Venture Capital

An industry where pooled money is invested into startups to try and generate high returns for investors.

What Is Venture Capital (VC)?

Venture Capital (also known as VC) is an industry where pooled money is invested into startups to try and generate high returns for investors.

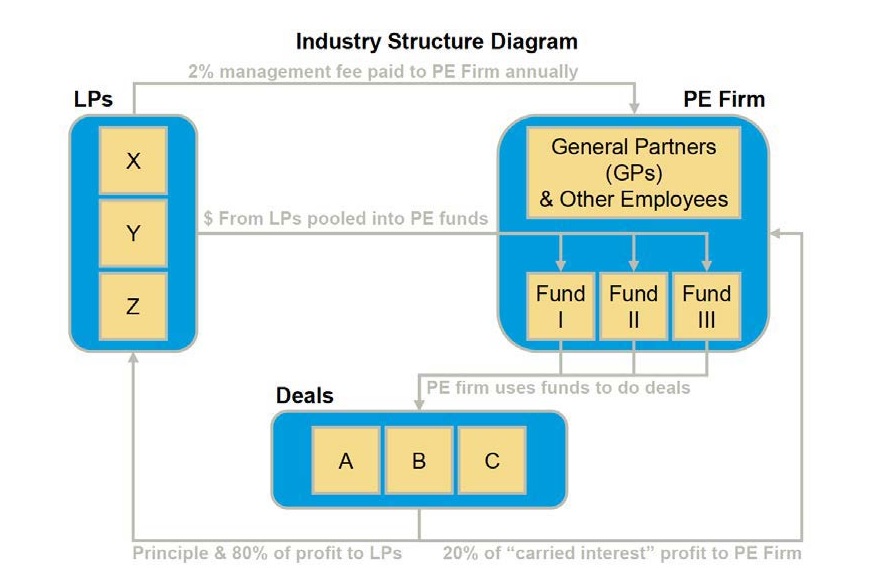

VC funds raise money from LPs (limited partners) and then invest those funds acting as the GP (general partner). For their work in finding, investing, growing, and exciting opportunities, they generally charge the LPs a fee of about 2% of assets under management (AUM) and 20% carry.

Another way to think about VC is as a type of private equity that is primarily focused on startups, early-stage and emerging companies that are believed to have long-term growth potential or that have demonstrated high growth.

VC funds not only provide funding to these startups, but they often also bring technical or managerial expertise, such as onboarding new staff with prior industry experience to improve the target firm.

- Venture Capital (VC) is a form of private equity financing that provides capital to early-stage, high-potential, growth startup companies in exchange for equity or an ownership stake.

- The primary purpose of VC is to support startups and small businesses with strong growth potential that lack access to traditional financing sources like bank loans.

- VC funding typically occurs in stages, including seed funding, early-stage financing, and later-stage financing, each supporting different phases of a startup’s development and growth.

- Common exit strategies for venture capitalists include initial public offerings (IPOs), mergers and acquisitions (M&A), or selling their shares to other investors, which allow them to realize returns on their investments.

Venture Capitalists: Funding stages

VC is used as an umbrella term for all stages of funding. In reality, there are many different times when a VC fund may invest in a company's lifecycle. Some of them even have distinct funds that specialize in each of these stages since the needs of the businesses are so different.

Angel Investors

An angel investor is an investor who provides financing for small companies or entrepreneurs, usually before the start of any official equity funding. They are often friends or family of the small company/entrepreneur who invest their own money and are usually investing in the person as much as the business itself. As a result, angel investors often take a more hands-on approach to their investments.

Seed Funding

The seed funding stage is designed to fund the development of an idea into an actual business that generates revenue. Along with the financing from angel investors, seed funding is often the first stage in which venture capitalists get involved. Funds are also usually provided by friends and family close to its founders in exchange for an equity stake in the company or for a share in the profits made from its products.

Series A Funding

Once a business develops a track record of growing revenue, the Series A round of funding can scale the business to expand into additional markets and expand its user base and product offering with a focus on growing revenues.

The investors involved in the Series A round are usually from more traditional VC funds, which usually contribute in the range of $1 million to $10 million in total funding. This money allows management to execute the business plan and develop a business model that will generate long-term profit.

Series B Funding

As the business matures, the Series B round of funding is focused on taking the business past the developmental stage. Series B appears similar to Series A in terms of the processes and investors, although a new wave of VC firms that specialize in later-stage investing may also join the round.

The investments typically lie in the range of $7 million to $10 million, with the main purpose of ramping up talent acquisition so the company is equipped with key players necessary to execute its business plan.

Series C Funding

Series C funding is designed to give a business the capital it needs to perfect its business model. The concept of the business is proven and considered less risky at this point. Capital raised ranges from $1 million to $100 million and can be used for a variety of purposes, such as the acquisition of competitors for geographic expansion, intellectual property, or talent.

