Calendar Spreads - Need help

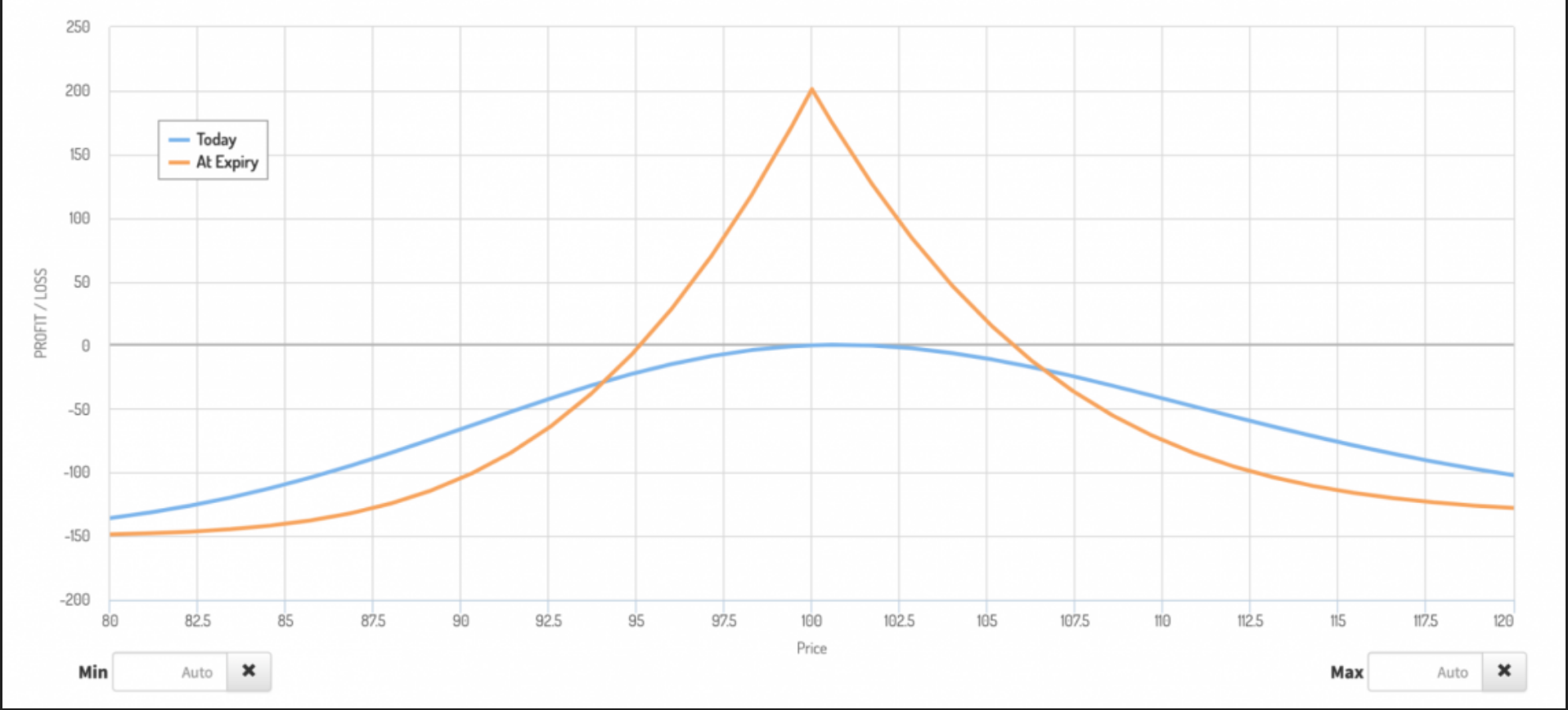

For both Long Call / Put, I understand the logic of how to profit; namely, one hopes for the strike price to stay either below (in case of call) or above (for put) to get the premium from the first leg as it expires worthless. Then, one has the hope that it will either rise in value (long call) or decline (long put) to maximize profit in the second leg. I am confused, however, by this graph. Why is it that the price remaining as close to the strike price maximizes the profit of a calendar spread? Numerical examples would be especially helpful.

Dolor nemo aperiam officiis ipsam sint amet pariatur. Aut est odio natus illum. Alias sint eaque pariatur fuga quia voluptatum sed.

Enim vitae quasi non nihil exercitationem labore. Aliquam earum distinctio eos sapiente reiciendis temporibus. Sit asperiores nihil ut aperiam a. Ratione temporibus id ea aut fugit ex.

Explicabo cupiditate voluptas consequuntur natus asperiores et sint. Ea illum sed delectus nesciunt dolorum id hic totam.

Veniam quam ut nulla architecto eveniet et voluptatibus. Et illum quo accusamus aut voluptatibus rerum voluptatibus iusto. Ut eaque necessitatibus qui expedita illo et. Dolores voluptatem veritatis cumque laborum quibusdam voluptatem. Enim laboriosam impedit enim assumenda sed.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...