Expected Default Frequency (EDF)

A probability measurement that a company will default on the amount lent to them within a specific time frame of one year.

What is Expected Default Frequency (EDF)?

Expected default frequency (EDF) is a probability measurement that a company will default on the amount lent to them within a specific time frame of one year.

Credit is established when one party lends a resource to another based on a deal or contract. Credit is always given based on a contracted date in the future, after which the payment has to be made. The resource may be money, like banks, or in some physical form, like inventory.

Credits involving physical resources like inventories are called trade credits, while one involving money is called debt. However, both forms of credit involve risk.

This risk is attributed to the lender's issuing resources in advance to the borrower without any immediate payment. Consequently, the credit-issuing party may experience financial losses if the borrower cannot repay the credit.

Therefore, any organization that extends credit must examine the borrower and his credit history before doing so. This evaluation process, which considers specific criteria to determine the risk associated with extending credit, is commonly known as credit analysis.

In financial terms, if a borrower cannot fulfill the obligations of a credit offered to him, the borrower is said to have defaulted. Expected Default frequency, abbreviated as EDF, is a method of credit analysis developed by Moody’s Analytics as a part of the KMV model.

The KMV model was the work of three well-known researchers Stephen Kealhofer, John McQuown, and Oldrich Vasicek.

The Expected Default frequency theory suggests that a company defaults when the total liabilities payable by the company exceed the market value of its assets. This model measures credit for a five-year time horizon.

EDF computes the probability of a company or borrower defaulting on its payments within a given period by failing to meet its credit repayment obligations.

Key Takeaways

- Credit is established when one party lends a resource to another based on some deal or contract.

- If a borrower cannot fulfill the obligations of a credit offered to him, the borrower is said to have defaulted. Expected Default frequency (EDF) is a method of credit analysis developed by Moody’s Analytics as a part of the KMV model.

- EDF computes the probability of a company/borrower defaulting on its payments within a given period by failing to meet the credit repayment obligations.

- The EDF theory suggests that a company defaults when the total liabilities payable by the company exceed the market value of its assets.

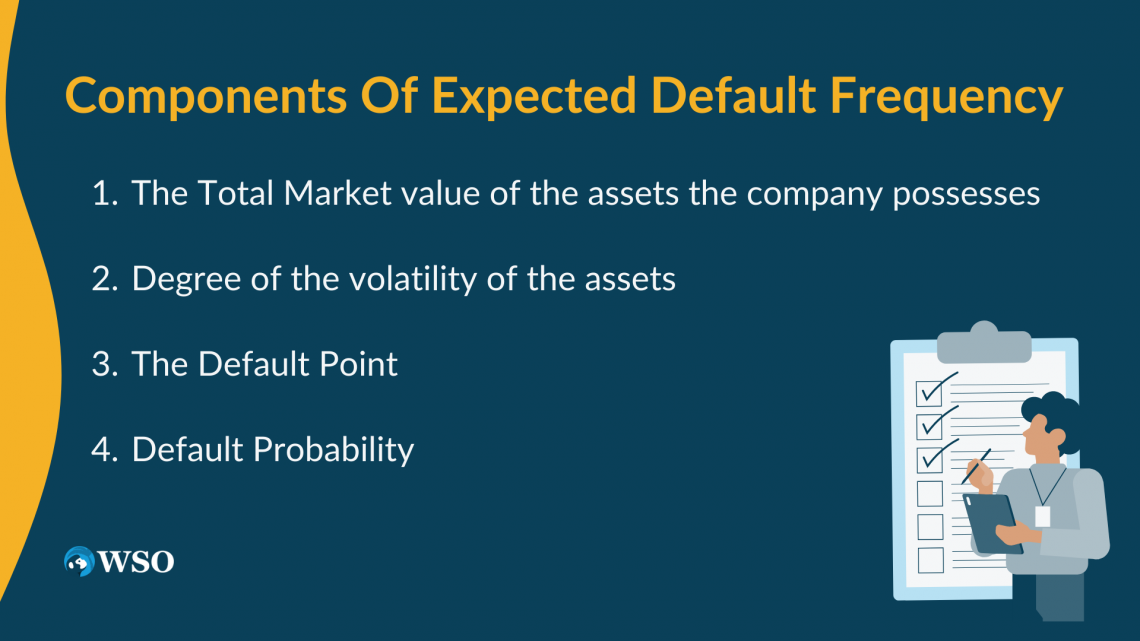

Components of Expected Default Frequency

There are four considerations while determining a company's Expected Default Frequency value. They are as follows:

