Discussion: Quant Signals & Regime Change – Observations from the RenTech 13F Data

The spread between the "Mag 7" and the equal-weighted S&P 500 has reached levels that typically trigger institutional rebalancing. With the recent volatility in semiconductor names (post-DeepSeek efficiency news), we are seeing a significant divergence in how fundamental funds and quantitative funds are reacting.

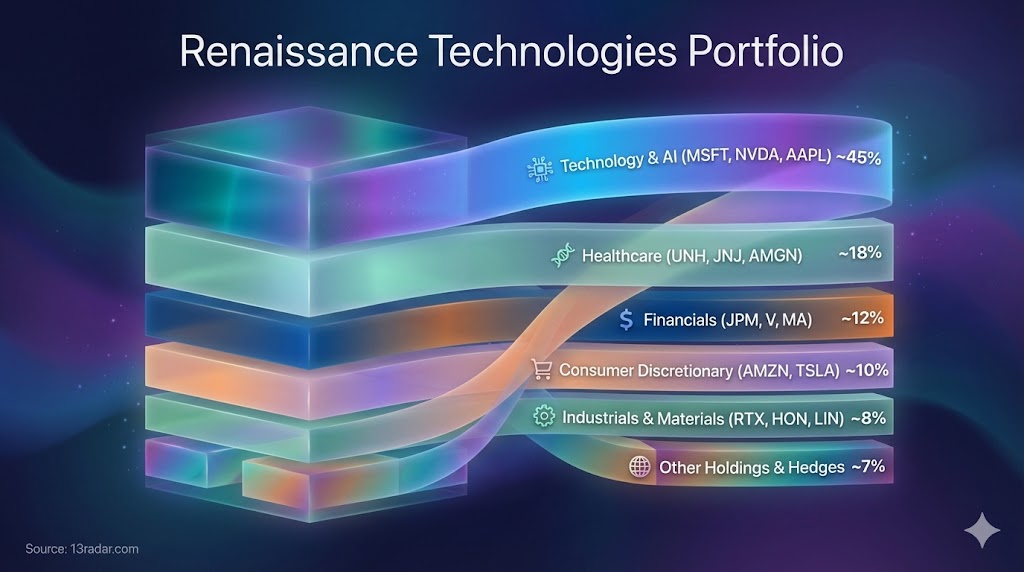

A factor analysis of the recent renaissance technologies portfolio filings suggests that the "Medallion" methodology might be positioning for a regime shift. Unlike long-only growth funds that are forced to ride the beta wave, the latest data points toward a systematic reduction in single-stock concentration risk, favoring a "basket approach" over conviction bets.

1. Factor Rotation: Momentum to Mean Reversion

The defining characteristic of the current allocation is the extreme breadth of the tail. While the street remains obsessed with NVDA/AMD, the quantitative filings reveal a heavy accumulation of mid-cap and small-cap equities, particularly in the Industrial and Consumer Discretionary sectors.

This looks like a classic Mean Reversion play. The valuation gap between large-cap tech and the "average stock" is at historical highs. The systematic accumulation of these underperforming sectors implies that the models are assigning a higher probability to a "Catch-up" trade from the broad market, rather than a continuation of the mega-cap breakout.

>>> DATA OBSERVATION: The "Long Tail" Exposure

Analyzing the position sizing distribution:

- Concentration Risk: Top 10 holdings represent a significantly lower % of AUM compared to the average Macro Hedge Fund.

- Beta Hedging: The portfolio appears to be maintaining market neutrality by balancing high-beta tech with low-beta pharmaceuticals and utilities.

- Implied Volatility: The shift suggests a defensive posture against localized sector blowups (like the semi correction).

2. The "Quality" Factor: Meta Platforms vs. Hardware

It is worth noting that not all tech is being treated equally by the algorithms. While pure-play hardware exposure has seen some trimming in line with volatility targeting, Meta Platforms (META) remains a prominent holding in the data set.

From a factor perspective, this likely separates "Growth" from "Quality/Profitability." Meta's metrics—specifically Free Cash Flow (FCF) yield and Return on Invested Capital (ROIC)—rank highly on fundamental quant screens. This suggests the sell-off in tech is not indiscriminate; the models appear to be filtering for balance sheet strength over revenue growth projections.

3. Disconnected from the Narrative

The most striking aspect of the portfolio structure is its lack of correlation with the daily news cycle. While the market panic-sells on AI efficiency fears, the RenTech holdings show little evidence of reactive trading. The positions are seemingly calibrated to capture liquidity premiums and arbitrage pricing inefficiencies rather than directional bets on the "AI theme."

Open Question: Is anyone else seeing a similar rotation into small-caps/value in their internal fund flows? Or is this just a short-term volatility adjustment?

Exercitationem consequuntur aut nostrum. Suscipit voluptas omnis odio. Ut maxime velit qui quidem recusandae non nisi. Exercitationem veniam ullam distinctio a fugiat. Vel vero reprehenderit et rerum quae suscipit hic. Est ullam similique similique nostrum corrupti.

Rerum et corporis aut et assumenda. Autem rerum harum qui omnis. Qui consequatur repellendus occaecati ipsa nam. Pariatur doloremque ex saepe assumenda.

Qui est ab doloremque error sint blanditiis. Quia voluptatem iusto est eligendi occaecati aut officiis. Beatae quisquam harum illum consequatur ut dolores. Animi animi et sed qui est molestiae sequi. Et amet qui eius animi.

Voluptatem laudantium possimus nisi explicabo praesentium laudantium. Unde eligendi ut et aut quia fuga hic. Praesentium rerum eius laborum voluptatem in. Aliquam et doloribus libero perspiciatis quia repellendus.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...