Window Dressing

An accounting technique companies will use to manipulate their financial health into appearing more healthy.

What Is Window Dressing?

Window Dressing refers is the manipulation or adjustment of financial data to make the company’s financial health appear more favorable than it is. There are numerous techniques that businesses or individuals will use to increase the attractiveness of their financial standing.

The term "window dressing" originates from making something appear more attractive by adding superficial improvements, like arranging items in a shop window display.

Accounting can often be called creative, innovative, or aggressive. Accounting is defined as communicating and reporting financial data. Therefore, these adjectives describe window dressing, which paints a picture of what is happening behind the scenes.

Creative accounting commonly occurs during reporting periods, such as quarterly or annual financial statements, when companies must disclose their financial condition to the public. They will employ these aggressive accounting techniques to enhance the company's reputation.

This accounting technique distorts the proper financial position of a company and can deceive investors and stakeholders.

This distortion has caused regulatory bodies, such as the Securities and Exchange Commission (SEC), to implement rules and regulations for detecting and preventing these practices.

Innovative accounting is more common with larger companies with significant shareholders because they want to impress their investors. Hence, they continue to put their money into their business.

Companies will also employ this technique to trick lenders into qualifying for loans and other credit options.

- Window dressing refers to the practice of making a company's financial statements or performance appear more attractive than they actually are.

- This involves using accounting tricks or strategic timing of transactions to improve the appearance of financial health, often to mislead investors, analysts, and other stakeholders.

- Companies may engage in window dressing to attract new investors or to retain current ones by presenting a more favorable financial position.

- Enhancing the appearance of financial statements can lead to higher stock prices, benefiting the company's market value and shareholders.

Understanding Window Dressing

Companies use it for several reasons, driven by their desire to present a more favorable image of their financial performance.

Even though it is generally considered unethical, it's essential to understand the motivations behind this practice to spot its occurrence.

Here are some explanations of why companies resort to window dressing:

Attracting Investors And Pleasing The Public

The way that companies attract new investors or retain existing ones is by presenting a positive financial picture. When numbers fall, fearful businesses will paint a perfect financial picture to appease investors in their funding decisions.

They will use this method to satisfy these stakeholders' expectations and maintain positive relationships. These distorted financial statements can instill confidence and stability in stakeholders, investors, and employees.

Maintaining Stock Price

Publicly traded companies will use window dressing to maintain or increase their stock prices.

Note

Higher stock prices benefit the existing shareholders and the company's ability to raise capital through stock offerings or debt issuances.

Meeting Analyst Expectations

Institutions face a lot of pressure to meet or exceed analyst expectations regarding financial performance. By manipulating their financial statements, they can create the illusion of surpassing targets, which can help avoid adverse market reactions.

Securing Financing

Businesses will use creative accounting to obtain more favorable financing terms from lenders or creditors. If they present a healthier financial position, the companies can negotiate lower interest rates, increased credit limits, or better loan terms.

Preserving Credit Ratings

It can maintain or improve a company's credit ratings. Higher credit ratings allow companies to access capital markets at lower borrowing costs, secure better credit terms, and demonstrate financial stability to investors and stakeholders.

Executives' Incentives And Compensation

Executives often have performance-based compensation linked to financial metrics like earnings per share (EPS) or revenue growth. Corrupt leaders will manipulate economic data to achieve their targets and gain monetary rewards or bonuses.

Competitive Advantage

By presenting more robust financial performance, companies can attract customers, suppliers, and business partners, creating a perception of stability over their competition.

Despite these potential motivations, It can damage a company's reputation and undermine investor trust. These inaccurate assessments of a company's financial health can cause the misallocation of capital and increased systemic risk within the financial system.

Regulators must scrutinize financial statements and hold companies accountable for their reporting practices.

NOTE

Employing any manipulation in accounting is unethical and will have severe consequences for the business’s reputation and operations.

How Do Companies Window Dress

Now that we have examined why a company would participate in innovative accounting, let’s look at how they do that.

