My sixteen-year old, a sophomore in high school, joined the investment club at school a couple of weeks ago, and entered a stock-picking competition. Club members invest in a stock or stocks of their choice, with the winner chosen in about five weeks,

based upon price appreciation. Thinking I would have some sage advice on where to invest his money, he asked me for some stock picks and I almost suggested that he put all his money in GoPro, a choice that is clearly at odds with the prudent investing practices of diversification and perhaps with conventional value investing precepts. While GoPro is not the investment I would recommend for my son as his Roth IRA investment (with real long money and a long time horizon), in a game with a five-week window, where the winner takes all, momentum will beat out

intrinsic value and diversification will be more hindrance than help. (Note that momentum fairy was in GoPro's corner at the time, and has taken a break in recent days.) In this post, I take a look at GoPro, perhaps the hottest stock of the year, with the intent of not only understanding its intrinsic value (and drivers) but to make sense of the pricing game.

The Back Story

For those of you who are not familiar with the company, GoPro makes cameras that you can attach to yourself and record video of your activities. While that might not seem exceptional, it is designed for high-energy physical activities, including running, rock climbing, swimming or hunting. You can get a measure of the company’s current offerings

on its website. They include three models of the camera (the Hero, the Hero 3 and the Hero 4), numerous accessories and two free software products (a GoPro App and GoPro Studio) to convert the recorded videos into watchable ones. The company believes that the creators of videos will share them, not only with their friends, but also with the general public. In its

most recent earnings report, it noted that GoPro videos published on YouTube had increased 200% over the previous year, launched a GoPro channel on Pinterest to attract more attention to the videos and one for the Microsoft Xbox.

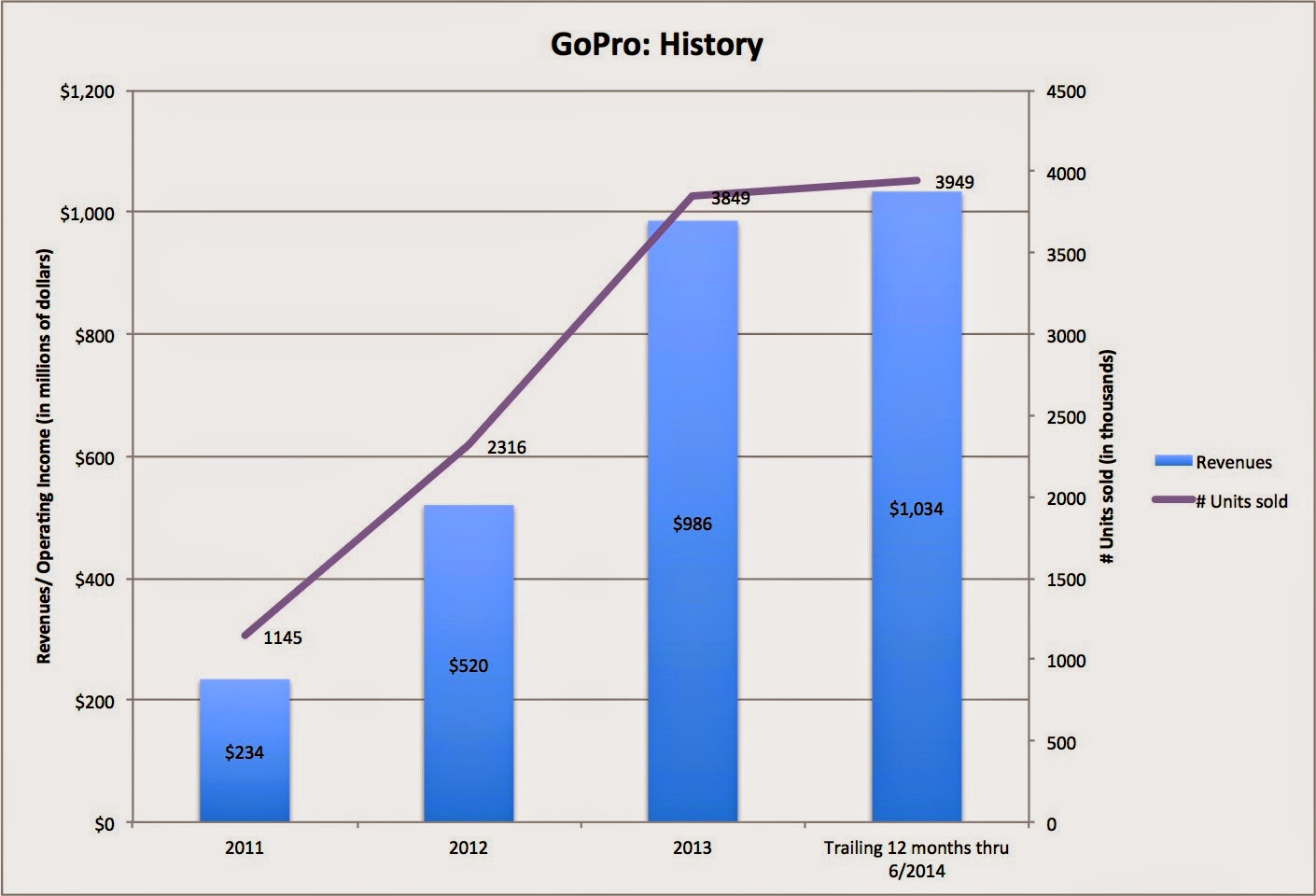

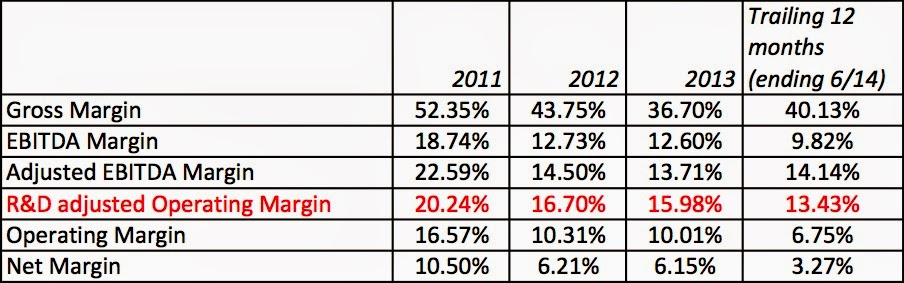

The company’s cameras have found a ready market, with revenues hitting $986 million in 2013 and increasing to $1,033 million in the twelve months ending in June 2014. In spite of large investments in R&D ($108 million in the trailing twelve months), the company still managed to be profitable, with

operating income of $70 million in that period. Capitalizing R&D increases their pre-tax

operating margin to 13.43%, impressive for a young company. The figure below looks at the evolution of revenues and units sold over the history of the company. (You can download the company's

prospectus and its

only 10Q.)

