DATA : A bitter pill to swallow for MM London advisory exits.

To sum up - Lateral to BB/EB/Balance Sheet or MBB (unless you have this experience already before MM broker).

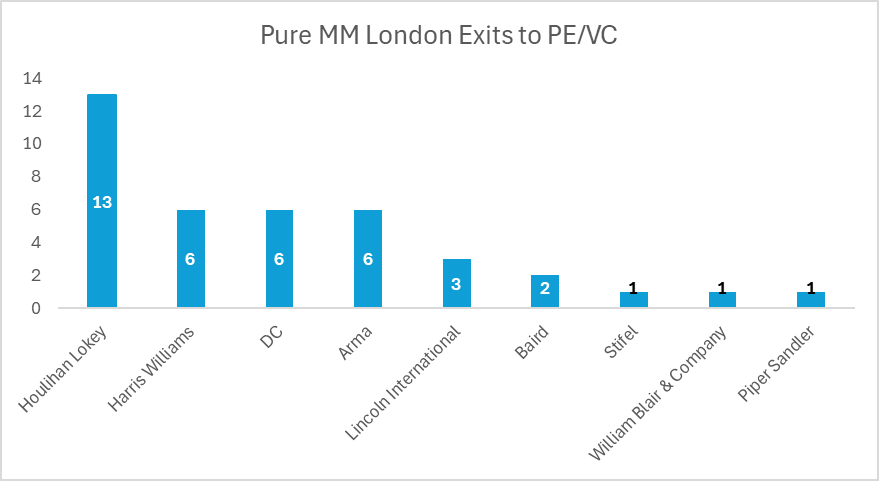

Spent a few hours looking at MM exit ops to Private Equity (Long train journey) and am disappointed with what I have seen. (Shock - interns ranking / rating firms has WSO has no impact on reality). Single digits over the span of more than 10 yrs to PE.

Note : These are not the KKRs of the world - many of these are 2 man PE firms ( it looks like there is no / not much committed capital).

Time range - A far back as you can go to present. (Definitely over 10 yrs)

Location - LONDON.

Firms - As selection of Mid Market Advisors / Brokers - whatever you would like to classify them.

What does this analysis cover?

If they were at Evercore [insert any BB/EB] and lateralled to a MM company - they are not "ex-MM" and have not been included on this data - they are ex-Evercore.

Similarly if they have Big 4 experience (Accounting qualification) then they have not been included here. (There are a LOT more ex big-4 than there are ex-MM in London PE firms. Not even a comparison , which makes sense - accountants are extremely useful in MM deals.

Similarly, big law qualified lawyers who have moved into an MM firm and moved on after that to a PE firm have not been included.

For the US and Europe this will (and is) completely different.

I have every single firm the individuals moved on to (by firm). This is a sum of that.

Interesting Note : Houlihan places well into special sits (of course due to their strength in restructuring)

Jeff no longer MM, congrats!

Based on the most insightful WSO content, the data highlights a challenging reality for mid-market (MM) advisory exits in London, particularly when it comes to transitioning into Private Equity (PE). Here are the key takeaways:

Limited PE Exits from MM Advisory in London:

Exclusions in the Analysis:

Houlihan Lokey's Unique Position:

Geographical and Market Differences:

This analysis underscores the uphill battle for MM advisors in London aiming for PE roles, with a clear advantage for those with Big 4 or BB/EB backgrounds.

Sources: https://www.wallstreetoasis.com/forum/private-equity/going-from-mm-investment-bank-to-mega-fund?customgpt=1, Any career regrets after moving from PE to public markets?, https://www.wallstreetoasis.com/forum/consulting/qa-eb-co-invest-pe-m7-mba-mbb?customgpt=1, Thoughts on Blair in 2021 and Beyond?, Breakdown of Post-IB Exit Opportunities

Did you include the RX team @ HL or only the M&A guys? Seems a bit odd

Your William Blair numbers are wrong. I know at least 3 (not great) who left to the buyside straight from Blair.

Given you are including special sits in your HL numbers, I think you should include non-traditional PE roles in your analysis as well.

However, I do agree you need to lateral to a BB / EB to have more options. The problem with the MM shops is that they are churning sell sides (process driven) rather than doing buysides (analysis driven) and hence you're not putting on your investor hat when you do those deals.

Hi ,

1. It says "LONDON" in capital letters....: "Location - LONDON." ; "For the US and Europe this will (and is) completely different."

So 1 guy went to buyside in London? and would be interesting to see his background. Did he work there at an internship before etc? This is materially lower buyside exits than something like FTI consulting etc and big 4.

2. "Non traditional PE" has been included in PE...special sits is still PE right.

3. Agree with your last paragraph. Additional thought is : at the MM level you can larp as a banker all you want...you are just a broker. Not proper finance - and that is reflected in the poor exits which is a shame given hours etc. (Chances of buyside any higher at mid market M&A advisory vs FTI consulting?).

Note: does NOT include portfolio positions etc. The analysis is JUST deal team aka investing.

Think it’s quite weird that you didn’t separate HL M&A and RX, think RX is one of the best teams in London and top in its niche so no surprise it places well in Special Sits - would remove any ex-RX samples

Hi intern - appreciate your frontal lobe is still in development, pls fix. I'm not going to split up specific teams for MM banks esp when its not straight forward to do so. If you use your critical thinking skills you will be able to understand HL minus RX = similar exits to the other MM brokers. Obviously - that is why I explicitly said "Houlihan places well into special sits (of course due to their strength in restructuring)".

Haven’t updated the title, am an analyst at a MF. Apologies for poking a hole in your exit analysis, enjoy LMM buyout buddy

LOL, HL Rx is nothing but a beggar or crumbs eater from PJT table. In the UK, Rx is not concentrated to only Boutiques, Big4 relationships is hard to replícate

Repellat veniam quod autem quod est sit. Sit quo vel ut molestiae. Sapiente quo sint tenetur distinctio voluptatibus minima iure nemo. Repellat non consectetur laborum nemo sequi ut vel.

Quam praesentium delectus quia laboriosam. Consequatur repellendus eos omnis corporis delectus voluptate iusto quia. At dicta eos velit. Quidem qui omnis quas amet voluptatibus quidem eos nostrum. Officiis perspiciatis harum soluta voluptate.

Maxime rerum in voluptates doloremque. Vel ut eius assumenda rerum voluptatum qui consectetur. Rem quasi dolores autem nihil autem voluptatum. Totam ut nobis blanditiis deserunt voluptatum perspiciatis vel. Ex deserunt eligendi sit. Similique sed aut dolorem quam laboriosam et consequatur.

Modi temporibus molestias hic minima. At nulla quo minima hic nulla. Fuga ut voluptas tenetur est. Rem aut quia eveniet at labore cupiditate inventore. Veritatis qui reprehenderit qui alias cum nobis soluta.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...