Here are a couple of ways companies window dress:

- Timing of transactions: Companies will conduct strategic time transactions to manipulate financial statements. They sometimes recognize expenses, like maintenance or repairs, after the reporting period to artificially inflate profits.

- Vice versa, they might recognize revenues before they should, such as counting sales before they are finalized.

- Manipulating reserves: If adjusted, reserves and provisions, such as those for bad debts or legal liabilities, will impact financial statements. Reducing these reserves will increase their reported earnings and financial ratios, making their financial position appear strong.

- Off-balance sheet transactions: The most common way organizations falsify financial statements is by making off-balance sheet transactions to prevent certain assets or liabilities from being recorded. For example, they might enter into operating leases instead of capital leases to avoid having to recognize the support.

- Creative revenue recognition: Employing aggressive revenue recognition techniques can boost reported revenues. For instance, recognizing revenue, they might record sales before the products are delivered or services are performed.

- Strategic debt management: Manipulation of debt levels and debt ratios can help you appear more financially stable. They might temporarily borrow near the reporting date to reduce reported debt levels.

- Selective disclosure of financial ratios: Businesses will highlight only the financial ratios that present them in a positive light while failing to disclose those that reflect poorly on their financial condition. For example, they might emphasize profitability ratios while neglecting any liquidity ratios that reveal potential risks.

- Investors and analysts should exercise caution and thoroughly analyze financial statements.

NOTE

Examining multiple periods of financial data, reviewing footnotes and disclosures, and considering other sources of information is the best way to assess the proper financial health of a company.

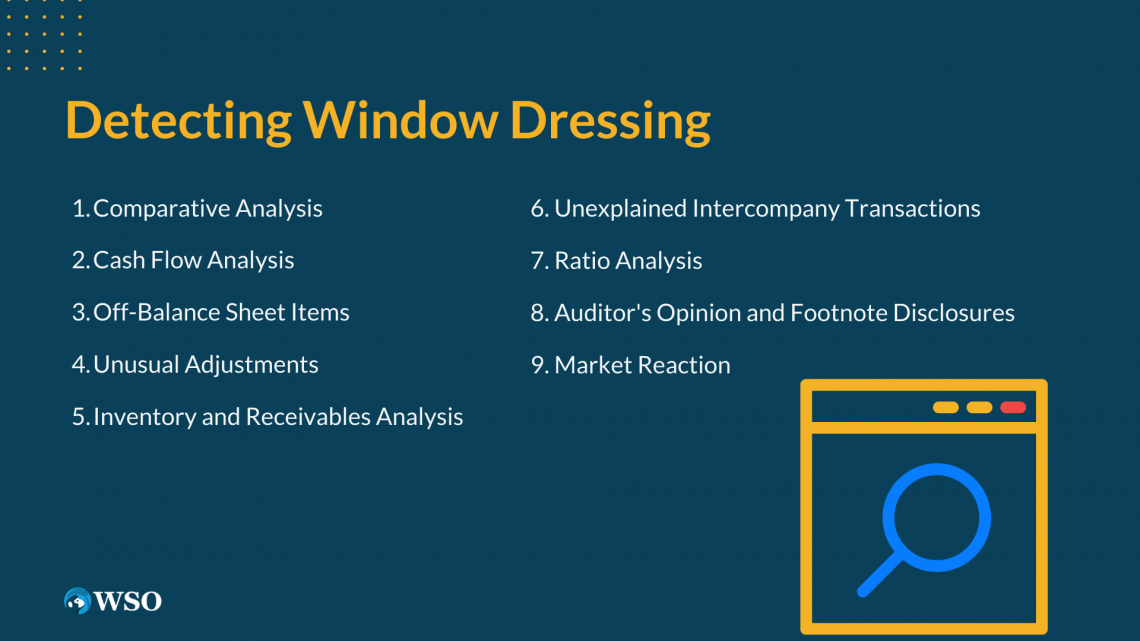

Detecting Window Dressing

Detecting window dressing requires careful analysis and scrutiny of financial statements. Individuals can find a company’s financial statements on the SEC’s platform EDGAR. To see this information, look for Form S-1, Form 10 Q, or Form 10 K.

