|

Give ‘em Some Credit

We often talk about how much American consumers adore their credit cards. But, like some multi-decade marriages, the attraction tends to fall off after a while.

Don’t worry; they’re still far from breaking up. But safe to say US consumers have hit a rough spot with their significant other. In December, consumer credit growth slowed to its lowest rate in more than two years, meaning credit growth hasn’t been this bad since the days when no one even knew what the term “meme stock” was.

Like anything in economics, it’s not just a double-edged sword; it’s more like a mace with all those spikes, as there are often endless ways to interpret any given piece of data.

Before we get started, here are some of the numbers:

- Consumer credit rose by $11.6bn in December against expectations of $26bn

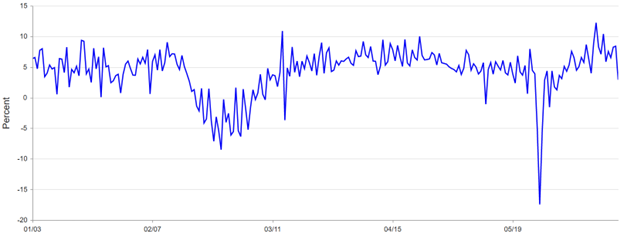

- ^ That’s a growth of 2.9%, the smallest in over 2 years

- Revolving credit (i.e., credit cards, etc.) grew by only 7.3% annualized

- Non-revolving credit (i.e., auto loans, etc.) grew by only 1.5%

Disclaimer: mortgages are not included in this report from the Federal Reserve, so don’t come at me with all this “oh, but what about housing??” b.s.)

Now that we got that out of the way, let’s speculate wildly on what this could mean.

Traditionally, declining consumer credit growth is a horrifically bad sign for the US economy. As we said, credit and consumers have been madly in love for decades in the States, so when the romance slows down, the whole economy gets concerned.

And that’s largely because consumer spending makes up two-thirds of the US GDP in any given year. There’s no way we’d be a $25tn economy without the likes of Discover all the way up to Amex.

Credit drives spending like a gas pedal drives a car, which is obviously great for the macro environment. But, taking a micro perspective, this could be interpreted as a good sign for the balance sheet of the average consumer. Ben Franklin said that he’d “rather go to bed without dinner than rise in debt,” and although we’re not exactly fans of starving over here, we can’t help but smell what he’s steppin’ in.

Some debt can be good, but obviously, an excess of debt is a great way to put on some financial handcuffs. The fact that debt growth on the balance sheet of the individual consumer slowed on average isn’t exactly the worst thing in the world from a micro perspective. Lesser debt means fewer defaults as well as more discretionary income, giving consumers the assist from the micro perspective.

Unfortunately, this is Macro Monkey, and the macro generally tends to outweigh the micro. In economics, scaling up from the individual to the national is far from linear. The magnitude of a slowdown in credit and what that means for the “C” in the below equation carries far more importance.

C + I + G + NX = GDP

Let’s not sit around and ponder why credit might be slowing. I’d like to introduce you to my friends Rate Hikes and Expected Recession. I think they may have something to add here.

Credit carries elasticity, and that elasticity can vary based on wider economic conditions. When good times are expected, an uptick in interest rates isn’t generally a reason to run for the hills. But, when expecting poor economic performance in the short- and intermediate-term, any growth in a monthly payment is a reason to run past the hills and just keep running.

Now, with recession fears even trendier than the latest TikTok dance, combined with the fastest rate increases the US economy has ever seen, it’s no surprise consumers are falling out of love with their credit cards.

Like any relationship, it’s complicated. They have their ups and downs, but they always find themselves back together in the end. Someone get Julia Roberts and Hugh Grant over here; I think we’ve got a great idea for 2023’s next rom-com.

|

Iure cupiditate minus vero natus ut deserunt enim molestiae. Non facilis numquam dolorum mollitia ab voluptas eligendi. Nihil architecto eum nemo nulla. Dicta quo sapiente nemo alias rem accusamus. Debitis ex eaque voluptatem.

Sapiente tenetur qui maiores et omnis libero. Dolor et voluptatem aut id. Cum earum animi ut voluptates deleniti deleniti sint.

Sint fugiat assumenda eos qui culpa. Eveniet facilis quo corporis dolore necessitatibus. Repellat non a nam eveniet minus laudantium aperiam. Velit officiis cum reiciendis et aperiam excepturi et. Illo corrupti fugit autem quis.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...