Why is UBS doing so badly this year? (With Data)

Can someone explain how UBS is managing to perform this badly, especially after integrating Credit Suisse and poaching senior bankers from Barclays? I mean, they had all the pieces handed to them, and yet here they are, underperforming the market. How do you botch such a massive opportunity this badly? (Genuinly curious as to the reasons is it culture, bankers, hires, exposure etc.)

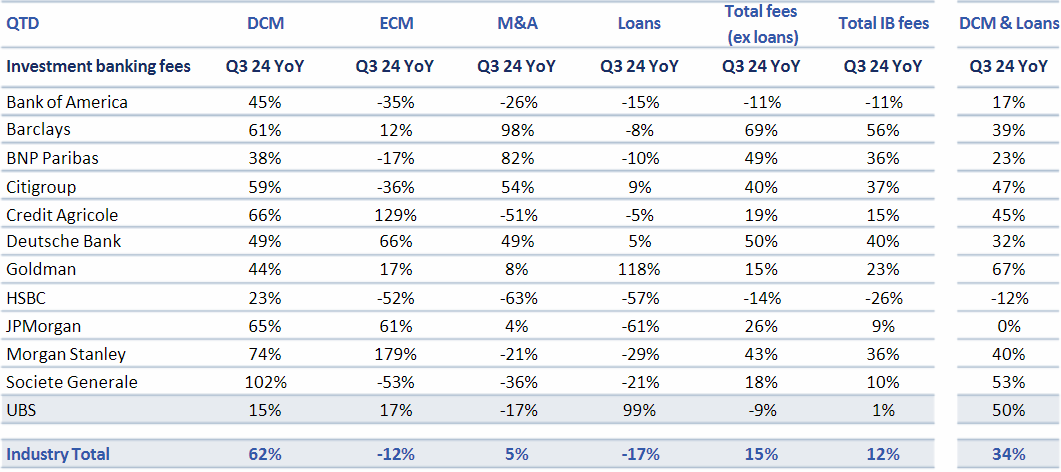

Q3 YTD Investment Banking Fee Trends

Dealogic as of 13th August 2024

Interested

Thats why they market senior headcount and hiring versus fees

This is quarter to date not year to date. It says it on the top LHS

so your thesis is great bank, bad quarter? I don't buy it

It’s a month and a half of data if through August 13

By your logic GS has fell off and been replaced by barclays

"management provided some reassurance at Q2 that the IB pipeline at the start of Q3 has seen positive momentum, but execution of the pipeline depends on market volatility"

So they are going to start to say their pipeline is fantastic and the numbers you see are because of market volatility, sounds like a scapegoat

Hmm we’ll see. I think 2025 will be a great year with rates lower and the election behind us

Bump

there is a lot of hung deals on the platform. things keeping people busy but with low chance of closing. a lot of the big wins from spring summer are processes that got zero bids or 1 low ball one that doesnt work. or the client is facing some litigation/financials are getting worse so buyers are all stalling.

trust me i have visibility on this.

theres been some slide marco and team have shared showing our "huge" successes vs last year but the slides clearly are comparing UBS pre CS to UBS post merger so its actually not good at all. If you nearly double headcount and absorb a franchise and only get IB revenue up 10-20% it likely means things are flat or actually down if just comparing to UBS pre merger.

a ton of hugely important pitches that have sucked up time and most have been lost despite senior banker involvement.

UBS will still be ok because of the WM success, but IB is not doing well.

Good perspective

exactly.

even worse is there are a lot of people on the platform with guarantees for this upcoming bonus cycle. if you don't have one, expect a 40 to 65% bonus at best.

In baseball terms sounds like they should be going for more singles and doubles ($100mm - $750mm deals), versus hitting the home run ($5bn deals)

If you always go for a home run you’ll end up striking out a lot. I think they are going for big deals because all the decision makers have guarantees (cough cough Barclays) so revenue doesn’t matter and they want to elevate their own personal notoriety. Seems like their personal ambition is selfishly hurting the rest of the bank (non guaranteed normies)

A variety of factors with each impacting to a varying degree:

1) integration is very distracting, teams focus is on org structure, process and personnel which is time could be spent with clients

2) Tech should be ~40% of the fee pool and the team is still building and just isn’t getting it done even with 20+ MDs in the Americas alone

3) Experimenting with the strategy to go up market suddenly is very hard and likely different than previous UBS/CS/Barclays individual strategies

4) UBS wasn’t able to keep CS revenue generating people fast enough before they went elsewhere

5) Actively demoting, firing existing UBS power structure to consolidate Barclays power in the bank

6) UBS will never pay a rainmaker a straight percentage of the revenue he/she brings in, those you generally attract are younger or underperforming MDs who are ok with the structure

7) Culture shift from one of merit to one of Barclays-ism where how close you are to the new decision makers in each group matters more than straight performance with more time spent on internal politics than external deals

8) A bit of randomness with bad luck with companies with low odds of winning coming to market, versus companies with better odds of winning not coming to market

They’ve tried to mitigate this by dramatically opening up the loan book and taking more risk, but even then still not enough to compensate for the combination of the above factors

Given these results maybe at the end of the day Barclays was right in not promoting Marco

True?

As long as the investment bank isn’t glaringly bad that’s good enough for UBS and not the banks focus

Would double check your numbers to make sure it’s encompassing all the regions or if you’re only interested in Americas then would show that. Looking at just M&A from dealogic shows 19% increase YoY for the first 8.5 months in of 2024 (9/15/24). That number is actually 23% for just Americas

again, this is INCLUDING another IB on the platform. only up 20+% is pathetic

Don’t know if the prior years numbers are pro forma for CS but wouldn’t be surprised if they were since deal flow evaporated after the collapse in March. You’d have to compare the YTD to 2022 when both banks were more normal

What is that relative to the fee pool? Expenses definitely went up higher than 20%

Also these are published results, not derived

?

Solid analysis there and very on brand for the typical LF banker. Not even gonna ask where the 60% came from

Damn wtf Barclays really killing it right now

For real. Been seeing them on some massive mandates recently. Verizon-Frontier, IBM Hashicorp, CVC-Epicor

What’s the verdict on prospects looking to join versus top BB / EB (Europe)?

Europe UBS has historically been much stronger than the US relative to peers

What are they in the US league tables this year?

Q4 league tables loading

Quam qui nihil ut et. Sed saepe non voluptatem. Soluta in iusto dolorum voluptas inventore. Cum animi in asperiores voluptate provident saepe. Quas aspernatur sit molestiae vel consequatur voluptatem quis. Magnam unde recusandae nam voluptatem cum neque.

Pariatur minus omnis laborum sapiente fugit voluptatem. Consequatur totam et amet optio.

Temporibus pariatur sed hic veritatis reprehenderit quam. Dolores in quae earum aliquid ullam. Nobis ratione enim et consequatur molestias. Cumque dicta eos qui quod sit adipisci aliquid laboriosam.

Libero ea consequatur iusto rerum. Porro vel dolores magni ipsum. Harum consectetur et a. Harum rerum provident exercitationem. Distinctio hic velit recusandae nostrum.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Non quia velit tempore nostrum cumque. Qui non magnam ullam doloremque voluptatem eos doloribus. Sunt consequuntur eum aut. Aut commodi velit consequatur sunt accusantium et. Vel alias voluptatibus qui ad blanditiis pariatur aspernatur.