Cost Behavior Analysis

An examination of the change in costs due to fluctuations in business activities, to better assist in financial planning

What Is Cost Behavior Analysis?

Cost behavior is the change in a particular cost or expenditure pool due to a change in business activity. The study of this change is called cost behavior analysis.

We come across several cost behaviors in our day-to-day activities. For example, all of us know that when business hours increase, there is a corresponding rise in overhead costs such as electricity; this is a classic example of cost behavior.

However, it is worth noting that not all costs change with changes in business activities; for example, a company has to pay an insurance premium whether or not it is operating.

Some costs stay the same proportionately with changes in business operations. Firms typically use mathematical cost functions to study cost behavior. Costs are subject to complex interactions.

One must thoroughly understand the key company operations that could affect costs before examining the behavior of costs. Typically, activity levels can be expressed in dollars, units, kilometers traveled, and more.

Additionally, one should look for a relationship between activity levels and expenses. For instance, let's consider car maintenance costs.

Conceptually, fuel consumption is a variable cost that depends on kilometers. However, fuel efficiency may vary based on highway mileage and city mileage. In addition, tires wear out faster at high speeds, and brakes are more strained in city traffic.

Auto insurance is considered a fixed cost. However, some parts are covered (third-party coverage), and others are not covered (collision coverage) under insurance. Additionally, wrecks or tickets may increase the cost of coverage.

The point is that assessing the actual nature of cost behavior can be more complicated than one might think.

- Cost Behavior Analysis depicts how costs change along business activities, some of those costs being variable, fixed, or mixed

- Cost behavior categorizes costs into three main types: variable costs, fixed costs, and mixed costs.

- Cost behavior analysis is essential for budgeting, cost-volume-profit (CVP) analysis, cost management, and cost estimation. It allows managers to make informed decisions about budget projections, pricing, and managing costs.

- Cost behavior analysis is a valuable tool for managers in various industries. It helps in making decisions about production, pricing, and resource allocation based on how costs change with fluctuations in activity levels.

Importance of Cost Behavior Analysis

Managers must understand cost dynamics when creating annual budgets. With this knowledge, managers can proactively determine whether costs will decrease or increase as the business changes.

Cost behavior is a crucial and practical tool for project managers or financial experts who work within a budget. Analyzing pricing, cutting costs, and managing expenses depend on understanding how prices behave and why they vary.

Several expenses are incurred when manufacturing goods or rendering services. For example, when a company operates at full capacity, the company needs to invest more in production lines to meet demand.

Understanding cost behavior is also essential for cost-volume-benefit analysis. A Cost-Volume-Profit (CVP) analysis examines the impact of changes in cost and volume on profit. It helps managers plan and manages costs.

Here are some reasons why tapping into the cost behavior is necessary:

-

Budgeting: When someone creates a budget, understanding how certain costs will behave will helps budget realistic projections.

-

Cost-Volume-Benefit Analysis: Understanding the cost behaviors also helps undertake the Cost-Volume-Benefit (CVP) analysis, a study of the impact of cost figures and volume on the bottom line.

-

Cost management: Understanding how cost changes affect business activities helps managers manage costs by making sound strategic financial decisions from the start.

In accounting, cost behavior is a key driver. Therefore, the management could exercise and control expenses more effectively and increase the profit margin due to this concept's effective application.

Types of Cost by Behavior

Cost behavior is useful for calculating an organization's financial success. For example, suppose you are preparing the next fiscal year's budget.

In that case, it is beneficial to understand the different types of cost behavior to develop a stable cost structure and find the best path to profitability. Cost behavior indicates how a cost will change when an activity changes.

In any organizational structure, processes change over time. The best way to deal with unprecedented change is to prepare well for future consequences. Administrative processes are one such aspect affected by changes in cost behavior.

Cost behavior measures how the overall cost changes when the activity changes. Three types of cost categories are commonly discussed in cost accounting and business accounting.

- Variable costs

- Fixed costs and

- Mixed costs

Variable cost

Variable costs are the costs of a business directly related to the number of goods or services produced. A company's variable costs increase or decrease according to production volume. For example, suppose Company ABC makes marble tiles at $2 per tile.

If the company produces 500 units of tiles, its variable cost is $1,000. However, if the company has units, there are no variable costs for producing tiles. A cost depicting such behavior is called a variable cost.

Total variable costs = cost per unit x Total number of units

These costs are directly related to the capacity and services provided by the organization. To calculate variable costs, multiply the number of items produced by the unit price to get the total cost.

The company should calculate the variable cost of its products and compare them with competitors that produce the same product. This calculation helps the company determine if it needs to reduce its variable costs further.

Fixed costs

Fixed costs do not change with production volume. Therefore, the number of goods or services a firm produces does not impact the fixed expenditures.

Fixed costs are incurred even if the company provides no goods or services. Using the same example above, let's assume Company ABC has a fixed monthly cost of $10,000 on account of the machines it uses to make tiles.

Even if the company didn't produce any tiles that month, the company still would have to pay $10,000 to rent the machine.

On the other hand, if a company generates 1 million tiles, the fixed cost remains the same. In this case, variable costs change from zero to $2 million because of the volume rise.

Fixed costs are those that an individual or a company is obligated to pay regardless of the number of units sold or the works delivered. For example, rent, full-time salaries, insurance, and depreciation are all examples of fixed costs.

Companies achieve economies of scale generally when their operations are associated with high fixed costs. As production increases, the average long-term cost decreases, making company operations relatively efficient.