The Total Market Value of the Assets the Company Possesses

The EDF calculation requires determining the total market value of the assets possessed by a company. Since this value cannot be directly observed, Moody's Analytics developed an option-theoretic model to evaluate it.

The option-theoretic model uses two things to compute the market value of the assets:

- The market properties of a company's equity value

- The book value of the company's liabilities

This model considers the equity value of a company as the representative of its underlying assets.

NOTE

If the book value of the liabilities payable by the company exceeds the market value of its assets, the company is said to have defaulted.

Degree of the Volatility of the Assets

Asset volatility refers to the scattering of the returns of a particular asset or assets a company owns. Generally, increased volatility of the assets is viewed as an increase in the risk of investing in the company’s assets or offering credit to the company.

NOTE

The prices of volatile assets are less predictable, hence considered high risk.

The standard deviation of the returns from the assets is a measure of asset volatility. If the assets show greater volatility, there is a greater risk of defaulting on the credit payment, so the investors are less optimistic about investing in a company with volatile assets.

The Default Point

The default point represents the level of the market value of assets below which a company cannot make scheduled debt payments. The default point varies for different companies and depends on two factors:

- The total valuation of the company’s assets

- The liability and debt structure of the company

Default Probability

The default probability is the likelihood that a company cannot fulfill its scheduled repayments within a specific period. It helps estimate the probability of a borrower being unable to meet its debt/credit obligations, i.e., the interest and principal payments within a given time frame.

The default probability depends on several factors:

- the borrower’s characteristics

- the debt history of the borrower

- The economic environment surrounding credit transactions

For example, in case of high inflation, the value of money is reduced. So the borrower’s ability to make repayments is strained due to the loss in the currency value.

NOTE

There are different methods of evaluating the default probability for businesses and individuals. For individuals, the default probability can be estimated by their FICO scores, whereas, for businesses, the default probability is estimated by their credit rating, computed by several credit rating agencies and credit analysts.

