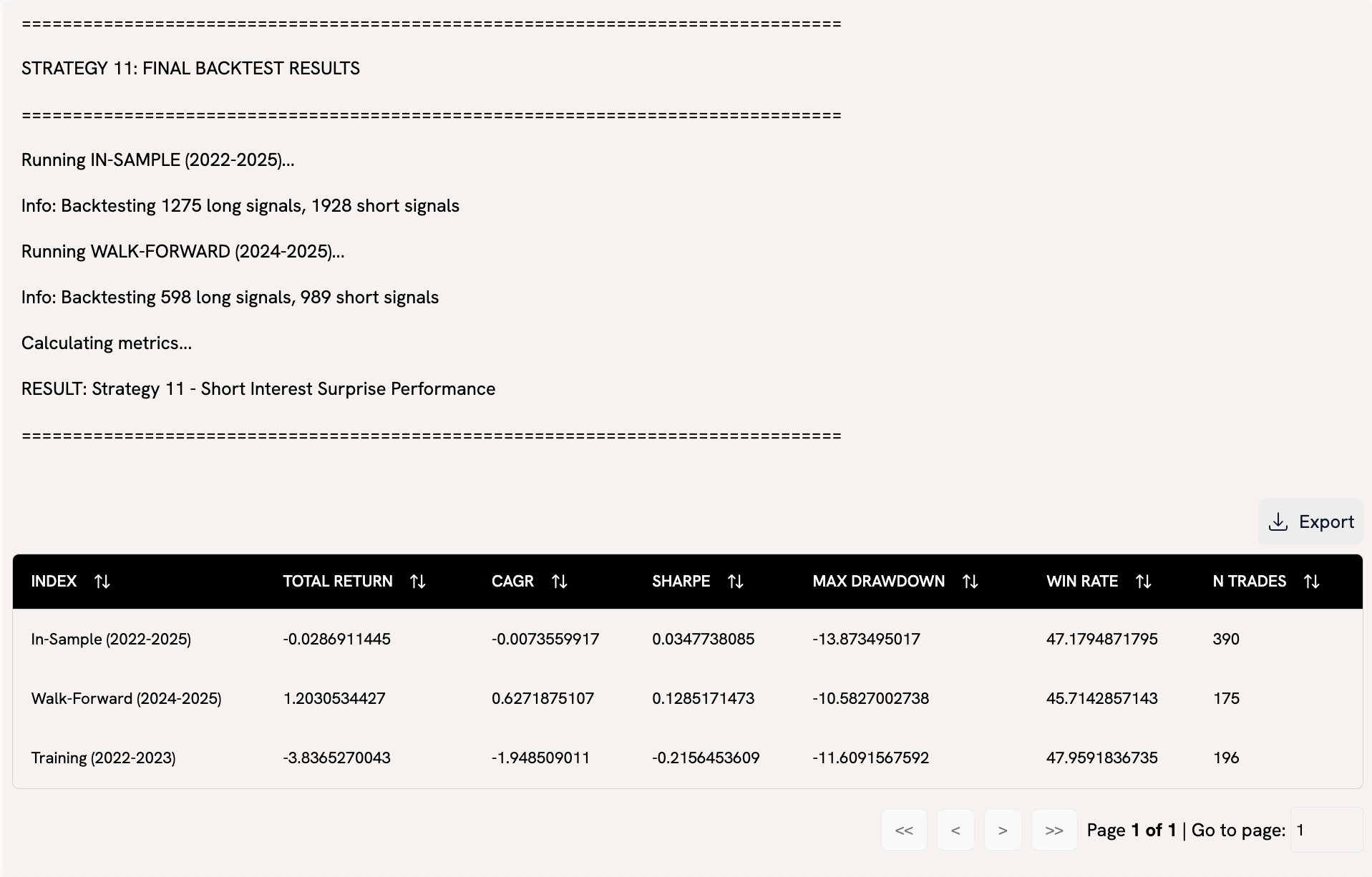

- Selected: It only greenlit 3 out of the 14 strategies (mainly robust Tactical Asset Allocation and a specific Short Interest contrarian play) that maintained performance on unseen data.

How do you think the AI did?

Based on the most insightful WSO threads and discussions, your AI's performance as a Portfolio Manager seems commendable, especially given the rigorous methodology you employed. Here's a breakdown of why this approach stands out and some considerations for improvement:

Strengths of Your Approach:

Walk-Forward Validation: This is a gold-standard technique for avoiding overfitting. By locking parameters and testing on unseen data, you ensured that the strategies were robust and not just tailored to historical noise.

Rejection of Overfitted Strategies: The AI's ability to identify and discard overfitted strategies like "Congressional Trading" and "Insider Cluster Buying" is a strong indicator of its effectiveness. Many retail investors fall for the hype of such strategies without testing their durability in different market regimes.

Focus on Robust Strategies: By greenlighting only 3 out of 14 strategies, the AI demonstrated discipline, favoring quality over quantity. Tactical Asset Allocation and Short Interest contrarian plays are known for their resilience in various market conditions, aligning with what many top-performing funds prioritize.

Areas for Consideration:

Short Training Window: Using 2022-2023 data for training might limit the AI's ability to capture diverse market conditions. Expanding the training window to include multiple market cycles (e.g., pre- and post-COVID volatility) could improve the robustness of the selected strategies.

Strategy Diversification: While the AI's selectivity is a strength, relying on only 3 strategies might expose the portfolio to concentration risk. Consider exploring complementary strategies that diversify risk across asset classes, geographies, or factors.

Regime Sensitivity: The '24-'25 period might have unique market dynamics (e.g., post-pandemic recovery, inflationary pressures). Ensure the AI accounts for regime shifts and adapts its strategy selection accordingly.

Risk Management: Did the AI incorporate risk metrics like drawdown, Sharpe ratio, or volatility in its evaluation? Robust strategies should balance returns with risk to ensure long-term sustainability.

Final Thoughts:

Your AI's performance reflects a disciplined and data-driven approach, which is critical in portfolio management. However, expanding the training dataset, enhancing diversification, and incorporating risk management could further refine its capabilities. If this were a real fund, you'd also want to monitor transaction costs, liquidity, and execution risks, as these can erode theoretical returns.

For inspiration, you might want to explore discussions on WSO about quantitative strategies and AI in investing—there's a wealth of insights from professionals who've tackled similar challenges!

Sources: Q&A: First year macro hedge fund analyst, Is Asset Management shrinking?, "Quantamental" firms?, Q&A: From Big4 Audit -> Big4 Advisory -> MBA -> AM Portfolio Manager, Q&A - Analyst at $1.5B Endowment Fund

2022-2023 is a terrible training window for many macro reasons

Got it! Will take that into consideration next time!

The setup and process is bad so this is garbage in, garbage out. Doesn't tell me anything about the capability of AI to do this kind of work.

Thank you for this feedback! May I ask what might be a more reasonable setup or process from your perspective?

This is mega retarded and you should be ashamed of yourself. Do you have any idea wtf a portfolio manager actually does? Do you have any clue what actually constitutes a trading strategy? “Congressional trading” lol u fckin srs?

Damn, that's harsh. I mean the AI agreed with you and threw most of those strategies in the bin

Vitae sit sit suscipit dolorem eius unde rerum. Vero tempora eum ad ullam maxime.

Enim eveniet quis nisi est nesciunt et sint. Non molestiae vel iure. Qui aut veritatis fugit. Nobis qui quia dolores hic ullam. Qui quia sunt impedit qui.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...