Series D, E, F... Funding

A company may choose to offer additional rounds of funding for various reasons. Most of the time, it is in efforts to scale their business to new heights. Each subsequent round is typically represented by a subsequent letter.

How is a venture capital fund structured?

The structure of the fund is a limited partnership: the VC firm is a general partner, and investors are limited partners. The limited partners are usually sovereign wealth funds, mutual funds, pension funds, endowment funds, insurance companies, etc.

All the partners have an ownership stake in the fund. However, only the general partner manages the partnership.

How Do VCs Operate?

VCs operate by pooling funds from various investors and then using the pooled funds to invest in many startups, thereby reducing the risk while improving return prospects.

It is usually beneficial for investors to invest through VC funds, as they share the risk with other investors, thereby reducing their own.

Another benefit is that they can take on a much broader position, which would have been impossible had they used just their funds. The operations of a VC fund can be divided into three stages: raising capital, investing, and repaying profits.

VC Firms: Raising Capital From Investors

The first step in raising capital is to define the objectives of the fund. Next, the GPs set a target fundraising threshold, which is the capital they look to raise from the limited partners.

The fundraising can take from months to years, and it all depends on the GP’s reputation, strategy, and market situation. Once the target capital is raised, the fund is usually closed to new investors.

The Investing Process

The next important thing for the fund to do is to invest in startups for three to five years. The main goal here is to provide as many resources as possible. The resources include financial capital, industry knowledge, sales enhancement, product development, etc.

In the business financing round, it's common to have one "leading" fund investor of the round. Often that investor (in our case fund) sets the key terms and negotiates the prices.

Generation And Distribution Of Returns

The fund generates returns through exit opportunities. In general, there are three exit scenarios for portfolio companies:

- Direct share sale to another entity

- Merger with or Acquisition by the strategic buyer or private equity fund

- Initial Public Offering (IPO) on a public stock exchange

Funds might distribute returns either after they close all of their deals or after the close of each deal.

There are two fees that LPs must pay for GP (the fund manager firm):

- Management fee. The annual payment is used to cover the operational expenses of the fund. The common industry standard is 2%.

- Carried interest (carry). The performance-based fee earned by VCs. Usually set to 20% of the profits.

Risk management procedures of the fund

VC firms and institutional investors alike are careful to limit their risk of loss and, depending on their bargaining power with the founders, will demand special treatment on their investments relative to the shares of the founders. This can happen in several ways:

-

Preferred stock (in the context of VC funding) enjoys seniority over common shares as well as potentially different voting power.

-

Convertible preferred stock has the option to convert into common shares at some future time.

-

Convertible debt enjoys even higher seniority than any equity-like claims while it remains a debt. At some future point in time, debtholders may decide to convert their stake into equity to acquire ownership and voting rights, often at discounted prices. However, this early-stage convertible debt often carries low or even no interest at all.

Private Equity Vs. Venture Capital

Venture funds tend to invest:

- In risky, early-stage growth firms

- Using equity only

- To acquire <50% of ownership

- In more innovative industries (tech, fintech, biotech, etc.)

- Diversely to spread their risk and find one profitable deal that overweighs all losses

- In small amounts across different startups

Private equity funds tend to invest:

- In less-risky, mature firms

- Across a variety of industries

- To acquire > 50% of ownership

- Using debt and equity

- In large amounts concentrated in mature private companies

VC firms: roles, salary, and daily work

There are many different roles within a VC firm, but usually follow a strict hierarchy ranging from an analyst up to a partner.

Roles

The most junior role in a VC firm is that of an analyst. These people are typically MBA students pursuing an internship or fresh university graduates. The primary responsibility of an analyst is to conduct market research and study the company and its competitors.

Analysts also attend conferences and try to scout deals that might lie within the investment strategy or thesis of the fund that the VC firm is investing out of. An analyst can expect to make between $80K - $150K in yearly compensation.

Associates are immediately after analysts and can either be junior or senior. Most associates tend to come with a financial background with powerful skills in building relationships.

They do not make investment decisions in a firm but work closely with those who do. An associate's salary can range from $130K - $250K a year.

Above associates, you can find principals. Principals are senior people who can make investment decisions but do not have full power in the execution of the overall strategy of the firm.

A principal can expect to make around $500K - $700K in yearly salary and a bonus of $1M - 2M in carry.

The most senior role within a VC firm is a partner. Partners could be general partners or managing partners, depending on whether the individual just has a voice in investment decisions or also in operational decisions.

In addition to making investments, partners are also responsible for raising capital for the VC firm’s funds. A partner's salary typically exceeds $1M with around $3M - 9M in carry bonus.