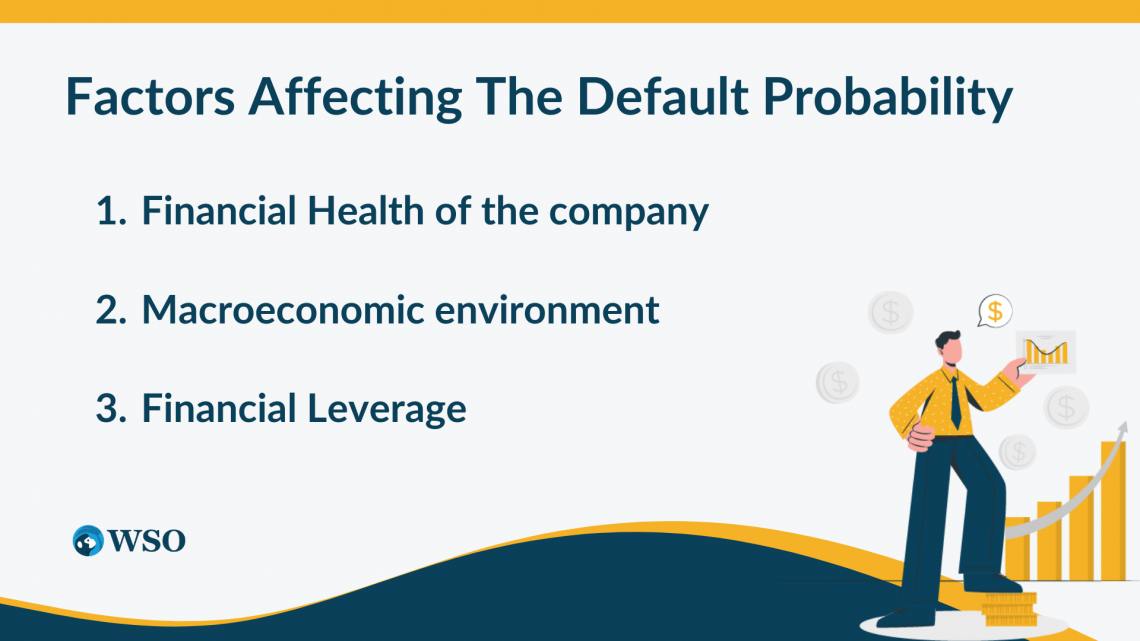

Factors that Determine the Default Probability of a Company

The key factors affecting the default probability of a company are as follows.

Financial Health of the Company

A debt-issuing organization decides whether to extend a loan to an individual or a company by analyzing and assessing its financial conditions.

The liquidity ratios of a company indicate its potential to repay its short-term obligations. It indicates whether an entity can repay its liabilities using its current assets.

The profitability ratio is another important factor in determining a company's financial health.

It provides information about a company's profit and the returns it gets from its assets. Any debt-issuing organization considers these important factors before lending money to a company. They only lend money to companies they feel can repay the debt.

Macroeconomic Environment

Moody’s KMV credit model calculates the Expected Default Frequency(EDF) as a function of distance to default. The distance to default is the difference between the total asset value of a company at the time of analysis and the default point.

NOTE

According to Moody's KMV model, a company becomes bankrupt when its assets' total market value becomes less than its debts.

The default distance is normalized with respect to the standard deviation of the future asset returns. This helps to compare the default frequencies of different companies without considering their size and minimize the risk involved.

Distance To Default (DD) = (MV - D) / σ

Here:

- MV = The total market value of the company’s assets

- D = The total debt of the company

- σ = The volatility(standard deviation) of the market value of the assets

The difference between MV and D gives the market value of the company’s equity, which is a function of the present value of all the future cash flows the company will generate.

NOTE

The general macroeconomic sentiment in society plays an important role in creating cash flows in a company.

If there is an economic slowdown and the probability of a recession is high in the market, there will be fewer cash flows, which will reduce the market value of the company’s equity, resulting in a shorter distance to default.

Hence the macroeconomic environment also plays a role in determining the expected default frequency.

Financial Leverage

When businesses use borrowed funds to invest in their products or operational activities, it is called leverage.

Leverage helps investors increase their purchasing power in the market, enhancing the returns obtained from investments.

NOTE

Some companies prefer to use debt to finance their activities rather than issuing new shares to the shareholders.

A company's leverage is evaluated by comparing the market value of its assets with the book value of the liabilities it has to pay. If a company's asset value decreases while the book value of its liabilities rises, the risk of default rises.

When the book value of liabilities exceeds the total market value of assets, implying that the value of assets possessed/owned by the company is insufficient to meet future debt obligations.

Expected Default Frequency Formula

We have seen the components of the EDF in the earlier section.

They are:

- The default point of the company (in $)

- The total market value of the assets possessed by the company (in $)

- The asset volatility (in %)

We can calculate the EDF if we know these three quantities. The formula used to calculate the EDF is as follows:

EDF = (Default Point / Market Value of Assets) * (Asset Volatility)

The above formula returns the expected default frequency as a percentage. Let's calculate the EDF using an example.

Suppose an aviation company's default point is $4,000, and the total market value of all its assets is $10,000.

This company's asset volatility percentage is 35%. The above formula gives the expected default frequency as 14%. Hence, there is a 14% likelihood that the company will default on its debt.

For example, as seen above, the aviation company's default probability is 14%, which is significantly less. So, the debt-issuing organization can consider issuing debt to the company.

The interest rate at which credit is granted also depends on the default probability. Debt-issuing organizations tend to give debt at a lower interest rate to companies with lower default probabilities because there is less risk.

On the other hand, companies with higher EDFs have to pay large amounts of interest even if they get a loan.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?