Investment-Grade Bonds

A bond that is believed to have a lower risk of default and has received higher ratings by credit rating agencies

What Are Investment-Grade Bonds?

An investment-grade bond is defined by the Securities and Exchange Commission (SEC) as a bond that is believed to have a lower risk of default and has received higher ratings by credit rating agencies. As a result, such bonds tend to be issued at lower yields than less creditworthy bonds.

These instruments are just another form of bonds and specify corporate and government debt deemed “safe” and likely to be paid back with interest.

As you may know, companies and the government tend to issue debts to raise capital and finance new projects/investments. It is similar to an individual taking out a loan to purchase a car or house, as the debt must be paid back.

Every bond has a risk directly correlated with the issuer’s ability to pay its debt. To account for this, investors have several bond labels to determine the likelihood of debt repayment. Rating agencies determine this bond rating.

Investment-grade bonds are considered the most reliable and are issued a rating of BBB (S&P and Fitch) or a Baa3 (Moody’s). We will go into detail regarding bond categorization and rating assessments below.

-

Investment-grade bonds are safer and have lower default risk, offering reliable but lower yields compared to riskier bonds.

-

Credit rating agencies assess bonds and assign ratings based on creditworthiness, with investment-grade bonds typically rated above BBB or Baa.

-

The 2008 financial crisis exposed how misleading AAA ratings on risky securities contributed to the meltdown.

-

Investment-grade bonds perform well during economic downturns but may see reduced demand during optimistic market periods.

-

Pros of investment-grade bonds include lower risk and stable returns, but cons include lower yields, potential liquidity issues, and higher buy-ins. Consider bond funds or ETFs for easier access.

History of investment-grade bonds and the rating scale

Historically, trading has allowed businesses to give loans to consumers based on their confidence in repaying. Wealthy and trustworthy individuals are naturally more likely to pay off loans. They are like investment-grade bonds in today’s terms.

Credit agencies originated in the United States during the early 1900s. Starting with publicly issued railroad bonds, credit ratings soon emerged with the formation of the big 3 rating agencies, as they initiated letter grading on the quality of financial instruments.

Events such as the Glass-Steagall Act in 1933 further consolidated the function of rating agencies, as commercial banks were separated from investment banking. As a result, investors needed more transparency on corporations, and credit ratings played a considerable role.

With the end of the Bretton Woods system in 1971, global financial expansion was propelled by the SEC explicitly referencing credit ratings. During this period, the number of debt issuers grew exponentially, which also led to the Big 3's growth.

Standards & Poors, Moody's, and Fitch — Rating Agencies

To understand investment-grade bonds, it is crucial to comprehend the overall credit rating scale assigned by the big 3 rating agencies: Standards & Poors, Moody's, and Fitch. This is because the rating scale from the three agencies is identical.

A credit rating is essentially a valuation of a company's creditworthiness. It is represented by variations of letters and numbers ranging from A-D, with a triple-A being the highest quality and C or D being the lowest quality, also known as default.

Investment-grade bonds are issued credit ratings above BBB (S&P and Fitch) or Baa (Moody's), which includes BBB, A, AA, and AAA. BBB is the bottom line, typically associated with medium risk, while the rest of these bonds have a lower risk.

For clarification purposes, any rating below BBB would be considered speculative and labeled a junk-grade bond by credit agencies. This includes BB, B, CCC, CC, C, and D, the other possible company credit ratings.

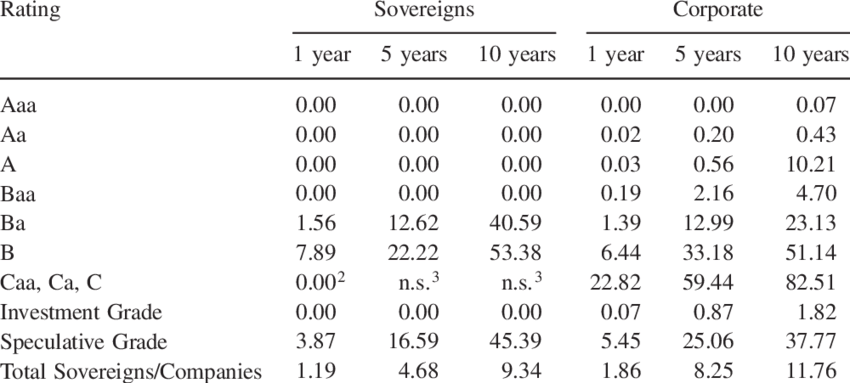

Credit rating and default probability usually match accurately for short-term bonds but may vary for long-term bonds because more variability comes as time goes on.

Research by ResearchGate depicts this clearly with statistics on sovereign and corporate bonds. For example, for the corporate bond column, one can observe that 1-year and 5-year bonds' default rates significantly increase as the rating decreases, but this does not apply to the 10-year column.

For the 10-year corporate bonds, bonds with the A credit rating had a much higher default rate than Baa. Although both are investment-grade bonds, it can be inferred that the credit rating for long-term bonds tends to be more unpredictable.

How are investment-grade bonds rated?

Rating agencies use a range of intrinsic and extrinsic factors to determine the right level of risk for bonds, just like how an investor would approach the analysis of a stock.

Internal criteria include the analysis of the company's overall health, its balance sheet, free cash flow, etc. External measures include its partnership with other corporations and its network of influence.