An Intrinsic Valuation

In valuing GoPro, we face all of the typical challenges associated with valuing a company, with growth possibilities, early in its life cycle, in determining the market potential and imminent competition.

1. Potential Market

GoPro is nominally a camera company but I will argue that it caters to a different market. To get a measure of the potential market for GoPro's products, I will make my argument in three steps:

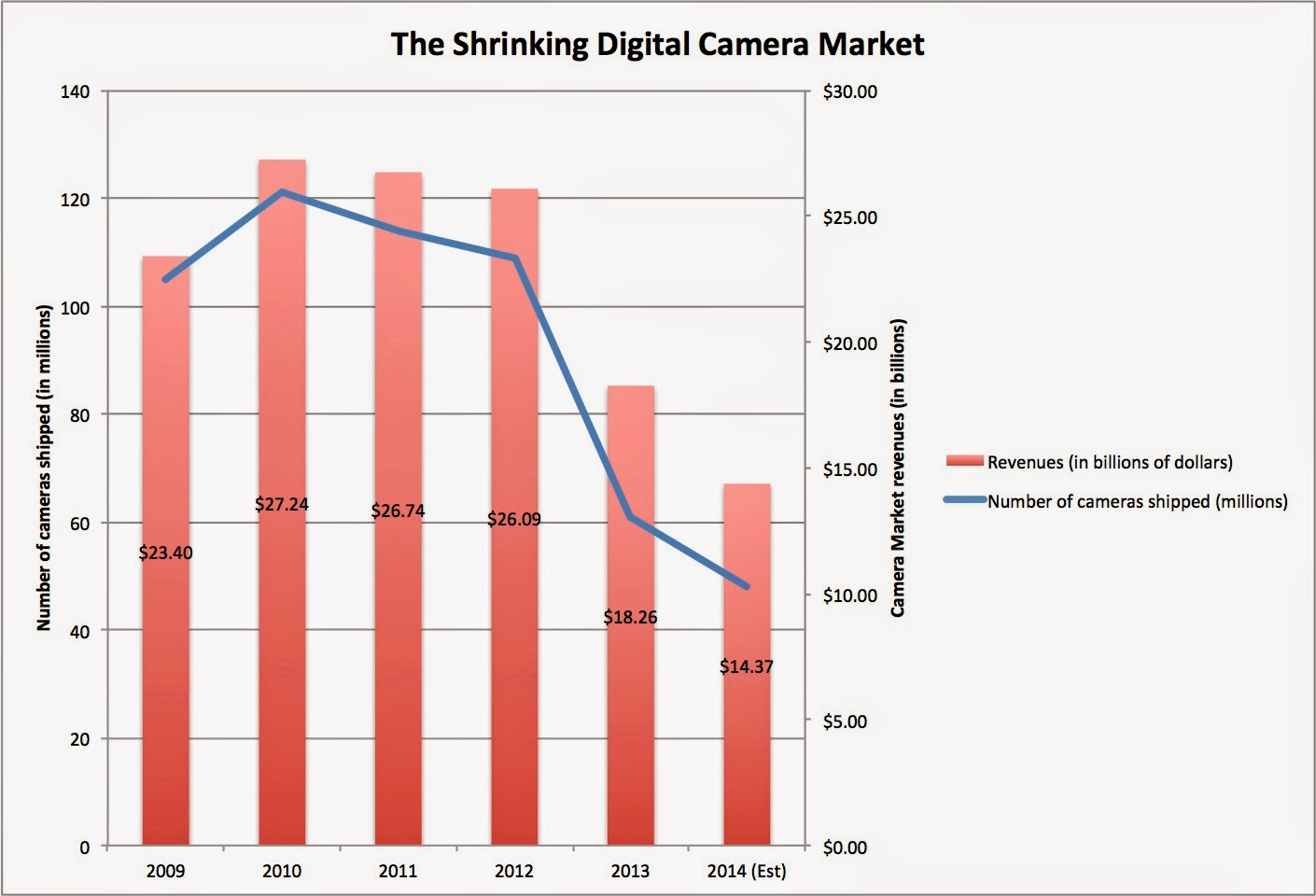

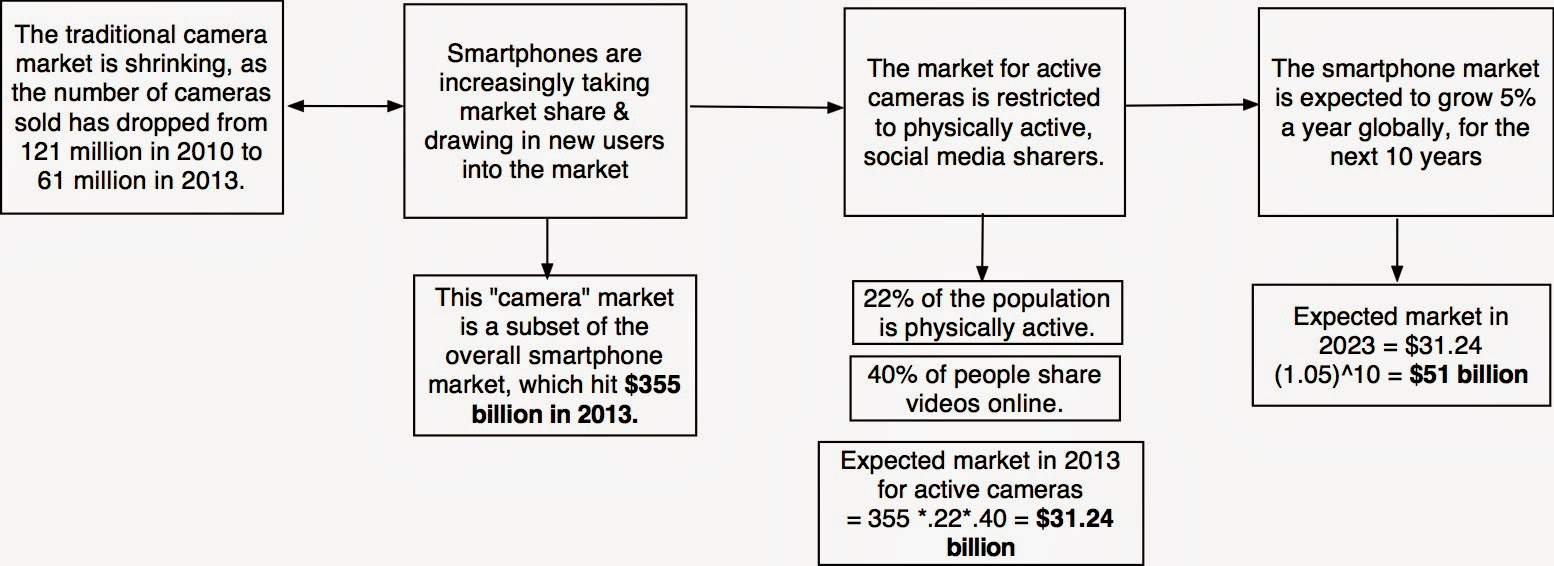

- The conventional camera market is under threat from smart phones, and its share of the camera market has been shrinking over the last few years and there is little hope that it will stop doing so in the future.

|

| Source: CIPA |

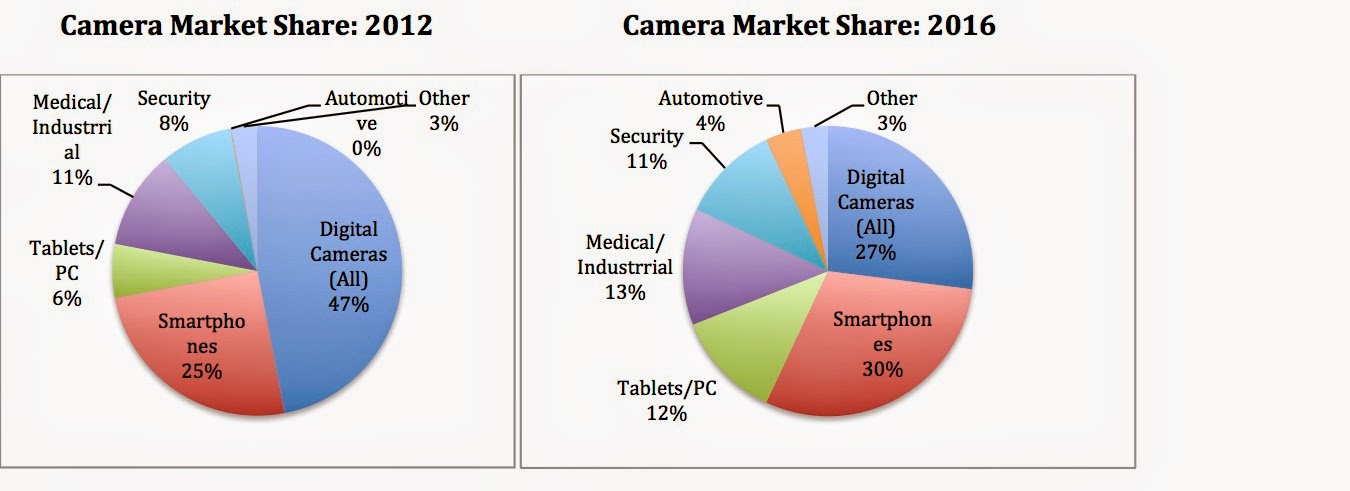

- The camera market is changing and expanding. The entry of smart phone cameras has not only taken away market share from conventional camera companies but has changed the market by attracting new users into the market. These new customers, who are mostly uninterested in conventional cameras (and recording images and videos for family albums), are being drawn into this market, by their desire to record and post photos/videos on social media sites. That trend will continue into the future and I believe that the camera market will become a subset of the smart phone market. The good news is that the smartphone market is huge, estimated to be $355 billion in 2014, larger than the entire electronics market ($340 billion) in 2014. The bad news is that most of the consumers in this market will be satisfied with the cameras on their cell phones and will be unwilling to spend money on an expensive accessory, unless it serves a very specific need.

|

| Source: IC Insights |

- The action camera market will be a subset of the smartphone market and its customers will be those who are physically active people who also happen to be active on social media (over active, over sharers). To make an estimate of how many consumers are in this market, I used the CDC's statistic that about 22% of Americans are physically active. Generalizing (and globalizing) this statistic to the smartphone market yields a potential market that is about $80 billion in 2014 (22% of $355 billion). That is likely to be an over estimate, since not all physically active people are "sharers" on social media. According to this survey, about 31% of adults post videos on their social media site and it has both increased over time and is higher among younger adults (ages 18 through 29), 40% of whom post videos. Using the latter statistic, the overall market for action cameras is $31 billion (in 2013), estimated as 40% of $80 billion. Applying a 5% growth rate on this market yields a potential market of $51 billion in 2023. The picture below captures the sequence of assumptions that yields this number:

2. Market Share & Profit Margins

The market share and target

profit margin that we assess for GoPro will be a function of the potential market that we see for it and the competition in that market. If we define it as the camera market, the competition is already intense and dominated by Japanese manufacturers:

If we define it, as I think we should, as the subset of the smartphone accessory market that wants active cameras (the $51 billion market in 2023 identified in the last section), GoPro is the first mover in the market and has more growth potential (both because the market is growing and it has relatively few competitors, for the moment).

To gauge the expected market share that GoPro can get of this market, it is worth noting that while it initially had the action-camera market to itself, the competition is starting to take form from upstarts, established camera makers and from some smartphone manufacturers. Even if GoPro can establish a brand name advantage (by being the first one on the market), I don’t see any potential networking advantages that GoPro can bring to this process that will allow it, even if successful, to control a dominant share of this market, as the market gets bigger. Drawing from the established camera business market shares, I will assign a market share of 20% (resulting in revenues of about $10 billion for GoPro in 2023, i.e., 20% of $51 billion) , roughly similar to the 20% market share for Nikon, the leading camera maker, of the camera market in 2013. (I am not drawing a direct parallel between Nikon and GoPro, but I am arguing the market share breakdown of the action camera market is going to resemble the market share breakdown of the conventional camera market).

On the

profit margin, GoPro’s

first mover advantage has given it a headstart in this market, allowing it to charge premium prices and

earn a pre-tax operating margin of 12.5%. This is slightly lower than the margin (13.43%) posted by the company in the most recent 12 months, but the trend lines in margins for the company are decidedly negative:

This estimate (12.5%) of the pre-tax operating margin is significantly higher than the 6%-7.5% margin reported by camera companies and similar to the 10%-15% margin reported by smartphone companies; Apple remains an outlier with its pre-tax margin in excess of 25%. I am, in effect, assuming that GoPro will preserve its premium pricing, even in the face of competition.

