Modified Internal Rate of Return (MIRR)

A monetary indicator of an investment's appeal

What Is Modified Internal Rate of Return (MIRR)?

The modified internal rate of return (MIRR) is a monetary indicator of an investment's appeal. Ranking equivalent alternative investments are made in capital budgeting. As the name suggests, the internal rate of return (IRR) is modified, and as such, MIRR seeks to address several issues with the IRR.

The original version of the Modified Internal Rate of Return is occasionally implemented incorrectly on the erroneous presumption that interim positive cash flows are reinvested in another project at the same rate of return as the project that produced them.

It is typically a fanciful scenario, and it is more probable that the money will be reinvested at a rate closer to the company's cost of capital. As a result, the IRR frequently presents an overly optimistic image of the initiatives under consideration.

Also, a larger project with a lower modified internal rate of return could have a greater net present value. Hence the adjusted internal rate of return, like the internal rate, is not appropriate for comparing projects of various sizes. However, certain modified internal rate of return alternatives may be applied to these comparisons.

That is why we first have to understand the net present value and the internal rate of return to understand the modified internal rate of return better.

- Modified Internal Rate of Return (MIRR) improves on internal rate of return (IRR) and evaluates investment attractiveness in capital budgeting.

- Net present value (NPV) compares project costs to future cash flows for investment decisions.

- IRR assesses investment profitability based on a discount rate.

- MIRR addresses IRR's issues of multiple rates and conflicting investments.

- MIRR compares similar-sized investments, considers returns and reinvestment rates, but calculation methods may vary.

Net Present Value

The net present value (NPV) of an investment is the difference between the initial investment of the project and its future expected cash flows. It is one of the capital budgeting techniques used to assess if the project will be worth more or less than its value in the future and, therefore, whether to invest or not.

The net present value formula is

NPV= - Costs + PVECF

Where,

- NPV: net present value

- Costs: are the initial costs and/or today’s value of the invested cash

- PVECF: present value of all expected future cash flows,

For example, suppose a company’s cash revenue from its coconut oil business is $28,000 yearly. However, the costs are around $19,000 yearly, including taxes, and the initial investment required for this business is $22,000. Therefore, the required rate of return on such investment is 13%, and the project operates for eight years.

Profit = expected cash flow = Revenues - costs = 28,000-19,000 = $ 9,000

An important consideration of the NPV is that it considers the time value of money, meaning the premise is that the $1 earned today is not worth the same as the $1 earned tomorrow. Assuming that the money can be put used to generate returns. Making $1 earned today is worth more than $1 tomorrow.

Here the PVECF is an annuity because we have the same expected cash flow for the entire investment period.

PVECF = 9,000[1 − (1/(1.13^8)]/.13 = 43,188.93

NPV= - initial investment value of cash + PVECF = -22,000 + 43,188.93 = 21,188.93

If the NPV is positive, then we can take the investment.

Now, based on the previous example, let’s say that the project generates profits of 6,000, 8,500, and 14,000, respectively, and the project operates for three years with the exact cost of investment and required return, then the NPV becomes:

NPV= -22,000 + 6,000/1.13 + 8,500/(1.13)^2 + 14,000/(1.13)^3= -$330.82

The NPV is negative; we don’t make the investment in this case.

Internal Rate of Return

Why did we go through the net present value? First, to determine the internal rate of return IRR, we need the NPV.

The Internal Rate of Return is the discount rate that makes the NPV of an investment equal to zero in a DCF Analysis. It is a financial research indicator used to determine the profitability of possible investments.

- Generally, the greater the internal rate of return, the more favorable an investment is. However, IRR is consistent across investment kinds and may thus be used to rank different prospective investments or projects on a pretty level basis.

- When comparing investment choices with similar features, the investment with the highest IRR is likely to be the best.

- The IRR rule states that if the IRR of an investment exceeds the required return, then the investment is acceptable.

For instance, consider an investment that costs $200 and returns $225 in one year. Then the IRR will be

NPV= 0 = - 200 + 225/[1+ IRR]

⇒ IRR= 12.5%

If the required return is less than 12.5%, the project will be rejected

If the necessary return is more than 12.5%, the project will be accepted

Problems With IRR

Although IRR is very popular in practice, it has several flaws:

A. Multiple IRRs

A Non-Conventional cash flow: A succession of negative and positive cash flows over time with several changes in the cash flow direction is known as an unconventional cash flow. In contrast, a regular cash flow experiences one shift in the direction of the flow.