Much like private equity compensation, pay in VC funds also includes a carry bonus, which may result in a large payout depending on the performance of the firm.

To learn more about careers and compensation in the VC space, visit our

- Guide to Private Equity Careers & Venture Capital Careers

- Venture Capital Salary & Compensation, Average Bonus in Venture Capital.

A Day In The Life Of A Venture Capitalist

In VC firms, analysts mainly do a combination of research, modeling, and other miscellaneous things - and this changes as you climb the ranks. Here is some insight into working at a VC firm from @Associate1.

“It honestly depends on week-to-week. On average, maybe sourcing is 25-30% of the job?

There's a lot of follow-up work involved when sourcing (i.e. light DD) and if you decide to move forward, DD gets more intense (research, memo writing, customer calls, talking to other investors, etc.)

I also don't do much cold calling; a lot of my sourcing comes from my existing network, the network of friendly investors, accelerators, things that the partners ask me to look at, etc. This eliminates a lot of the headache/time hassle associated with banging your head against the wall doing only cold sourcing.”

Venture Capitalist Working Hours

What are the hours like working at a VC firm? Do those hours vary by the firm? Answers to all of those questions from @care1g.

“Really depends on the stage of fund (early vs. growth / late-stage) and "reputation" of the firm. The Associates at the top late-stage / growth equity funds often work very late hours because their deal flow is top-notch and they see every opportunity.

VC is also a role where ideation starts from the bottom.

Associates are tasked with building thematic market maps and are constantly sourcing/finding new deals in their spare time. Generally speaking though, the hours are less than traditional private equity.

Processes and time to term-sheet in VC are way faster than private equity and sometimes decisions to move forward with a deal are made within weeks vs. months in traditional PE. I typically work 40 - 60 hours per work with no weekend work. If there is a live deal, that number is more like 60 - 80 hours.”

Check out this video about The Road to VC through Investment Banking!

Examples of venture Capital Firms

Here are examples of some of the most renowned VC firms and their best investments:

Sequoia Capital

Sequoia Capital is a renowned U.S. VC firm founded in 1972 that partners with companies in early- and late-growth stages across all sectors. In recent years, they have been focusing on the internet, mobile, healthcare, financial, and energy companies.

Sequoia Capital turned its $60 million investment in WhatsApp into $3 billion after Facebook’s $22 billion acquisition in 2014, making it the largest private acquisition of a VC-backed company ever at that time.

Accel

Accel, founded in 1983, is a US VC firm that operates in California, London, China, and India. They primarily invest in technology-related companies in their early growth stage, as well as some seed investments.

Accel is best known for its early investment in Facebook, co-leading Facebook’s $12.7 million Series A in 2005 with a 15% stake. When Facebook went public in 2012, Accel’s stake was worth $9 billion, representing a 700x return on their investment.

Kleiner Perkins

Kleiner Perkins is an American VC firm based in Silicon Valley founded in 1972. They specialize in investments in incubation, early-stage, and growth companies in the technology space. Kleiner Perkins was an early investor in Google, funding $12.5 million in their Series B round in 1999.

A year after Google’s IPO in 2004, Kleiner Perkin’s stake was worth about $4.3 billion - a 300x return.

Andreessen Horowitz

Andreessen Horowitz was founded in 2009 in Silicon Valley, California, and primarily backs seed to late-stage technology companies. They specialize in investments across consumer, enterprise, bio/healthcare, crypto, and fintech spaces. Andreessen Horowitz is the biggest investor in Coinbase, a cryptocurrency exchange platform.

The famed VC firm led a $25 million Series B round, securing shares at $1 apiece. When Coinbase went public in April 2021, its stake was worth almost $10 billion - almost 400x return on investment.

Benchmark

Benchmark is a San Francisco-based VC firm founded in 1995 that focuses on early-stage investing in several markets, including enterprise software and services, communications, mobile computing, and financial services. Benchmark invested $13.5 million in Snap Inc.’s Series A in February 2013 as the sole investor in the round.

When Snap Inc. went public in March 2017 at a $25B valuation, it was the second-highest valuation on the exit of any social media and messaging company since 1999, valuing Benchmark’s stake at about $3.2 billion.

Founders Fund

Peter Thiel’s Founders Fund was founded in 2005 as a San Francisco-based VC firm investing in science and technology companies building revolutionary technologies. The firm invests in all stages across a wide variety of sectors, such as aerospace, artificial intelligence, and consumer internet.

Founders Fund funded $200 million into a small biotech startup called Stemcentrx, which developed innovative therapies for cancer patients. In April 2016, the drug company AbbVie paid $1.9B in cash and $3B in stock to buy Stemcentrx, where $1.7 billion went to the company’s largest individual investor, Founders Fund.

