It's been awhile since I've done a WSO CDO update and a few of you have asked me about it, so when I saw this article about hedge funds and family offices moving into P2P lending with big money I figured it was as good a time as any to do an update. But first, the hedge fund stuff.

It's no surprise to anyone familiar with peer-to-peer lending that institutional players would get involved at some point once the investment strategy proved out. Beaumont Financial Partners of Boston has committed $1 million to Lending Club investing, and based on their anticipated return of 6-7% they're only buying the cream of the crop. In my experience, that type of return comes from A1 and maybe some A2-rated notes, so very low risk as far as P2P lending goes.

Another interesting development is that they made the investment through LC Advisors, the division of Lending Club set up to handle accounts for institutional players. LC Advisors currently has $85 million AUM. If these numbers sound really small to you, it's because they are. But P2P lending is still in its infancy, and is just learning to crawl at this point. If you have any doubt that crowdfunding of all types is the wave of the future, I'd direct you to the JOBS Act. P2P lending alone is quickly approaching the $1 billion mark.

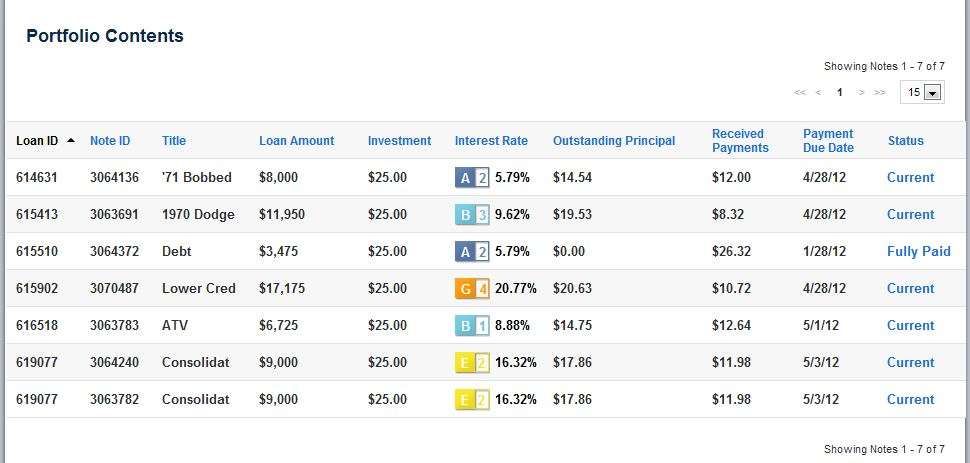

As for our little CDO, we made some big changes in the first quarter of 2012. First and foremost, we shed three of our ten notes. One of them was paid in full. It was an A2 rated note paying 5.79%, so having it pay off early actually improves the nominal ROR on the rest of the portfolio. The other two notes were sold for a slight profit when they were late (or missed) a payment. This has been my strategy throughout all my different LC portfolios. Here's the current breakdown:

As you can see, we're making 11.93% on this portfolio, so it's not too shabby.

I also decided to give Lending Club a shot at picking some notes for me. This isn't a long-term strategy for me (I'm way too anal to let somebody else choose my investments), I just wanted to compare Lending Club's results against my own. So far that portfolio is earning 12.73% and there haven't been any delinquencies or defaults, but keep in mind it is a very small part of my overall P2P investment. More curiosity than anything else.

Finally, my primary portfolio is posting a 14.17% NAR, and to date (18 months in) I still haven't had any delinquencies or defaults. I prune a note or two each month and sell them on the secondary market when they're late on a payment, and I generally sell them at a break even or single-digit profit after fees. I'd really like to have some data on what happens to them after the sale so I could determine whether it pays to be a little more lenient, but as it stands I'm not comfortable giving second chances and I expect to be paid on time. For those curious, I add to the portfolio each week.

If you have any questions, hit me with them in the comments.

You've had this CDO account for 18 months....how have taxes come into play?

very interesting. did some research on this for my boss. check out the german p2p lending sites smava and auxmoney

Eddie, any chance you will lateral to these hedge funds to share your investment strategies or oversee their p2p portfolios?

I think this is interesting, but looking at one CDO is such a small sample size to really get any idea if that rate of return is meaningful.

What happens when 5 years into the investment, 3 of your notes default? Or what happens if you got lucky and picked a great portfolio this time around and when you increase your investment from $100 to $10,000 your effective rate of return actually drops to 2%?

Not trying to sound like a downer, juts curious if there are some overall metrics that Lending Club shares on overall # of defaults over the life of these loans (or % of defaults) in the various groups so that you can get a better idea if you're outperforming or underperforming at any given point. Yes, you can sell them when they miss a payment, but how would you be making a profit every time on the secondary market if this was the case? Is it just not efficient enough yet?

Thanks, Patrick

https://www.lendingclub.com/info/demand-and-credit-profile.action

@Unforseen - The tax ramifications are handled the same as interest income.

@M Friedman - Not sure if you're being serious, but it would have to be a pretty ghetto hedge fund to be looking for my advice.