Back to the problem, when we have such a situation, there is a possibility of having more than one discount rate that makes the NPV zero and, therefore, more than one IRR.

It will lead to confusion about what IRR or whether to take the investment or not and might sometimes cause inefficiencies for the chosen IRR.

B. Mutually Exclusive Investments

A mutually exclusive investment decision is a situation where taking one investment prevents you from taking the other investments.

Given more than two investments having acceptable IRRs according to the IRR rule, which one should we choose? This situation also leads to confusion, inefficiency, and the risk of taking one investment leading to fewer revenues than the other investment.

Note that taking the investment with a higher IRR is risky and inaccurate.

C. Possibility of misinterpretations if used outside the assumptions and premise.

A project with higher capital investment may appear to have a lower IRR when compared to a project that has a lower capital investment.

A project with a lower IRR but with a slightly pumped-up capital investment can be profitable in the long term. But, if the management decides to with IRR, they will ignore this project.

A modified version is created to address the IRR problems and is called the modified internal rate of return.

Modified Internal Rate of Return (MIRR)

The modified internal rate of return was introduced to address the shortcomings of the IRR. It’s a financial metric to assess an investment’s attractiveness, typically used in capital budgeting to compare the investment opportunities in similar projects.

As the name suggests, the MIRR is modified, and the Modified Internal Rate of Return seeks to address several issues with the IRR. The MIRR, therefore, more accurately reflects the cost and profitability of a project.

We have three methods (approaches) and one formula to compute the MIRR. Before computing the Modified Internal Rate of Return, here is the example that we will use for all methods:

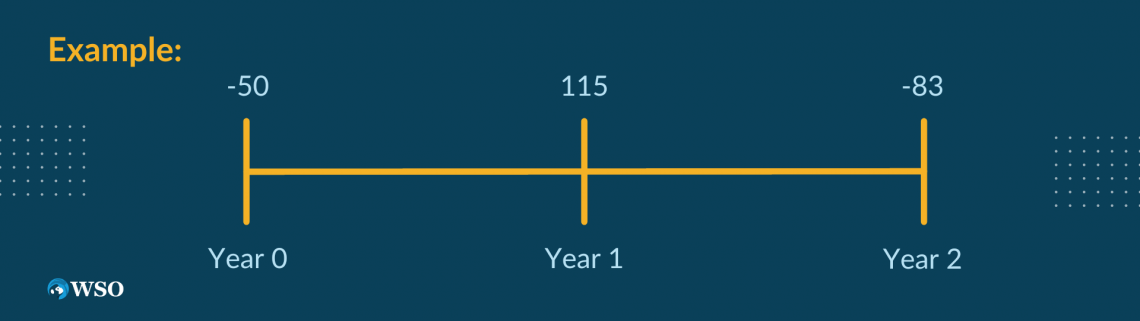

Suppose a company wants to invest in producing tissue paper for two years. The initial cost of the investment is 60 dollars, and the expected cash flows are $125 and -$83 for years one and 2, respectively. The required return on investment is 17.5%.

A. Method 1: The Discounting Approach

In this approach, all future negative cash flows are discounted back to the present (their present value) at the required discount rate, added to the initial cast then computed as the IRR.

Modified cash flows:

Time 0: -$50 + (-$83/1.175^2) = - $110.12

Time 1: $125

Time 2: $0

The MIRR is : NPV= 0 = - 110.12 + 125/(1+MIRR) ⇒ MIRR= 13.51%

In this method, we consider the initial investment of $50, and we discount all future negative cash flows to the present under time 0. In our case, only negative cash flow is at time 2, so we discount the $83 of time 2 to Time 0. At this point, we add all the cash flows using the IRR formula, leading us to get the MIRR.

B. Method 2: The Reinvestment Approach

In this approach, we compound all cash flows (positive and negative) except the first out to the end of the project's life and then calculate the IRR.