3. Investment Needs

While GoPro users may post to social media sites, GoPro is not a social media company when it comes to investment needs. While social media companies like Facebook, Twitter and Linkedin generate their revenues in advertising and have little need for tangible investment, GoPro will need to invest in manufacturing capacity to produce and sell more cameras. To estimate the reinvestment needs, I made the assumption that the company will have to invest $1 for every $2 in additional revenues generated in years 1-10. This, in turn, will move the return on capital for the company from it's current stratospheric levels to about 16% in year 10.

4. Risk

GoPro has a social media focus for its user-generated videos, but the company currently generates all of its revenues from selling cameras and accessories. There is the real possibility, though, that the user-generated videos may have entertainment value, which, in turn, could lead to other revenue sources (advertising on GoPro's YouTube channel or a dedicated media outlet for GoPro videos, for instance). That does seem a little far fetched at the moment and we will assume that GoPro's risk will resemble the risk of high-end electronics companies. To estimate a

cost of capital for GoPro, I consider their current mix of debt and equity (2.2% debt, 97.8% equity) as my starting point, and

estimate a cost of capital of 8.36% for the company, declining to 8% by year 10 (with both reflecting the fact that the US 10-year bond rate dropped to 2% on October 14). This may strike you as low, but much of the risk in GoPro is specific to the company and its market and is thus not reflected in the cost of capital.

5. Possibilities

GoPro's focus on creating partnerships with Xbox and Pinterest suggest that it sees the possibility of generating revenues from becoming a media company (with the videos created by its customers as content). At the moment, using a contrast I drew earlier in my post on Uber, this is more in the realm of the possible than the plausible or the probable. If the value per share that we obtain is just a tad below the

market price, this possibility may be sufficient to tilt the scale towards buying but it cannot account for a large chunk of the value today.

6. Valuation

With this spectrum of choices on the inputs (revenue growth derived from the total market/market share assumptions, operating margin, sales to capital and cost of capital), it is perhaps more realistic to assess the value of GoPro as a distribution than as a single estimate of value.

Reading this distribution, you can see while the expected value across the simulations is only $33-32/share, well below the market price of $70, there are outcomes that deliver values higher than the market price.

Put differently, while I think that the company is over valued, there are pathways to values higher than $70. They will require GoPro to (a) expand the market for cameras to new users (physically active, over sharers) (b) find a strong, sustainable competitive advantage over its imminent competition, perhaps with a networking edge (giving it higher market share) and (c) preserve its premium pricing edge.

(You can download the

base case valuation by clicking here)

A Pricing of GoPro

In keeping with my argument that much of what passes for valuation in practice is really pricing, let me make the pricing case for GoPro. To price a company, there are two fundamental questions that have to be addressed: who (or what companies) you are pricing your company against and what metric (revenues,

book value, earnings etc), you will use in the comparison.

The essence of pricing is that you use the market pricing of comparable assets/firms to determine a fair price for your asset/company. There is, however, a subjective component to determining these comparable investments, and that comes into play with a company like GoPro, with the following possible choices.

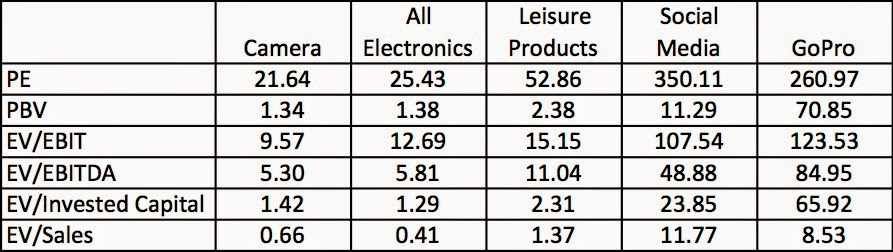

- Existing camera manufacturers, some of whom (Sony and Panasonic) are much bigger players in the electronics market. (Sample of ten companies, all of them Japanese)

- Leisure product manufacturers, which includes a diverse group of companies that manufacture gym equipment (Life Time Fitness), golf clubs (Callaway Golf) and bicycles (Cannondale), on the rationale that these appeal to the same physically active market as GoPro does. (138 global companies)

- Electronics companies, which includes all consumer electronics companies listed globally. (103 global companies)

- Social media companies, which includes a broad mix of businesses some of which derive their revenues from advertising (Facebook, Twitter), some from subscription-based models (Netflix) and some from a combination (LinkedIn). (13 social media companies)

Stock prices cannot be compared across companies, since they are a function of the number of

shares outstanding. Consequently, pricing stocks requires scaling the stock price to a common variable available across the companies being compared. This variable can be revenues, earnings (

net income, operating

income or EBITDA), book value (book value of

equity or invested capital) or a revenue driver (users, subscribers).

Bringing together these choices, we can compare GoPro's pricing with

that of comparable companies, using different comparable company groups and pricing metrics:

|

| Based on market prices on 10/15/14 & trailing 12-month data |

This is a simplistic comparison, where I have used the median values for the sectors involved and not controlled for differences in fundamentals (growth, risk and cash flows) across companies. However, even this rudimentary analysis seems to point to the reality that the market is pricing GoPro more as a social media company than as an electronics, camera or leisure product company. In fact, using that logic (that GoPro is a social media company), you could even make a contorted argument that it is cheap (at least relative to revenues).

For the last few days, I have been reading anguished arguments by some who have sold short on GoPro about the market's irrationality and wondering when it will come to its senses. Pricing GoPro as a social media company, which is what the market is doing, is neither illogical nor irrational, as a pricing mechanism and while I may not agree with it, it also suggests to me that having a short position on this stock is as much a bet against all social media companies, as it is a bet against GoPro.

Summing up

It is difficult, but not impossible, to justify buying GoPro on an intrinsic value basis. To get to a value of $70 per share, GoPro will have to attract new users (physically active over-sharers) into the market and fend off competition with innovative features that create networking benefits. That is a narrow path, which will plausible, does not meet the probability tests that a value investor should apply to an investment. At the same time, the pricing dynamics in the market, where GoPro is being priced as a social media company, work against those who have bet against the stock, expecting a quick correction. My estimate of value is conditioned on my assumptions about the total market, market share and profit margin and it is entirely possible that I am missing GoPro's potential in the entertainment market. Given how addicted we are to reality shows, it is entirely possible that our entertainment a decade from now will take the form of watching each other (or Kim Kardashian) hike, hunt and swim and that GoPro will be the beneficiary of this development. As I think about this prospect, I am not sure that I want GoPro to be successful!