@Patrick - I run into this every time I publish an update. The WSO CDO was all for fun and isn't really illustrative of any consistent pattern in P2P lending. As far as market efficiency in the secondary market, you might be right about my exploiting a current inefficiency. But that's a big maybe. I'll explain:

When someone misses a payment, it shows up in the notes for that particular loan before there is any status change in the note. After a few days the status will change to In Grace Period (a 10-day period they have to bring the loan current), but initially the loan status remains Current for several days. When I list the note on the secondary market, it gets listed as a Current note (obviously the most sought after loans), so maybe buyers aren't doing their research and drilling down to see that a payment has been missed. Or maybe they're chalking it up to an explainable error (bank overdraft, etc.) that will be rectified in a few days. I don't know.

Also, I price the loans I sell on the aftermarket just above my break even. In other words, the note might be paying 15% interest, but I'll price it to sell 5% above my breakeven so the buyer is looking at a ROR of over 20% (does that make sense?). So I might only make 5% after fees on a note I was supposed to be making 15% on, but I get a potentially bad loan off my books. The buyer gets a seasoned loan at a 20%+ interest rate, so I guess it's worth the risk for them.

I had one loan that went into delinquency (10-30 days late), got the status change, and was unsaleable. About a month later the guy brought the loan current. The status of the loan went back to Current and I was able to sell it for $5 more than I had it listed for a couple days earlier. I guarantee this loan went into default sometime after I sold it.

As for being able to analyze credit risk, etc... there really is a wealth of information on Lendstats.com. Pretty much any analysis you want to do can be done there backwards and forwards. As for Lending Club, they say the best and most stable rate of return comes from a portfolio of 800 notes ($20,000 at $25 apiece).

Thanks Spaceman...based on those #s, it's obviously still way too early to tell what the ACTUAL rate of return will be for the full portfolio once realized to maturity.

or am i reading that wrong? wouldnt a cohort analysis be much more useful here?

https://www.lendingclub.com/info/statistics-performance.action

Actually, Lendingclub also has a custom date range function for their returns page. Provides an easy way to conduct the cohort analysis.

Thanks - I think it's pretty scary unless you look at the older cohorts to see the true rate of default over time...another interesting question...what is the average and mean time a loan actually enters default? year 1, year 4?...

EB finally the post I was waiting for!! Two quick questions:

1.Expanding on Patrick's point, can you do any arbitrage on the secondary market? 2.Any correlation between type of loan and defaults?

Thanks :)

As far as arbitrage goes, the most obvious form of arbitrage in P2P lending is known as "blending". This is when you borrow from Lending Club (for example) at 6% and turn around and lend the money out at 16%. I haven't given any thought to arbitrage on the secondary market. In fact, I've only used it to sell notes; I've never actually bought a note on the secondary market.

I really can't speak to a correlation between loan purpose and default because I use a really strict criteria for selecting the loans I invest in (90%+ of my overall portfolio is credit consolidation loans - in other words, using the loan to retire credit card debt, etc...). I'm not interested in funding anyone's wedding or vacation. I suspect those types of loans have a higher incidence of delinquency, but that's just a guess on my part.

Is this legal? If so, it sounds like a really good way to build the house of cards I've always dreamed of.

I've got a fair amount of money in LC as well, so thought I'd chime in with a few additions:

https://www.lendingclub.com/info/download-data.action

Downloadable dataset of funded loans. For the number crunchers out there, definitely some nice gems and nuggets that can be mined out of there.

Cohort Analysis: Great point on the cohort analysis. Lendingclub's earliest set of loan data goes back to 2007, so it is possible to do some rough analysis by cohort.

I did a rough look at the 2008 cohort of loans ($13.5M in funded loans across 1580 loans). - 18% of loans by value has defaulted or has been written off ($2.5M) - Based on simple interest calculation (too lazy to do any other way),, the performing loans have generated $4.3M in interest to 12/31/2011, or 9.6% per year - Net annualized return would be in the 4% range - Keep in mind this calculation understates net return, since the defaulted loans were assumed to have no interest earned at all. 2008 cohort was probably also a pretty bad cohort given the 09 shocks.

2009 cohort - $47M of funded loans, 4700 loans - 10% of loans by value written off to date, $4.8M of loan value - Simple interest to date of $10.5M, average of 10.6% per year - Net return to 12/31/2011 of 5.9%

Loan purpose: - Do not invest in (1) education, (2) small business, or (3) renewable energy! By loan purpose, these are the top 3 defaulting categories (15% default rate, 12%, and 9.55 respectively). For some reason, these loans have not panned out over time. Granted education and renewable energy has small sample size bias (400 total loans to date).

Here's a pretty cool tool a reader just pointed me to:

http://lucrativelending.com/nickel-steamroller-lending-club-portfolio-a…

Just saw there was an update about 2 months back. Just want to report that my initial investment of ~3k in 130 notes is still holding steady with a 9.39% net annualized return. I have about $700 in principal still outstanding, and $570 in interest received to date. By the end of the year, all my notes will be at maturity or only have a tiny amount of principal left.

Considering the market's behavior over the same period, and the "slow and steady" rate of returns, I plan on reinvesting a considerable amount.

Dawg this post is 12 years old...

Magnam impedit aut est velit error dolor. Mollitia quia dignissimos totam suscipit. Est eos qui minus eligendi in. Similique sint autem quia possimus labore iure quidem.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...