The Cap Table Defense: Why Anthony Noto’s $500K Print Changes the SoFi Short Math

The recent Muddy Waters short thesis against SoFi Technologies has generated significant chatter across trading desks, primarily focusing on accounting mechanics and fair value adjustments. However, dissecting a short report is only half the battle; the real alpha lies in observing how the targeted management team responds in the capital markets. While corporate PR teams typically issue sanitized press releases to defend their balance sheets, true structural confidence is only validated through SEC-mandated open-market transactions.

Desk Note: The Liquidity Counter-Offensive

When an institutional short seller attempts to force a liquidity event or trigger capitulation, they rely on a vacuum of institutional support. A CEO stepping in to personally absorb the float at depressed prices effectively weaponizes the cap table against the bears. It creates a hard fundamental floor that quantitative models and risk parity equations are forced to immediately price in.

Parsing the SEC Data Room

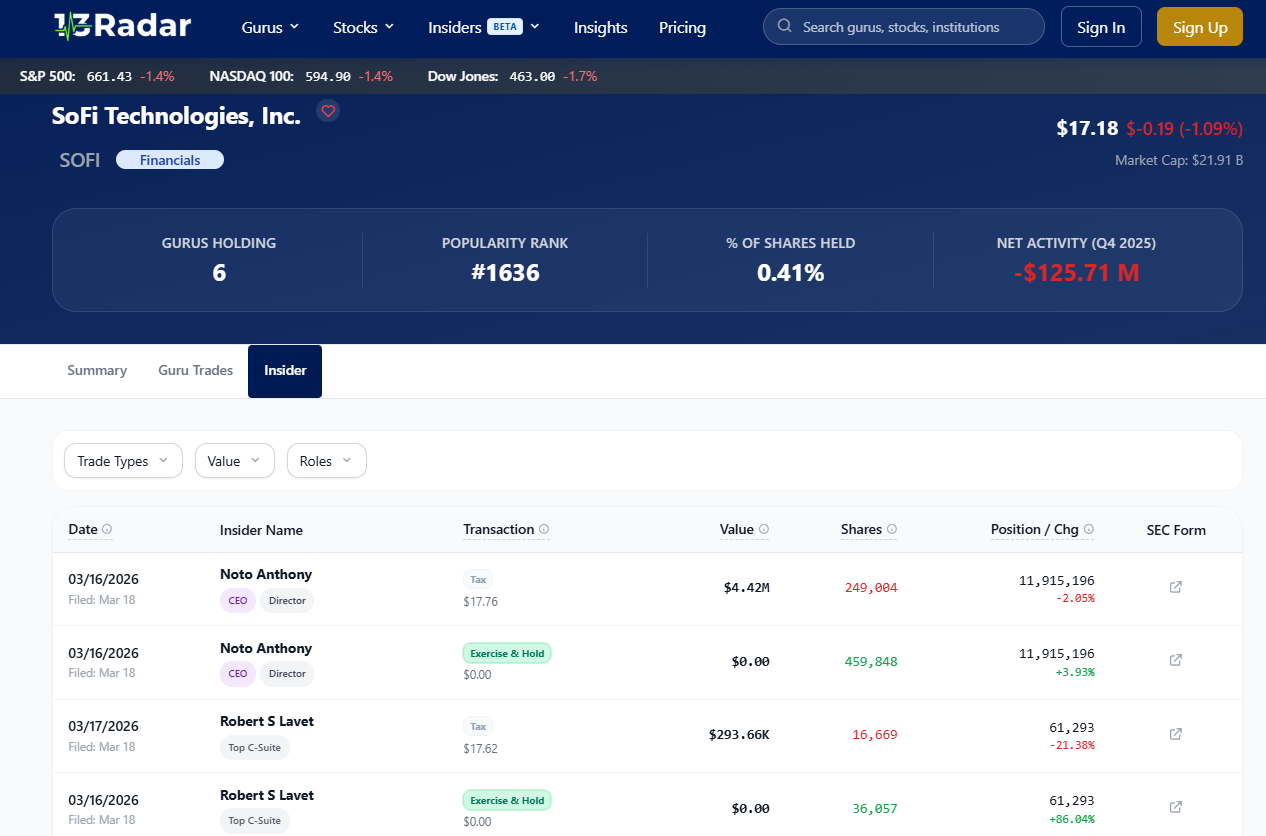

For portfolio managers evaluating the risk/reward skew of this specific fintech battle, the internal tape is the only metric that matters right now. CEO Anthony Noto's decision to deploy half a million dollars of his personal cash directly into the teeth of a high-profile short attack is a masterclass in market signaling. When analyzing the latest SOFI insider buying, the data reflects an executive who possesses absolute asymmetrical information regarding the firm's loan book, deposit stickiness, and upcoming margin expansion. Management does not throw $500k of personal capital into a burning building; they allocate when their internal DCF models show that the public market has severely mispriced the equity.

The Macro Divergence Factor

What makes this specific capital allocation so compelling for institutional observers is its stark contrast to current behavior in Silicon Valley boardrooms. Recent Form 4 filings show a noticeable increase in executive sales across major tech companies. We are currently in a macroeconomic environment where legacy software founders and AI hardware executives are aggressively utilizing elevated multiples to de-risk their personal portfolios and distribute stock. Against a backdrop of sector-wide tech distribution, a fintech CEO aggressively buying his own equity is a glaring anomaly that demands serious institutional attention.

Recalculating the Short Borrow Risk

The mechanics of shorting a high-beta tech stock become exponentially more dangerous when the C-suite goes on the offensive. Borrow fees and margin requirements hinge on momentum, but a massive executive buy-in fundamentally disrupts the bearish algorithm. For hedge funds currently short the name, this Form 4 print serves as a stark warning: the underlying fundamentals may be far more resilient than the sell-side consensus suggests. In the modern market, observing where the smartest money in the room places its proprietary capital remains the ultimate arbiter of value.

Dolore voluptas officiis aperiam expedita nihil quo. Et nihil inventore in eveniet sit vel velit. Ducimus facilis ipsam nostrum aut. Ut illo incidunt quos ad iste. Rerum dolore odio voluptatum ipsa iure est.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...