Capital Allocation in Mid-Cap Fintech: A Look at Shift4's Internal Ledger

High-beta payment processing equities are currently experiencing severe multiple compression. In an environment dominated by shifting cost-of-capital assumptions, traditional valuation metrics—such as adjusted EBITDA projections and theoretical total addressable market expansions—often lose their predictive value. For institutional investors conducting deep-dive due diligence, the most reliable gauge of a company's structural integrity is the direct capital allocation behavior of its executive board.

The Distribution Wave Across the Tech Sector

Contextualizing management behavior against macroeconomic realities is a standard prerequisite for any fundamental thesis. Recent Form 4 filings show a noticeable increase in executive sales across major tech companies. This broader trend is largely driven by a realization that the zero-interest-rate environment has definitively ended, prompting C-suite officers to lock in personal liquidity and diversify their concentrated wealth via 10b5-1 execution plans. Observing whether a specific management team is participating in this distribution wave or actively resisting it is a core component of assessing forward risk.

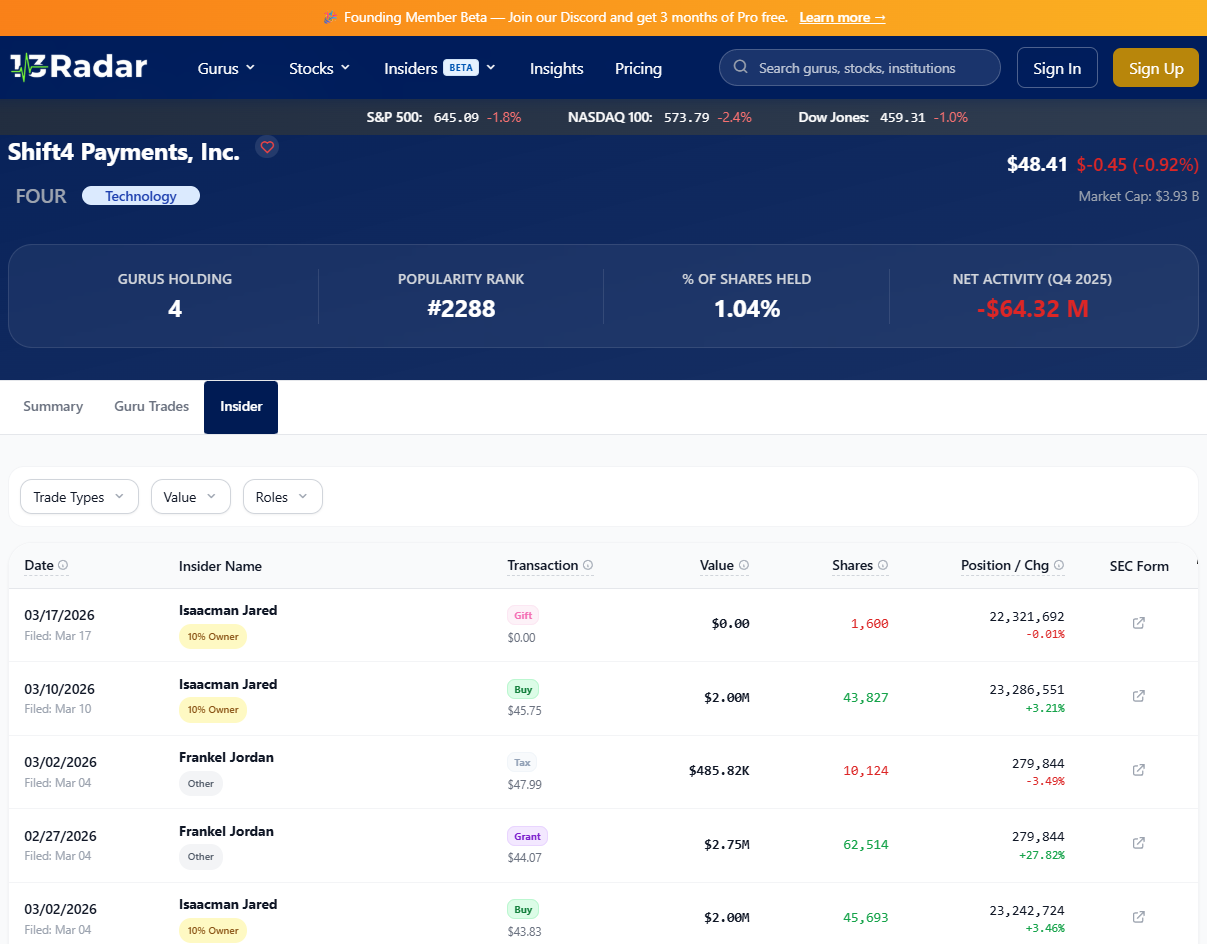

The Divergence: Analyzing the FOUR Cap Table

A granular review of the FOUR recent insider trading reveals the actual financial posture of Shift4 Payments' leadership. In corporate finance, an executive's refusal to liquidate vested equity during a sector-wide drawdown is not merely a passive holding strategy; it is a calculated assertion regarding the firm's internal rate of return.

- Equity as Currency: When founders and key directors maintain or expand their exposure rather than dilute it, they are signaling that the company's internal growth metrics remain highly robust despite public market volatility.

- M&A Defense: Concentrated internal ownership serves as a natural poison pill against hostile, undervalued buyout attempts from larger private equity sponsors.

The Institutional Takeaway on Valuations

Hedge funds and distressed value shops do not typically allocate capital based on public relations sentiment; they track the raw, post-tax cash moving through the regulatory wire. If the data indicates that the primary architects of Shift4 are comfortable maintaining heavy exposure to their own balance sheet, it mathematically establishes a fundamental support level grounded in executive conviction. Conversely, heavy, discretionary liquidations would suggest that internal models no longer justify the current public multiple. In the current liquidity environment, identifying these specific boardroom alignments provides a strictly empirical framework for evaluating the asset's true risk-to-reward ratio.