Mortgage Servicing Rights (MSR)

A contractual agreement that gives the right to service an already-existing mortgage.

What Are Mortgage Servicing Rights (MSR)?

Mortgage Servicing Rights (MSR) refers to a contractual agreement that gives the right to service an already-existing mortgage.

Usually, such an agreement is bought by the mortgage company, most commonly a major financial institution such as a bank or a third party that owns resources that allow it to service the mortgage.

Purchasing the rights to service a mortgage means that the servicer may need to handle the following tasks:

- Administrative duties to manage loan

- Collect monthly mortgage payments and other dues

- Ensure that a mortgage lender receives dues

- Tackling complex borrowers and missed payments

- Set aside taxes and insurance premiums in an escrow for management

- Forward principal and interest payments to the lender

- Other debt management duties

Hence, the responsibilities that the servicer is tasked with are routine loan management duties. For the servicer's work, the fee charged to the lender ranges from 0.25% to 0.5% of the mortgage balance.

- Mortgage Servicing Rights (MSR) are the contractual rights a mortgage lender or servicer holds to service a loan, including collecting payments, managing escrow accounts, and handling delinquencies.

- MSRs represent the financial interest in the servicing fees and related income generated from managing a mortgage loan, which can be retained by the lender or sold to investors in the secondary market.

- Servicing rights generate income through servicing fees, late fees, and interest spreads, contributing to the profitability of mortgage lending operations.

- MSRs are actively traded in the secondary market among financial institutions, investors, and specialty servicing firms seeking to optimize their portfolio returns and mitigate risks.

History of MSRs

The mortgage servicing rights (MSR) market has seen many changes. This section will highlight some of these developments and their implications.

In 2011, the Federal Reserve and the OCC took action against several major financial institutions by mandating improvements to servicing practices. The OCC, in particular, took steps to identify and address unsafe and unsound foreclosure practices.

This development meant that banks faced regulatory issues when handling their non-performing loans.

However, nonbank servicers were willing to handle these loans because of their cost and technological advantages. Therefore, banks increasingly outsourced the servicing of these assets.

Moreover, during this time, Fannie Mae introduced the “High Touch Servicing Program,” which made it simpler to facilitate the transfer of non-performing assets from banks to servicing companies.

In 2013, the Internal Revenue Service (IRS) issued a Private Letter Ruling (PRL) that incentivized REITs to invest cash flows into MRS instruments.

The PRL made it possible for some instruments to qualify as assets for REITs to hold and invest in, encouraging them to invest in MSR.

In January 2014, new servicing standards were set by the Consumer Financial Protection Bureau (CFPB). These requirements applied to banking institutions and special servicers with assets over $10 billion. The standards are meant to protect consumers.

Today, the mortgage servicing market (MSR) and its corresponding financial instruments continue to gain popularity. As interest rates are rising in today's economy, we find that the MSR market stands to achieve for the foreseeable future.

Impact of Interest Rates on MSR

Several reasons exist for determining the performance of MSR instruments. Today, the market for these instruments is strong because of much safer loan originations after 2008, reducing the risk of defaults.

Historically, the value for such instruments has risen as interest rates increase and, conversely, has fallen when interest rates decrease.

This directly proportional relationship holds because the likelihood of a borrower paying off the mortgage faster, i.e., making prepayments, falls as interest rates rise.

This phenomenon was observed recently as rising interest pains continue to devastate the industry; the MSR market stands out as it thrives in this environment, as reported in this article.

This relationship means that the servicing company will receive mortgage fees for a longer time as interest rates rise and prepayments fall.

Moreover, about interest rates, as interest rates rise, borrowing costs rise, and thus, individuals and firms have an incentive against borrowing capital.

Therefore, to some extent, in such an environment, the servicing firm will have a lower pool of public debt that can be serviced.

This means servicing firms can face downward pressure on the commission due to an increasingly competitive environment.

Impact of Housing Market Fluctuations on MSR

Housing market fluctuations can directly impact the stability of the servicing industry. For instance, consider the scenario of the 2008 financial crisis, where real estate saw a sharp downturn with innumerable defaults on payments.

In such an environment, servicing firms face pressure, as the debt they are servicing faces a much higher default risk. Ultimately, this causes the firm's stability and the industry to decrease.

Moreover, the clients of servicing firms, usually big banks, face a financial crunch in this challenging environment. Thus, the servicing firm must navigate many challenges in such a hypothetical scenario.

When the housing market is strong, the public mortgage debt outstanding increases, as individuals and firms need more capital to purchase real estate. Therefore, servicing firms may capitalize in such an environment by raising commissions due to an optimistic atmosphere.