While it can be challenging to identify creative accounting, here are some strategies and indicators that can help in the detection process:

- Comparative Analysis: Perform a comparative analysis of financial statements over multiple reporting periods. Look for significant fluctuations or abnormal patterns in key financial metrics. Sudden and unusual changes indicate potential window dressing.

- Cash Flow Analysis: Analyze the operating cash flow and compare it with the reported net income. Discrepancies between cash flow and reported profits may indicate aggressive revenue recognition.

- Off-Balance Sheet Items: Scrutinize the footnotes and disclosures to identify off-balance sheet transactions or potential liabilities that may have been omitted from the balance sheet. Pay close attention to lease arrangements or contingent liabilities that could be used to hide debt or assets.

- Unusual Adjustments: Significant and unexplained changes in accounting methods could indicate manipulation to improve reported financial results.

- Inventory and Receivables Analysis: Evaluate inventory turnover ratios to identify potential manipulation. Unusually high inventory levels indicate overstated sales or delayed recognition of expenses.

- Unexplained Intercompany Transactions: Related-party transactions are one of the most common ways companies manipulate their data. Organizations will use artificial transactions between any related entities to inflate revenues or understate liabilities.

- Ratio Analysis: Conduct a comprehensive analysis of financial ratios. Compare trends to industry peers or historical data to see if anything is abnormal. Pay attention to liquidity ratios, leverage ratios, and profitability metrics, as they have the highest likelihood of revealing potential anomalies.

- Auditor's Opinion and Footnote Disclosures: Since the auditor is a professional, one must carefully read the auditor's opinion and footnotes. Look for any qualifications, uncertainties, or concerns raised by the auditors.

- Market Reaction: The market reaction, whether positive or negative, will usually reflect on the business’s financial statements. Monitor the market reaction to company announcements, earnings releases, or significant events. Evaluate whether reported financial results align with market expectations.

- Investors should seek professional advice or conduct thorough due diligence to make informed investment decisions.

NOTE

Although these strategies can help detect aggressive accounting, conclusive evidence may require a more profound examination by a forensic account or expert analysis.

Window Dressing and Mutual Funds

Creative accounting can still occur in investment funds. Portfolio managers engage in aggressive accounting by selectively disclosing only their best-performing investments while hiding the poor performers.

They do this because they know that by showcasing a portfolio with solid returns, they will increase the fund's overall appeal.

Portfolio managers rebalance the fund's portfolio near the end of a reporting period. This could be done by selling underperforming or unpopular securities and replacing them with better-performing assets. This creates the impression of a high-quality portfolio and boosts reported returns.

Corrupt managers might temporarily reduce the cash holdings and invest the funds in securities to generate higher reported returns. This will create the appearance of an actively managed fund and attract investors seeking higher returns.

Another way to make the fund appear more attractive is to deliberately increase the concentration of the fund's portfolio in a few top-performing stocks near the reporting period. This will inflate the fund's returns and create the impression of outperformance.

NOTE

Window dressing, even in mutual funds, is considered unethical. While it aims to attract investors and improve reported returns, it must be more accurate and distort the fund's actual performance and risk profile.

It puts investors, the public, and stakeholders at risk and should not be practiced. Regulatory authorities closely monitor mutual funds to ensure they follow the regulations. These regulations are set to enhance transparency and protect investors' interests.

Window Dressing FAQs

No, it is generally considered unethical in the field of finance. It is a manipulative practice to present a misleading or distorted picture of a company's or mutual fund's financial performance or position.

The legality of this accounting practice varies on the specific actions taken and the jurisdiction in which they occur. While window dressing may not be explicitly illegal, certain aspects violate securities laws, accounting regulations, and other regulatory requirements.

Creative accounting aims to enhance a company's financial position to the public to gain funding or market popularity.

Some people consider this type of accounting an art when not used as a manipulation tactic. This is because it sometimes involves adjusting numbers to motivate a business to what needs to be changed to yield better results.

It is typically tough to detect and requires an expert analyst or a forensic accountant.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?