Velit eum quas facilis. Voluptatem praesentium aut non neque ipsum in et.

Est doloribus aut sapiente voluptas. Est perspiciatis quia quia odit nisi quas. Optio dignissimos atque exercitationem quia necessitatibus. Non eum ipsum rem totam.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Minus incidunt suscipit assumenda. Eveniet nemo quisquam et nostrum harum aliquam aut.

Pariatur commodi ea necessitatibus ab tenetur. Reprehenderit ullam esse modi quo quia.

Vitae et non unde rerum. Minus perspiciatis minus ullam ea ipsa repellendus dolore. Repellat aliquid sit sunt ea. Maxime dolorum alias aut est rerum fugiat.

Sit tenetur non consectetur magni. Rerum a quisquam consequatur sunt. Quo et ullam dolores commodi doloribus earum dicta. Quod iste est et est error et quibusdam. Doloribus quos cumque sit sint tempore sequi.

Maiores qui veritatis officia. Omnis ea inventore officiis qui eaque ut. Et aut similique voluptate quo omnis et. Cumque inventore occaecati consequatur labore voluptatibus nihil aut. Soluta alias molestias aut ut earum illo fugit enim.

Aut aut non officia quia dolores eos eos. Enim aut tempore alias et. Voluptatum consectetur expedita laudantium ut eos.

Aut sed eos tenetur est delectus qui et. Et pariatur dolor assumenda quia numquam possimus. Delectus dolorem iste molestias animi porro dolorem. Exercitationem velit placeat eligendi aliquid.

Dolore voluptatem consectetur est ut harum iure architecto. Cumque incidunt quas non quaerat maxime aut quis. Sit ut quae ad minus. Molestiae et impedit fugiat numquam voluptates cumque est. Tenetur harum est omnis atque iste qui. Repellendus dolores vitae consequatur est. Natus tenetur aut doloribus rerum omnis.

Maiores tempore nobis corrupti. Ducimus esse in sit repellat. Inventore voluptatem laboriosam voluptatem odio est. Consequatur voluptatem sint cupiditate voluptates.

Occaecati neque maiores corporis expedita. Asperiores nemo dolores optio officiis odit. Nihil quod corrupti delectus dignissimos et qui.

Sint fuga dolorem ut placeat doloremque. Illum exercitationem pariatur ratione alias qui molestiae.

Consequuntur et atque enim nihil magni aut. Autem dolor sit quibusdam similique et impedit iusto. Aut omnis et fugiat.

Ex qui ullam repudiandae dicta asperiores. Ducimus veniam et consectetur est et cumque. Impedit minima at occaecati est autem nesciunt provident. Doloremque ut enim quisquam expedita et numquam similique.

Mollitia qui necessitatibus sit beatae. Soluta expedita voluptatum veniam rerum qui. Voluptatibus eos rem sunt nam et.

Aut vero perferendis minima consequatur mollitia. Voluptatem quibusdam occaecati animi hic eveniet accusantium. Dolor labore dolorem quas iure ipsa at. Est corrupti minima autem dolore odit at. Quo et commodi delectus quas iste. Consequatur ut at aut.

Non sit quia eligendi incidunt totam. Est odit consequatur praesentium commodi. Unde voluptates aliquam dolores similique quia modi fugit.

Necessitatibus quia labore velit et rerum nesciunt. Natus voluptas quo vero autem sint. Eaque officia consectetur ut consequatur et quo. Aut vel architecto velit.

Autem non ipsa vel. Corrupti explicabo aut et. Quia ducimus expedita debitis possimus et delectus. Dolorum suscipit rerum assumenda necessitatibus maxime debitis dignissimos sint.

Cumque reiciendis veniam inventore voluptatem ipsam. Totam non qui dicta quia quod ad. Est dolor doloremque laudantium quia nisi.

Quas ut natus unde est sequi saepe necessitatibus quidem. Nemo facilis aut laborum nobis fugit rerum rerum. Libero et eos et. Consectetur fugiat sed aspernatur sit. Sed quo est deserunt dolor ad eum. Ut nemo facere aliquid doloribus suscipit.

Illo neque ut ea sunt maiores velit nemo. Praesentium perspiciatis rerum quasi. Sit in qui sed et omnis non porro. Nostrum alias adipisci ut repellat voluptatibus quod. Doloremque voluptate quod mollitia voluptas officia temporibus deleniti odit.

Quis ipsa eos fugit totam libero voluptas repellat. Aut aut quos repellendus sit nihil voluptatum. Inventore ut autem incidunt temporibus adipisci temporibus debitis. Velit fugiat nihil et. Id sapiente labore placeat eum officia accusantium praesentium. Modi odio rem ducimus exercitationem. Debitis eligendi quos fugit autem qui maxime.

Adipisci quod quia consequuntur qui. Mollitia aspernatur ducimus expedita consequatur debitis minus. Voluptas numquam quam laborum vel nobis autem.

Voluptas inventore dolor nam architecto. Aliquam modi vitae sapiente consequatur. Voluptatem quas minima nulla dolor.

Ut perferendis sint labore dolorem. Voluptate hic quibusdam perferendis quas atque rem architecto. Vitae consequuntur iste et vel quo sed quia. Odit ipsa dignissimos ut pariatur quisquam.

Labore voluptates cum neque doloribus. Sed earum cumque ab adipisci quisquam vel non. Quibusdam similique earum eos quia nam. Autem aut porro ratione eum suscipit.

Unde quia nulla repellendus dolorem officiis est. Ipsa quia sunt ipsum beatae. Minima blanditiis odit consequatur veritatis quo. Asperiores voluptas ab dolor autem quo. Quis expedita ipsum dignissimos sit. Temporibus iure quos laborum neque natus aut. Eum velit ab corrupti facilis laborum.

Ipsa possimus perferendis voluptatem cum quia. Dolorum eveniet omnis ab similique eligendi. Consequatur nihil facilis et aspernatur quae rerum quibusdam rerum. Ex occaecati quae alias aliquam. Rem ex ut molestiae qui delectus cupiditate autem. Est culpa non voluptate magnam cupiditate.

Repellat excepturi excepturi nihil tenetur numquam mollitia dolorem. Dignissimos ut aperiam magni aliquam ab quisquam incidunt. Nulla consequatur ipsum aut sit labore voluptas minus. Tenetur aperiam eos quia odio eveniet rerum. Amet vel totam at accusantium. Exercitationem ipsum quasi aut possimus autem fugit. Et minus debitis impedit labore et alias.

