Institutional De-risking: Analyzing the 13F Total Liquidation Anomaly in the Current Cycle

In an equity environment characterized by highly correlated passive inflows and compressed risk premiums, discretionary macro funds are aggressively re-evaluating their public exposure. The decision to fully liquidate a mature, multi-billion-dollar equity portfolio is rarely a routine rebalancing act; it is a definitive structural bet on impending volatility or a fundamental breakdown in public market valuations. For institutional analysts, observing how elite venture operators manage their liquid books provides a raw, unfiltered look at true macroeconomic conviction.

The Mechanics of a Complete Liquidation

From a trading desk perspective, unwinding concentrated, illiquid tech positions without destroying the bid requires significant runway and algorithmic precision. Institutional data suggests that the prolonged period of elevated tech valuations served as a prime liquidity event, allowing systematic 10b5-1 execution plans to quietly absorb passive index demand. When apex venture operators utilize extended bull market liquidity to entirely exit their historical positions, it signals a stark divergence between internal fundamental modeling and public consensus. The capital is not disappearing; it is simply being rotated out of a public tape that no longer offers an asymmetrical edge.

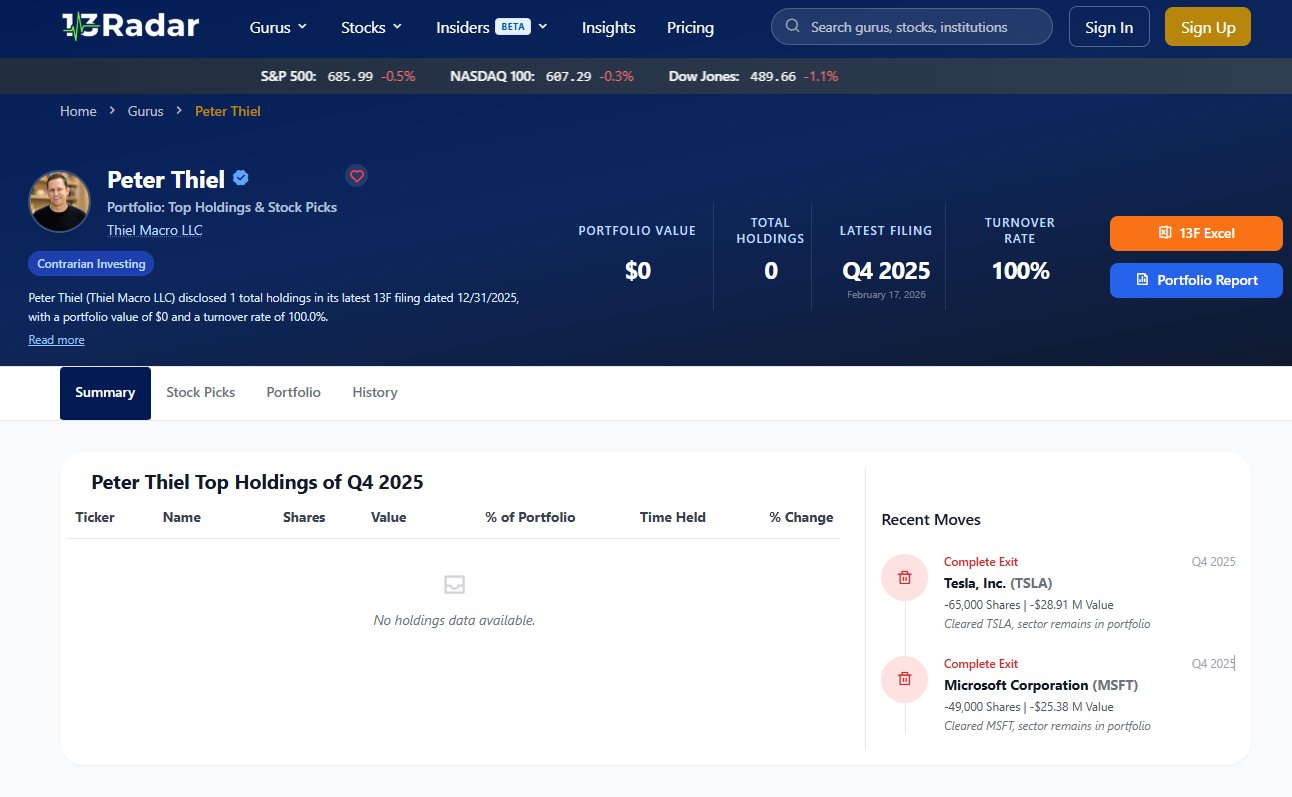

📊 SEC FILING ANOMALY: THE BLANK SLATE 📊

"An empty 13F is the ultimate idiosyncratic signal."

The definitive structural shift became public record when regulatory filings confirmed that peter thiel's hedge fund sold all public stock holdings in q4 2025. Transitioning from maintaining highly concentrated, strategic bets in data analytics and software to possessing absolutely zero public equity exposure is unprecedented. It requires an immense degree of macroeconomic pessimism regarding the near-term viability of public tech multiples.

Cash as an Aggressive Tactical Allocation

In modern portfolio theory, holding zero equities during a momentum-driven cycle is not a passive stance; it is a highly aggressive, directional position. It implies that the asymmetric upside has entirely evaporated from the public exchanges. For event-driven and macro analysts, tracking this specific breed of complete divestment provides a critical data point: identifying the exact moment when the architects of the tech sector fundamentally conclude that risk-free yields offer a superior risk-adjusted return compared to their own publicly traded equity.

When the premium on information asymmetry drops to zero in public markets, the smartest capital seamlessly retreats to the private sector.

Quo aut molestiae quaerat sit veniam debitis rerum. In ut officia voluptatem dolorem voluptas quia rerum. Dolorem labore vel temporibus culpa ut.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...