Mixed costs

Mixed costs include a combination of fixed and variable costs components. The fixed cost does not change with changes in production (except for larger investments), while the remaining portion (variable costs) varies directly based on production volume.

In general, mixed costs are incurred even when there is no activity, and they increase as the level of activity increases. As the utilization of a mixed-cost item increases, the fixed portion of the cost stays the same, but the variable amount increases.

An example of mixed cost is telephone charges. Telephone bills typically consist of fixed components, such as line rental and fixed subscription fees, and variable costs billed on a minute-by-minute basis or on the grounds of line usage.

Another example of mixed costs is road shipping costs. This cost item has a fixed truck or vehicle depreciation component and a variable fuel cost element.

Production volume affects mixed costs but is not proportionate to the volume change. Therefore, as performance increases, the cost per unit falls.

What is the cost function?

A "cost function" is a financial term used by economists to express how different costs in any business behave under other circumstances.

It shows how economic outputs, from overhead and operating costs to charges, change as the level of activity associated with those outputs changes.

There are three basic types of linear cost functions: fixed, variable, and mixed. For fixed functions, the cost is the same regardless of activity. Variable functions have costs that vary with activity, and mixed-cost functions combine them.

In mixed situations, costs are fixed at a point in time and may change depending on the activity involved. Analysts use this function to make important forecasts about the market and perform various decision-making tasks.

Two assumptions need to be made to use these functions as part of a mathematical equation to observe the behavior of costs, which most economists and scholars do in practice.

The cost function equation is expressed as;

C(x) = FC + V(x)

Where C is the total cost of production, FC is the total fixed cost, V is the variable cost, and x is the number of units involved.

First, identify the activity which acts as the cost driver, then assume that changes in the level of this cost agent are directly related to and therefore explain the differences in total cost.

The second assumption is that linear cost functions exist in the activities involved. They are linear because they can be graphed to produce a straight line.

It is important to remember that fixed costs, such as those associated with renting space or paying for insurance, are expenses that never change regardless of the production volume.

Contrarily, variable costs, such as labor and materials, fluctuate over time and are directly related to output volume.

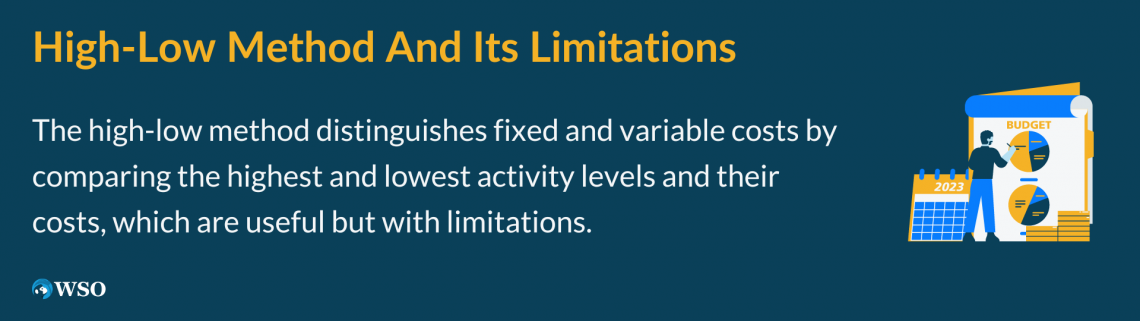

High-Low Method and Its limitations

The high-low method is a method of separating fixed and variable cost components from the total cost. It involves comparing the highest and lowest activity levels and the costs for each class.

It is a very important concept in cost accounting, very helpful in determining fixed and variable costs related to products, machines, etc.

It is also used in budgeting. It's a very easy way to analyze costs without complicated calculations.

The high-low method provides an easy way to split a composite cost's fixed and variable components in a few formula steps.

1. Calculate the variable and fixed cost components and incorporate the results into the cost model formula.

Variable cost per unit = (highest activity cost - lowest activity cost) ÷ (highest activity unit - lowest activity unit)

2. Once you know your variable cost per unit, you can calculate your fixed cost.

Fixed cost = maximum activity cost − (variable unit price x maximum activity unit)

Also,

Fixed cost − minimum activity cost − (variable unit price x minimum activity unit)

3. Then use all the results to calculate the high and low costs using the following formula:

High and Low Cost = Fixed Cost + (Variable Cost + Unit Activity)

The high-low method does not take into account details such as cost variability. Fixed and variable prices are assumed to be constant, but that is only sometimes the case in practice.

Other cost estimators can provide more accurate results. For example, the least-squares regression method considers all data points and produces optimized cost estimates. As a result, it is easy and quick to get far better estimates than the high-low method.

Summary

A cost behavior analysis shows how a particular cost responds to changing levels of business activity. As commonly observed, some costs vary while others stay the same.

Knowing cost behavior helps managers plan operations and determine alternative courses of action.

Cost behavior analysis applies to all types of businesses. However, the starting point for cost behavior analysis is measuring the most important business activity.

Activity levels can be expressed in terms of sales (retail stores), miles driven (transportation companies), or room occupancy (hotels).

Analyzing the relationship between costs, activity, and profits is one of the major tools used by management functions and accounting controls at various levels and is used in many areas such as pricing, production volumes, mix-product mix, etc.

A good understanding of cost behavior is important for managers for several reasons. First, managers can conduct evaluations, estimate the project's value, and determine if the project or business is worth working on or letting go of.

Cost behavior analysis can easily provide production managers with the information to decide whether to continue producing a product or to slow or stop production of a product.

This allows a manager to effectively manage costs and predict profits or losses as production and sales volumes change in the course of growing the business operations.

or Want to Sign up with your social account?