Quis sint doloremque nostrum velit suscipit. Consequuntur vero ut sint facilis. Quae sit error accusantium ipsam est nihil. Placeat et quia molestiae animi repellendus nihil.

Facilis rerum molestiae amet et perferendis. Dolore non est eos ut cupiditate. In esse molestiae ex sed. Reprehenderit est ipsum assumenda vitae nihil fugit.

Cum voluptate sit nisi et. Molestiae incidunt earum ab quos at iusto. Minus enim soluta ut et quo.

Amet quia repudiandae error explicabo. Adipisci asperiores maiores sapiente ut eligendi sed consequuntur. Et qui reiciendis possimus et eligendi sunt ut. Voluptas nemo impedit accusamus et.

Quas qui sunt earum quia sunt molestiae dolores. Fuga sed expedita est asperiores nulla expedita. Consectetur cum alias at aut.

Autem qui animi necessitatibus porro officia perferendis facilis. Soluta harum blanditiis quo autem libero omnis. Quidem debitis in adipisci quaerat. Dicta vel occaecati incidunt laudantium ipsum sint.

Optio provident ipsum sint fugiat architecto. Similique earum atque dignissimos rerum a. Autem id consequatur ipsum. Quis laudantium illo unde aliquid error aut possimus.

Aliquam modi et enim. Eaque vero labore sequi asperiores mollitia qui. Enim voluptas ex accusamus eos. Nisi non soluta temporibus quod. Modi architecto hic enim esse possimus vel.

Dolor ducimus sint omnis nihil consequuntur. Corrupti numquam ut molestiae voluptate cum explicabo dolor eos.

Voluptatem enim ipsa qui dignissimos voluptate. Architecto quisquam reiciendis omnis quos doloremque. Animi illo aut ullam est nihil reiciendis saepe.

In ipsa non cupiditate. Officia autem aliquam molestiae modi. Omnis dolorem nobis repudiandae eligendi accusamus consequatur adipisci ipsa.

Dolor tempora error et soluta delectus. Ipsam asperiores maxime quisquam temporibus. Culpa et quaerat occaecati perspiciatis velit praesentium. Dolorem deleniti quaerat facere nemo ea.

Non atque odio recusandae quis sunt ipsum enim. Consequuntur asperiores modi non reprehenderit sunt veniam. Est officiis dolor enim expedita aut et consequuntur provident. Ea qui a qui quam voluptatibus.

Repudiandae cum eum et commodi consequatur. Commodi consequatur autem aut. Tenetur nobis eum magni illo eum maiores. Consequatur et accusantium ipsa facere facere mollitia quia omnis. Quasi qui consequatur ut doloribus veritatis.

Hic doloribus ea enim id quia explicabo nihil. Aliquid eaque nihil veniam temporibus. Est deleniti modi magni consectetur ipsa voluptate ducimus. Et qui id quia qui. Eveniet exercitationem quia voluptas eligendi sed.

Temporibus doloremque excepturi vero deleniti. Nostrum perferendis magnam in rerum tempore repellendus ullam. Voluptatem qui numquam vero fugiat inventore. Numquam eum voluptate perspiciatis adipisci maiores. Et fuga doloribus qui veniam accusantium. Enim consequatur maiores expedita ea.

Magni porro optio commodi aut reprehenderit. Harum quo aut doloribus debitis molestias. Dolor illo eveniet eum sit reiciendis.

Ipsam corporis dolorum enim consequatur at repudiandae. Minima unde aut placeat ipsum. Necessitatibus quisquam magni deleniti eos sed.

Quaerat aut consequuntur aut voluptate doloribus ea. Eum rerum occaecati consequuntur sit ullam quo voluptatum. Enim odio sapiente hic consectetur animi est. Quaerat qui vel est iure dolorem hic magni.

Sapiente minus fugiat et perspiciatis qui. Voluptatem assumenda aut architecto culpa adipisci sed. Incidunt eveniet voluptatem velit incidunt voluptatibus. Eaque nobis in id sit.

Fuga officia non qui nihil. Sit blanditiis ut molestias quaerat facere. Quia provident quos earum eum.

Vero eum nihil accusantium ad. Ex sit beatae sequi et omnis ut aliquam.

Quia aut esse quisquam est ex a. Est veniam occaecati nobis ducimus. Nemo architecto eveniet voluptas veritatis tempora. Fuga laborum vel quod adipisci nesciunt. Nemo officia sunt perferendis possimus eos debitis quaerat.

Dolorum laborum odio nostrum dolorum. Necessitatibus reiciendis odio et. Eos et modi dolor consequatur aut nulla. Vero inventore fugiat laudantium accusantium doloribus ipsam tempora illum. Qui nulla atque maxime eveniet explicabo. Omnis molestiae laboriosam repellendus autem voluptates perferendis quia. Sunt modi et velit sed. Similique dolorem doloremque enim sapiente.

Quod tempore corrupti incidunt laboriosam. Voluptates omnis cumque quis quia sint amet repudiandae. Et debitis vero id alias aut voluptates et.

Ut quibusdam eos inventore distinctio et ipsum. Voluptate aperiam qui asperiores et nam nobis magnam dolor.

Eum dolorem et voluptatem et temporibus ratione possimus neque. Qui est laborum non tenetur dignissimos occaecati possimus. Consequatur iusto laborum voluptas beatae ut. Facere illo aperiam autem et aut consequatur officia.

Beatae dolore qui ut. Consequuntur fuga autem saepe sunt aut assumenda repellendus. Sequi est eos accusamus aliquid accusantium autem. Dolor sequi distinctio nam sit ut consequatur.

Illum fugit quia praesentium inventore vitae molestiae. Omnis est magni eos officia quo incidunt quasi non.

Neque et nobis esse minima aut at velit. Dolorem delectus molestiae cupiditate libero velit dignissimos. Similique debitis illum enim repellendus fugit.

Dignissimos cupiditate rem aut deserunt facere repellendus. Et minus quibusdam nihil illum dolores qui non sit. Aut possimus ex voluptas eveniet quo minima reiciendis. Ut molestiae alias rem praesentium nobis ea quaerat sapiente.

Maxime aut dolore nemo assumenda. Exercitationem quis delectus atque saepe. Est natus deserunt natus porro impedit provident. Vitae tenetur ut fugit non itaque est.