New Enterprise Associates

NEA is a US-based VC firm founded in 1977 that focuses on seed to growth-stage companies in technology and healthcare.

Their most notable VC investment was in Groupon, leading its Series A round in 2008 by putting in $4.8 million. Groupon’s IPO in 2011 was the biggest IPO by a US web company since Google went public in 2007, and NEA’s 14.7% stake was worth about $2.5 billion.

Union Square Ventures

Union Square Ventures is a New York City-based VC firm founded in 2003 and famous for backing startups, including Tumblr, Etsy Stripe, and Coinbase. They specialize in early-stage, growth capital, late-stage, and startup financing.

In 2007, USV led Twitter’s $5 million Series A, beating out CRV, Kleiner Perkins, Benchmark, and Insight Venture Partners for the opportunity to invest in the early social media network. Twitter’s IPO in 2013 valued the company at $14.2 billion, making Union Square Ventures' stake worth $863 million - a 170x return.

Greylock Partners

Greylock Partners is one of the oldest VC firms, founded in 1965 out of Silicon Valley. They primarily invest in seed-stage, early-stage, and later-stage companies in the software, SaaS, heath-tech, artificial intelligence, and other technology sectors.

Greylock Partners realized a 9x return of $700 million on their $80 million investment into Workday, a financial management, and human resources software vendor when the company went public in 2012. It was the highest-priced venture-backed public offering since Facebook’s, raising $637 million.

First Round Capital

First Round Capital is a San Francisco-based VC firm that specializes in providing seed-stage funding to technology companies. Specifically, they target technology companies in the enterprise, consumer, hardware, fintech, and healthcare industries.

First Round Capital was an early seed investor in Uber, funding $510,000 at a $4 million valuation. Uber’s IPO in May 2019 valued the company at $75.5 billion, making the San Francisco VC firm’s stake worth $2.5 billion - a whopping 4900x return.

These are some of the top VC firms as of now. Use the WSO Company Database to find more information about each company and many more in the VC world.

How do Venture Capital firms make money?

VCs make money through management fees and carry interest (carries). Management fees are generally a percentage of the total amount of capital being managed. Traditionally, this figure has been 2% per year.

For example, a VC fund managing a $100 million fund for its investors will charge $2 million per year to pay salaries and other operational expenses of the fund. The other way VCs make money, and often the most lucrative, is through carried interest. Carried interest is basically a percentage of the profits made from investments, which normally lie between 20% and 25%.

In order to cash out and receive the carried interest, a company within a VC firm’s fund has to be acquired or go public through an IPO, where investors are able to liquidate their position.

venture capital funding: Hard Truths

Securing venture capital is not easy and can often take years before an entrepreneur can secure any funds.

Imagine trying to borrow money from someone who doesn't know anything about you; access to venture funds is very limited for start-ups without a track record. VC firms rely heavily on informal networks to help identify potential investments.

These firms may receive hundreds or thousands of funding requests and may only listen to a handful of entrepreneurs and invest in one. Personal connections matter, and as a corollary, the personalities of the founders matter!

It is no coincidence that many founder-CEOs are strong and shrill personalities: Elon Musk (Tesla), Adam Neumann (WeWork), and Elizabeth Holmes (Theranos).

Venture capital can be a very expensive form of financing for the founders. VCs will try to extract as much as they can from the founders. Even in a very successful firm, founders regularly end up owning less than 20% of their firm after a few rounds.

The use of convertible debt protects the venture capital investors but severely dilutes existing shareholders in case of a “down-round”, that is, a round of funding that values the firm below the previous valuation.

As VCs grow their ownership, they will become more hands-on in questions of strategic decisions and will attempt to have their associates sit on the board. It is not uncommon for the founder-CEO to eventually be fired from their own firm.

In 2017, this happened to Travis Kalanick, who was one of the 2 founders of Uber.

Related to the second point, VCs’ and founders’ incentives are frequently not aligned. From the perspective of the VC, they are looking at each stake in a young firm as a "lottery ticket" in a portfolio of 20-100 others.

The optimal strategy is to grow every firm as quickly as possible to find out whether it has that 100X potential of Facebook or PayPal.

The founders, however, have all their human capital tied up in a single firm and would prefer to grow sustainably and organically to maximize the chance of survival at the expense of “moon shoot growth,” which leads to boom or bust within a short period of time.

Why Do Venture Investments Fail?

The main reason is senior management issues in startups. The majority of founders don’t consider the business aspect of the firm and are only concerned with the operations/technical side. That is the reason why many investment-backed startups fail.

If you are looking to break into VC but don't know how to, be sure to check out our VC Course. Below is a sample video to kickstart your journey into the VC space.

Everything You Need To Break into Venture Capital

Sign Up to The Insider's Guide by Elite Venture Capitalists with Proven Track Records.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?