In addition to intrinsic and extrinsic analysis, rating agencies also look at specific measures for different industries and coverage groups and forecast economic conditions. As a result, the rating process can be pretty complicated.

To rate a bond as investment-grade, the rating agency must first be assured of the company’s financial capacity to pay back the bond and interest.

The highest quality investment-grade bonds (AAA, AA) are highly stable financially and leave a minimal chance for potential default. For example, the graph shows that corporate bonds with such ratings have a default rate below 0.5%.

Moving down the list, bonds with A and BBB ratings remain relatively stable. Still, their capital structure and industry may be more susceptible to changes in economic conditions and unforeseen circumstances.

Case Study—2008 Financial Crisis

Having talked about the rating process and the usual reliability of credit ratings, there have been anomalies caused by manipulating securities through fraudulent ratings. The 2008 financial crisis is a prominent example of this.

Most are aware of the subprime mortgage story of the Great Recession, which led to millions of people losing their homes and life savings and the collapse and bailouts of critical financial institutions.

The role that rating agencies played is less conspicuous but undeniable.

The scene in the movie “The Big Short” did an excellent job of briefly explaining what went down. For example, suppose an entity came to a rating agency asking for an investment-grade rating on a bond or derivative. In that case, the rating agency says yes because, otherwise, the party will approach their competitors.

This phenomenon and the nature of greed propelled rating agencies to assign a considerable portion of the debt securities market with the AAA rating. This is considered the safest rating at the investment-grade level.

Behind these AAA rating securities were investments from mezzanine tranches and worse, which contained ratings of A-, BBB, etc. Rating agencies disguised risky investments as securities with a 0% chance of failing by giving them AAA ratings.

The hoax could not last forever, and in 2009 these supposedly “AAA investments” were suffering huge losses and downgrades. Many ended up getting downgraded to junk and even suffered principal loss, which meant investors lost their initial investment too.

Economists like Joseph Stiglitz blamed rating agencies as one of the key culprits that led to the 2008 financial meltdown, as their ratings were misleading and kept investors in the dark about what they were buying.

Although the big 3 rating agencies have a history, methodology, and solid reputation, they are not subject to deception and failure. The case study of the 2008 financial crisis is a perfect example of greed clouding rational judgment.

How does the economy affect investment-grade bonds?

Bonds rated investment-grade are generally less likely to default but have an inherently lower yield rate than junk bonds.

These bonds are considered safe and conservative investments and tend to be reliable during periods of economic downturn. However, their demand slightly decreases when markets are optimistic, as investors opt for riskier high-yield bonds.

Interest rates can also impact such bonds, depending on the term duration of a particular bond. Naturally, bonds with a higher duration tend to be more sensitive to changes in interest rates.

Bonds of investment grade tend to be of a longer duration, allowing them to be more affected by slight changes in interest rates. As a result, they tend to behave similarly to high-quality government bonds.

Junk bonds, however, are slightly less susceptible to interest rate changes as they are generally shorter-term investments.

Investment-grade bonds tend to benefit more from decreases in interest rates, and their value will usually rise faster than junk bonds under such circumstances.

Investment Grade Bonds Advantages & Disadvantages

Investment-grade bonds can prove to be safe investments that yield stable returns, but investors should clearly understand their pros and cons so that their judgment is sound.

Some of the advantages are:

- Less risk: Bonds rated with the investment grade (BBB-AAA) are less risky and volatile than stocks. Bonds are inherently safer than stocks because bondholders are paid out before stockholders in the worst-case scenario of bankruptcy.

- Stable revenue source: Bonds with the highest rating provides a steady source of revenue and can be effective as a source of hedging and diversification.

- Higher yield among safe investments: Although investment-grade bonds do not carry the highest yield rate, they typically earn more than secure investment options such as treasuries.

On the other hand, the disadvantages are:

- Lower returns: Bonds carry a lower return than stocks, but this goes for all types of bonds. Although riskier, high-yield bonds have a higher return than their investment-grade counterparts.

- Less liquid: Bonds are slightly less liquid, and investment-grade bond positions may take time to be offloaded. These bonds typically have to be redeemed upon maturity date, and selling them before maturity may come at a loss.

- Less transparent: Bonds of all grades are traded over the counter and therefore are less evident. It could sometimes lead to investors paying more money than they have to.

- High buy-ins: If one invests directly in an individual bond, it would require a high buy-in as most bonds are issued in $1,000 increments. Bonds do not have partial shares, so buying a personal bond would require substantial capital.

Investment considerations

After reviewing the pros and cons of investment-grade bonds, it is time to consider how to invest in them.

Considering transparency issues, the average investor might have more difficulty buying bonds directly. Instead, experts suggest the investment be made through purchasing mutual funds, index funds, and ETFs.

Bond funds are much easier to navigate than individual bonds and are typically less expensive. Investors can make such purchases through a standard brokerage account with zero commissions and low expense ratio fees.

The easiest way to view bonds and their yield rates would be via a brokerage. These firms typically have entire pages dedicated to fixed income securities like bonds, certificates of deposit (CDs), etc., with the precise classification of their investment grades.

Take Fidelity’s platform, for example. Investors can view the highest and median yields for fixed income securities, including investment-grade, municipal, and US treasury bonds, with maturity ranging from 3 months to 30+ years.

Researched and authored by Kevin Wang | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?