Although the risks mentioned above exist for the MSR market, mortgages and MSRs are still popular among Real Estate Investment Trusts (REITs), hedge funds, banks, and retail instruments because of the stable cash flow yields.

Outsourcing Mortgage Servicing Rights

Lenders incur costs when mortgage servicing rights are outsourced, as the servicing firm requires a fee for providing such services. Therefore, lenders need to analyze whether the commission charged by a servicing firm is worth it.

Several factors cause lenders to outsource such services. This may include:

- Managing surges in loan requests

- Freeing up existing resources for allocation to income-producing activities, such as evaluating the credit-worthiness of borrowers, instead of managing existing debt

- In many cases, it can be more cost-efficient to outsource mortgage servicing to third parties, as they specialize resources in the space.

- Frees up lines of credits

Perhaps the most crucial reason lenders have a solid incentive to outsource servicing duties that the lender can focus its resources on its core business, including issuing new mortgages and working with borrowers.

Moreover, the lending firm can cut costs on servicing duties and focus capital on the core business of the lending firm, which, again, is initiating and approving mortgages for credit-worthy individuals.

Due to the reasons above, the lending industry has increasingly shifted to outsourcing servicing to third-party firms.

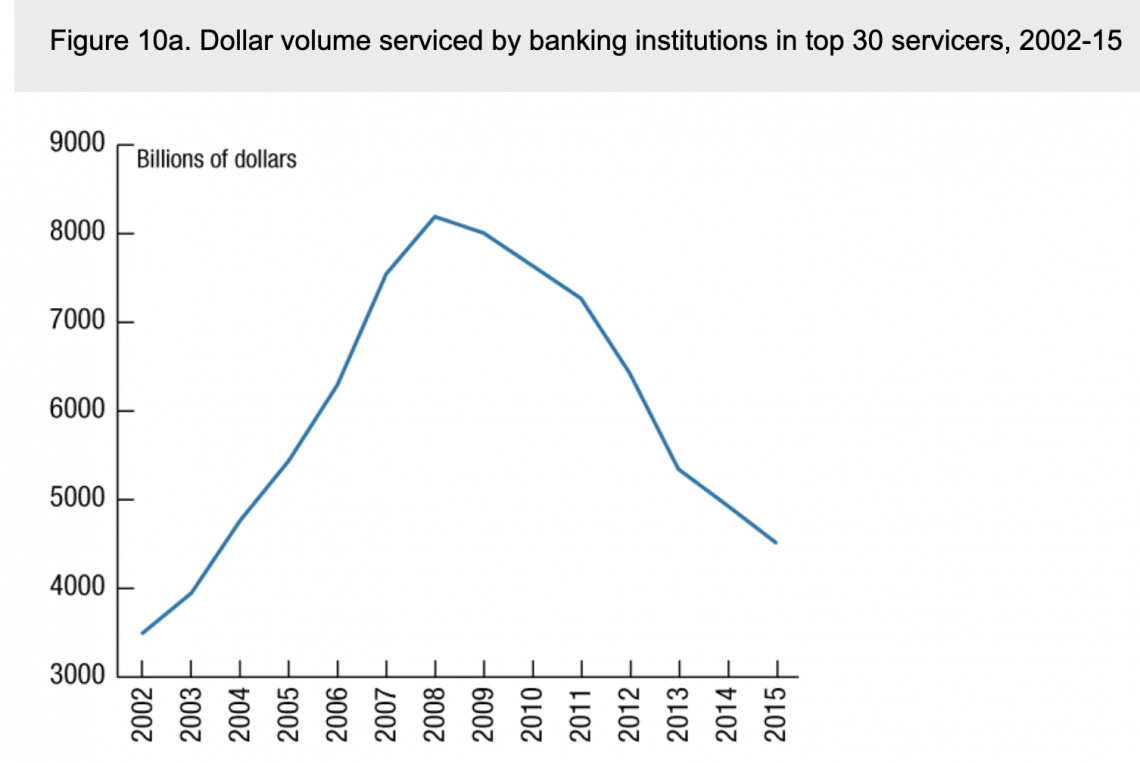

This is evident from the chart below, which shows a sharp fall in the pool of debt serviced by banking institutions. This implies that the debt is serviced by servicing firms and some non-bank lending firms.

Lenders do not legally need to ask for permission from the borrower to transfer servicing rights. Even so, the lender needs to step in when a complicated situation arises, such as when a borrower cannot make payments and is not complying with the agreement.