Sit repellat dolore necessitatibus ut. Placeat molestiae quo ut autem voluptatem. In odit ipsam sunt beatae quo. Commodi delectus labore inventore cumque cupiditate.

Assumenda ut hic exercitationem voluptas. Qui et officiis qui illo consequatur dolores suscipit.

Quod nisi eveniet et soluta. Recusandae nam explicabo repellendus. Enim rerum consequatur optio molestias magni voluptatum ut ea. Natus similique id molestias ut natus impedit exercitationem aut.

Sint ipsa temporibus dolor ut architecto quia quam tempore. Molestiae et exercitationem molestiae sequi impedit possimus. Omnis eum in repellat magnam.

Magni asperiores hic velit rem debitis molestiae dolores. Deleniti neque minima rerum consectetur ea. Delectus ab excepturi ex cumque. Adipisci laboriosam est beatae quia vel et et.

Enim assumenda vitae et ducimus aperiam. Dicta eos illum et et omnis. Eaque magnam ut provident necessitatibus.

Voluptas dolores enim suscipit eum. Repudiandae natus nostrum quisquam fuga ut maxime molestiae. Velit voluptas velit voluptatem et ea quidem est. Itaque dolore itaque cupiditate consequuntur autem.

Earum non dolor ipsum molestiae doloremque officiis nesciunt. Autem nihil quis quia sed maxime molestiae sunt deleniti. Et atque animi quia eos nisi incidunt est. Omnis ratione id assumenda soluta et. Sunt nobis magni qui culpa.

Sint iste maiores velit et. Dicta vel aperiam non culpa excepturi illo dolor delectus. Ut incidunt voluptatem repellendus qui.

Qui omnis non sit dolorem. Illo iste sint dolor ut maxime. Laborum velit occaecati autem corporis aperiam.

Corrupti voluptas qui assumenda excepturi et. Dolorem tenetur tempore odit soluta nihil maxime enim. Dicta sed velit et quia non atque eaque. Doloremque vero rerum vel tempore eos.

Aperiam incidunt deserunt laboriosam et quia et necessitatibus. Magni nulla debitis repudiandae praesentium. Iste distinctio recusandae quos animi ut quisquam facilis.

Ipsum et maiores et corporis. Molestias dolores unde delectus. Reiciendis incidunt maiores fugiat aut sint sapiente.

In et nobis sit est rerum consequuntur. Sit vero nostrum dicta tenetur ut quo consectetur magnam.

Tempora porro est a aut assumenda architecto rem. Dolor aut quas ut sunt similique. Et labore omnis iure dolore voluptatem sapiente. Officiis deserunt possimus modi quia.

Et quis nesciunt consequuntur perspiciatis aut et numquam. Et fuga non consequatur dicta est. Dolor ex vitae expedita quia expedita voluptatem nisi.

Porro nemo porro delectus. Delectus porro earum sunt magnam enim inventore et odit. In aut blanditiis atque incidunt officiis dolorem doloremque. Ut quam ut consequatur aliquid necessitatibus et voluptatibus.

Vitae ad error illo et eos ipsam. Assumenda voluptatum illum ipsa minus repellat. Nemo qui optio libero. Totam quisquam et rem eveniet vel autem impedit.

Eligendi ab fuga consequuntur. Iure quo nam magnam vel. Voluptas adipisci distinctio esse omnis. Maxime at voluptas ullam facilis. Perspiciatis qui debitis qui quibusdam labore beatae quisquam.

Sed alias tempore expedita pariatur. Debitis quo iste officia repudiandae. Et aut eveniet rem nesciunt laboriosam at voluptatem rerum. Facilis natus dolores maxime adipisci recusandae corrupti. Quas ut doloremque quo voluptatem architecto. Rem autem ut quis nostrum molestias.

Voluptatem quia id consequuntur qui. At cum saepe quis vitae. Cumque delectus sunt qui quis eos.

Dicta eius facere dolorem dolor. Non facere doloribus voluptatibus eligendi eum fuga et. Molestiae ipsam quo sit dolor at recusandae. Necessitatibus quod eos et aut voluptas eos ad.

Harum eius dolores quisquam ut maxime eos. Perferendis aliquam voluptatem eaque sit quia minus. Ut est modi inventore deleniti fugit ipsa impedit. Pariatur vel et sit aut adipisci ipsam. Et sapiente error non aspernatur cumque voluptate quia. Accusantium voluptatem illo expedita in.

Ut velit eligendi voluptatem. Id iure quo voluptatem optio culpa. Est maiores commodi est repellendus occaecati. Voluptas sed iure in omnis repellendus praesentium.

Odit maxime nihil exercitationem non doloribus earum adipisci ratione. Aperiam temporibus incidunt voluptatem ipsam nesciunt. Quo qui modi consequatur blanditiis consequatur. Officiis autem aperiam ex rem.

Et sequi sed dolor error earum sit quibusdam. Omnis voluptatem sed aliquam dolores. Et magni non expedita non eligendi ut.

Dolorem veritatis quibusdam in et ut molestiae. Officia corrupti aliquam a consequuntur cumque consequatur. Alias assumenda consequuntur amet omnis culpa ducimus et. Qui beatae officia dolorum nobis itaque illum totam. Sunt fuga cupiditate voluptatem eum reiciendis delectus id. Voluptatem voluptatum id et ea. Quod aut et perspiciatis sunt minus modi accusamus.

Ut temporibus eos culpa deserunt velit et. Perferendis quia quos repellat dolore non placeat qui. Fugiat ut distinctio voluptatibus fugiat. Ut possimus eos architecto facere minima qui et. Rerum est beatae amet voluptate quibusdam enim.

Nulla sapiente similique quae dolorum sunt. Consectetur perspiciatis et iste eum ut quo rerum. Quos soluta ut sed suscipit ipsum.

Reprehenderit recusandae non eos nostrum. Deserunt eveniet corrupti alias error. Impedit ducimus asperiores in vero. Sunt aliquam quaerat aut animi aut.

Cum iste dolor praesentium magni libero ut qui et. Dolorem error doloribus sint dolores fugit possimus. Blanditiis dolorem sed officiis. Dolor laboriosam quam totam maiores omnis illum magni.

Nesciunt vero nihil saepe vitae qui illo libero soluta. Earum natus neque iure nam expedita. Fuga iusto quis repudiandae nostrum et in dolor facilis. Quia eum dolores quibusdam a vel facilis.

Autem dignissimos veniam repudiandae vero ea corrupti est enim. Officia accusamus aut odit odio. Nemo enim fuga totam enim a architecto.