The modified cash flows become:

Time 0: -$50

Time 1: $0

Time 2: -$83 + ( $125 x 1.175) = $63.875

The MIRR is : NPV= 0 = -$50 + ( $63.875/[1+ MIRR]^2) ⇒ MIRR = 13.03%

In this method, we consider the initial investment of $50 at time 0, then compound all our cash flow to the period of the end of the project. In our case, the project ends at time 2, so we have to compound the cash flow of time 1 to time 2.

To compound, we multiply our cash flow at time one by the rate, and then we add the cash flow value to time 2. At this point, the initial cash flow remains intact because it is the period of the end of the project, so we only add the compounded cash flow at time 1, and then we use the IRR's formula to get the Modified internal rate of return.

C. Method 3: The Combination Approach

In this approach, the first two methods are combined in one. First, we discount all the negative cash flows to the present, and we compound all the positive cash flows to the end of the project period, then compute the IRR.

The modified cash flows:

Time 0: -$50 + (-$83/1.175^2) = - $110.12

Time 1: $0

Time 2: $125 x 1.175 = $146.875

The MIRR is: NPV= 0 = -$110.12 + ( $146.875/ [1+MIRR]^2) ⇒ MIRR = 15.49%, the highest of the three methods.

D. The Modified Internal Rate of Return Formula

The following formula represents it:

MIRR= (FV/PV)1/n - 1

Where,

- FV: is the future value of all positive cash flows at the cost capital of the company

- PV: is the present value of all negative cash flows at the financing cost of the company

- n: the number of years of the project

Assuming the cost of capital and the company's financing cost are equal to the required return, the Modified Internal Rate of Return formula illustrates the third method.

Applying the formula to the example above:

n= 2

FV= $125 x 1.175 = $146.875

PV= $50 + ( $83/1.175^2) = $110.12

MIRR= (146.875/110.12)½ -1 = 0.1549 = 15.49%

What Can MIRR Tell You?

IRR overstates returns on investment and deceives investors. On the other hand, MIRR evaluates various expenses to determine the returns one might anticipate from an investment, avoiding misleading investors, businesses, and business managers.

In addition, a Modified Internal Rate of Return can be helpful in a variety of other financial matters, including

- Compares similar-sized assets based on the prospects they offer.

- An investment or project is more appealing if the MIRR is higher than the projected return, and vice versa.

- Computes the difference between the reinvestment rate and the investment return by modifying the IRR of a project or investment.

- Eliminates the problems brought on by many IRRs at the same time.

- Allows for the projected growth rate of the reinvestments to be adjusted at various phases of project completion

- Provides the option to adjust the computations to account for any reinvestment rate.

Advantages and Disadvantages of MIRR

The Modified Internal Rate of Return may be a valuable tool in determining which initiatives are most worth pursuing when your small firm considers possible capital investments in various projects. However, it has some disadvantages too.

Advantages

- Modified and improved methods to assess projects.

- Doesn’t suffer from multiple rates of return.

- It takes into consideration all the possible reinvestment rates.

Disadvantages

- There are different ways of calculation, and there is no apparent reason to say one of the three methods is better than the other.

- It asks for two other decisions, such as determining the cost of capital and financing rate.

MIRR VS IRR

This section aims to elucidate the difference between two fundamental concepts in finance: the Modified Internal Rate of Return (MIRR) and the Internal Rate of Return (IRR).

Both these metrics are commonly used to evaluate potential investments, and understanding their differences is crucial in making informed investment decisions.

Let's understand these differences below:

| IRR | MIRR |

|---|---|

| Exaggerates the projected return on investment. | Provides a precise estimate of the returns. |

| Might lead to capital budgeting mistakes. | Overcomes problems with capital budgeting brought on by numerous IRRs. |

| Calculates accounts, cash flows, and the reinvestment rate. | Calculate the returns using the corresponding anticipated stage-by-stage current reinvestment rates that are relevant. |

| Assumes that cash flows will be reinvested at the same pace. | Assumes that positive cash flows will be reinvested at the cost of capital. |

| Discounting the investment's initial growth. | Thinks about financing the upfront costs at the finance cost. |

| Similar to how the growth rate's inverted compounding works. | Helps managers set reasonable expectations for returns and plan their goals accordingly. |

| Occasionally offers two options, which causes confusion or misunderstanding. | Always presents just one solution. |

| Assumes that the growth rate will be the same from one project to the next. | Assumes that a project's growth rate will change as it progresses. |

Researched and authored by Ely Karam | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?