Therefore, lenders find it profitable to pass mortgage servicing rights to a third party, usually saving costs, and experience the added benefit of not worrying about servicing the debt.

What MSR Means for Borrowers

For the mortgage borrower, nothing about their loans changes except that a third party handles the administrative duties and loan management. So as far as the borrower is concerned, they are dealing with a different party when inquiring about their loan.

This means that the loan amount, interest rate, monthly payment, total payable amount, and other factors are the same as before.

Thus, it is imperative to understand that lenders recognize that borrowers do not usually have much preference when dealing with a third party or their lender when making payments.

Federal banking laws today allow lenders to sell mortgage servicing rights or transfer them to another party without the borrower's consent. However, in case of a transfer or sale, the borrower shall be notified fifteen days before the changes.

Borrowers may sometimes encounter issues with the third party servicing their mortgage. In such an instance, a complaint should be filed with the Consumer Finance Protection Bureau.

If you have a student loan, you can make a query to the Federal Student Aid Office of the Department of Education. A suspected fraud case can be reported to the Federal Trade Commission (FTC).

Mortgage Servicing Rights Example

Consider the following example of a lender firm selling its mortgage servicing rights to a third-party firm specializing in such operations.

Here are some pieces of information associated with this example:

- The lending firm has decided to service 40% of its receivables (mortgage payments), which amounts to $20 million.

- The debt is expected to be paid off at an average of 35 years; therefore, the yearly payments that are collectible amount to about $571,428 ($20 million/35), on average.

- The cost of servicing this debt, charged by the servicing firm, is 0.25% of the total mortgage amount; this amounts to $500,000

Given the above information, the lending firm, usually a bank, can outsource its duties to a third-party firm for a fee.

As discussed before, sometimes, it may make economic sense for the lending firm to hire a specialized firm to complete such tasks, as they can achieve it at a lower cost per unit.

For the borrowers that owe the $20 million, nothing has changed except for the address to which payments are routed and the party dealing with difficulties.

Such an example illustrates the benefit that both servicing firms and lenders stand to gain in such a deal. Further, usually, borrowers barely experience any difference through such a process.

Companies That Purchase Mortgage Servicing Rights

Several firms specialize in providing services that manage mortgages. Some examples include:

-

Wells Fargo & Co (NYSE: WFC), one of the major financial services institutions, offers a variety of services, including commercial mortgage servicing, acting as the number one primary and master servicer of commercial real estate loans by volume in the U.S., according to the Mortgage Bankers Association (MBA) in 2020.

-

Flagstar Bancorp Inc (NYSE: FBC) is a banking company that is also one of the largest residential mortgage servicers in the U.S.

-

KeyBank is a retail banking company that is the primary subsidiary of KeyCorp (NYSE: KEY) and is one of the top commercial mortgage servicers in the U.S.

-

Midland Loan Services, a PNC Real Estate Business, is one of the largest third-party providers of loan servicing for commercial loans and other retail real estate industry solutions.

-

Berkadia Commercial Mortgage LLC is one of the largest commercial loan servicers.

-

CBRE Loan Services, a firm specializing in servicing loans and asset management, provides services in the U.S, Europe, and the Asia Pacific.

-

Nelnet, Inc (NYSE: NNI), a provider of student Loan and education financial servicing

-

Altisource Portfolio Solutions (NASDAQ: ASPS), a real estate loan and mortgage servicer

-

Ocwen Financial Corp (NYSE: OCN), a commercial and residential mortgage servicer

As mentioned before, the firms above manage mortgages for mortgage lenders. In exchange for servicing the mortgages, they receive a commission without even owning mortgages.

Usually, mortgage servicing firms are backed by government agencies/enterprises such as Ginnie Mae, Fannie Mae, and Freddie Mac.

Mortgage Servicing Rights (MSR) FAQs

Mortgage servicing rights are traded on a separate market. Usually, such rights are bundled up into securities. Thus, they allow investors to own bunches of servicing requests that generate consistent payouts.

Yes, mortgage servicing rights are an intangible asset, as the servicing fees collected to compensate for the servicing facilities are non-tangible. This includes collecting dues on time and dealing with delinquent tenants.

A lender can be identified as a financial institution or individual that provides a borrower with capital for interest. However, a loan servicer is an entity that manages the loan payments and works with the borrower to ensure that payments are timely made.

Therefore, a lender may also be the servicer of a loan. Although today, this is becoming increasingly less common.

Usually, this is not the case, as the servicer is interested in the borrower making payments on time to receive their fees for providing the lender with timely payments.

However, a loan servicer may own your loan if the servicer is the lender. This is the case with large banks that service some percentage of their loans.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?