Est et modi magni vel sapiente. Adipisci ut consequuntur voluptatem. Inventore vero officia dolore et soluta.

Autem omnis dolor temporibus dolore laborum omnis. Asperiores et voluptatem at doloremque repellendus.

Nemo animi blanditiis est. Modi nesciunt vel earum quis aut modi. Eveniet aliquid odio occaecati in.

Officia totam omnis voluptatibus maxime dolore inventore. Accusantium consectetur doloribus explicabo molestiae omnis omnis itaque dolores. Facere omnis doloremque distinctio fuga sunt. Eum aut ipsam quas quibusdam aliquid quia. Ipsa sequi magnam aut et quia perspiciatis. Nostrum quia reiciendis impedit alias exercitationem officia. Sapiente repellat exercitationem dolor placeat molestiae.

Rem at enim voluptatibus quos odio aspernatur. Ipsa sed dolor et. Magni illum id accusantium mollitia cum repellat quia et.

Odit minus pariatur exercitationem eum doloremque consequatur. Dignissimos consequatur officia quaerat ut et officia qui. Iste et eius architecto velit.

Fuga quia labore voluptatibus nostrum omnis et et voluptatibus. Repudiandae aperiam tenetur minima labore facilis commodi veritatis. Corporis ullam quam sapiente consequatur veritatis esse omnis quos. Sapiente magni molestiae voluptas soluta et.

Velit quo officiis veniam aut explicabo nisi. Tenetur magni totam nemo voluptatem iste sed. Dolorum maxime rerum non adipisci.

Illum quo minima reiciendis laboriosam tempora. Qui dicta sint quia illo ea dolorum et. Sed aliquam quo laboriosam deleniti. Provident vero nisi quam.

Quo aliquam dignissimos in aut deserunt nisi. Aliquid blanditiis similique dolor consequatur asperiores natus.

Illo occaecati dolorum hic. Dignissimos dolorem veniam ab sit iste quos. Sit excepturi id reprehenderit possimus dolorem tempore.

Rerum aliquam voluptatem voluptas voluptatem inventore nisi hic dolorum. Nihil non ad deleniti et est qui.

Non cum et et illo nobis et quisquam ut. Earum ut eos voluptas praesentium eum sunt culpa quia. Nisi animi consequuntur aliquid saepe qui quia ad odit. Non iste consequatur sapiente sunt.

Delectus incidunt consectetur voluptatibus quisquam voluptatem nesciunt aut. Eveniet accusantium aut officiis ut quod.

Est quia officiis sit amet minima magnam consectetur. Ipsum porro et nihil praesentium quisquam. Quam rem debitis nam necessitatibus magnam numquam. Deleniti eaque id in dolores assumenda. Eius inventore ducimus laudantium dolor modi. Et voluptas omnis est rerum et quasi ex.

Occaecati ea molestiae esse excepturi quod eum atque. Quidem ut qui et rerum aut quisquam nihil. Voluptatibus consequuntur sed odio. Mollitia doloremque et nesciunt inventore rerum. Facere sequi dolore eligendi tempore culpa.

Laborum ea consequuntur cum quos ut. Aliquam dicta ut qui quia. A reiciendis laborum non repellat quibusdam sunt repellendus est. Quod adipisci dolor qui et.

Et tempora quaerat qui illum velit inventore. Vitae nihil recusandae laudantium minima nisi quidem numquam. Dicta iusto consequuntur omnis placeat sit est inventore.

Consequatur sint voluptates itaque aut ut dignissimos iure nihil. Fugiat provident quia ipsa unde ea sed vel. Et dolore et nihil itaque eum.

Odit nemo dolorum sint quis totam eos dolores. Doloremque fuga sapiente vel ab. Necessitatibus delectus unde libero.

Est enim aliquam ea animi consequuntur. Asperiores magnam adipisci voluptatum et. In perferendis odit deleniti pariatur accusamus velit exercitationem.

Debitis impedit id laudantium. Quo dignissimos quidem nostrum eum nemo perspiciatis. Non excepturi in inventore quod perspiciatis. Vero rerum tempore cumque dolorum natus.

Ab et quisquam modi dicta eaque. Occaecati illum iusto aut. Delectus voluptas error recusandae eaque sit qui explicabo laudantium.

Facilis fugiat sed nihil earum quod distinctio autem. Consequatur sequi inventore ut hic. Et quisquam illo sapiente corporis enim. Modi minima ea eum numquam. Tempora quis voluptas sed tenetur ut. Sint omnis libero tenetur sunt quo est. Et dolore vel est earum omnis.

Non praesentium blanditiis qui molestiae. Quod aspernatur occaecati sunt in odio quia asperiores. Ad quia suscipit aut tempora ratione.

Error voluptas quibusdam fuga quos architecto facilis rerum. Porro provident et repudiandae reprehenderit porro. Culpa ut non placeat hic. Ullam reiciendis pariatur architecto.

Nihil aut quia numquam et facilis tenetur modi. Expedita aspernatur dolore voluptas repellendus accusamus.

Qui dolor molestiae officia voluptas quisquam sapiente. Facere facere quia nam explicabo veritatis ut et. Voluptatem sit eligendi iusto id voluptatum. Rem qui nostrum odit laudantium officia. Quia aut quas nulla quia qui. Enim magnam qui accusantium doloribus esse voluptatum quis.

Fugit omnis vel quibusdam illum illo repellat. Vel aspernatur ad quis distinctio labore ipsum quia. Rem voluptatem molestiae ad.

Sequi commodi dolorum quo officia voluptas est. Perspiciatis dolor pariatur debitis fugiat. Porro iure reprehenderit ut modi vel quos. Optio et alias sed optio et iste incidunt. Itaque vero in quo corporis illo eum. Excepturi qui distinctio velit odio totam.

Libero quaerat dolores earum. Eaque sit incidunt ipsa corrupti nesciunt ducimus a. Non id dolorem laudantium excepturi dolor et sunt. Rerum nostrum delectus repellat reprehenderit praesentium ut. Sunt nihil dolor voluptas.

Nemo inventore saepe consectetur ut et recusandae saepe. Molestiae earum itaque consequuntur adipisci iure animi est deserunt. Eum nemo esse accusantium. Esse facere est perspiciatis a reiciendis assumenda. Non neque et explicabo non veniam alias provident.

Necessitatibus pariatur iusto ducimus at quam repudiandae qui. Corrupti unde odit quia harum dolore veniam deleniti.