As the NASDAQ approaches historic highs, Apple’s market cap exceeds that of the Bovespa (the Brazilian equity index) and young social media companies like Snapchat have nosebleed valuations, there is talk of a tech bubble again. It is human nature to group or classify individuals or entities and assign common characteristics to the group and we tend to do the same, when investing. Specifically, we categorize stocks into sectors or groups and assume that many or most stocks in each group share commonalities. Thus, we assume that utility stocks have little growth and pay large dividends and commodity and cyclical stocks have volatile earnings largely because of macroeconomic factors. With “tech” stocks, the common characteristics that come to mind for many investors are high growth, high risk and low cash payout. While that would have been true for the typical tech stock in the 1980s, is it still true? More specifically, what does the typical tech company look like, how is it priced and is its pricing put it in a bubble? As I hope to argue in the section below, the answers depend upon which segment of the tech sector you look at.

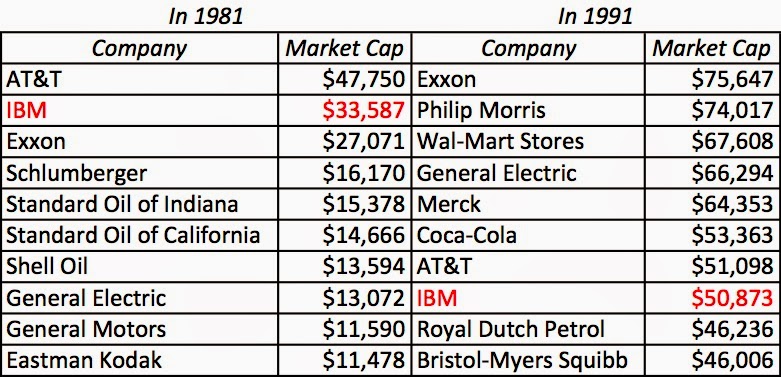

A Short History of Tech Stocks

|

| Market Capitalization at the end of each year (S&P Capital IQ) |

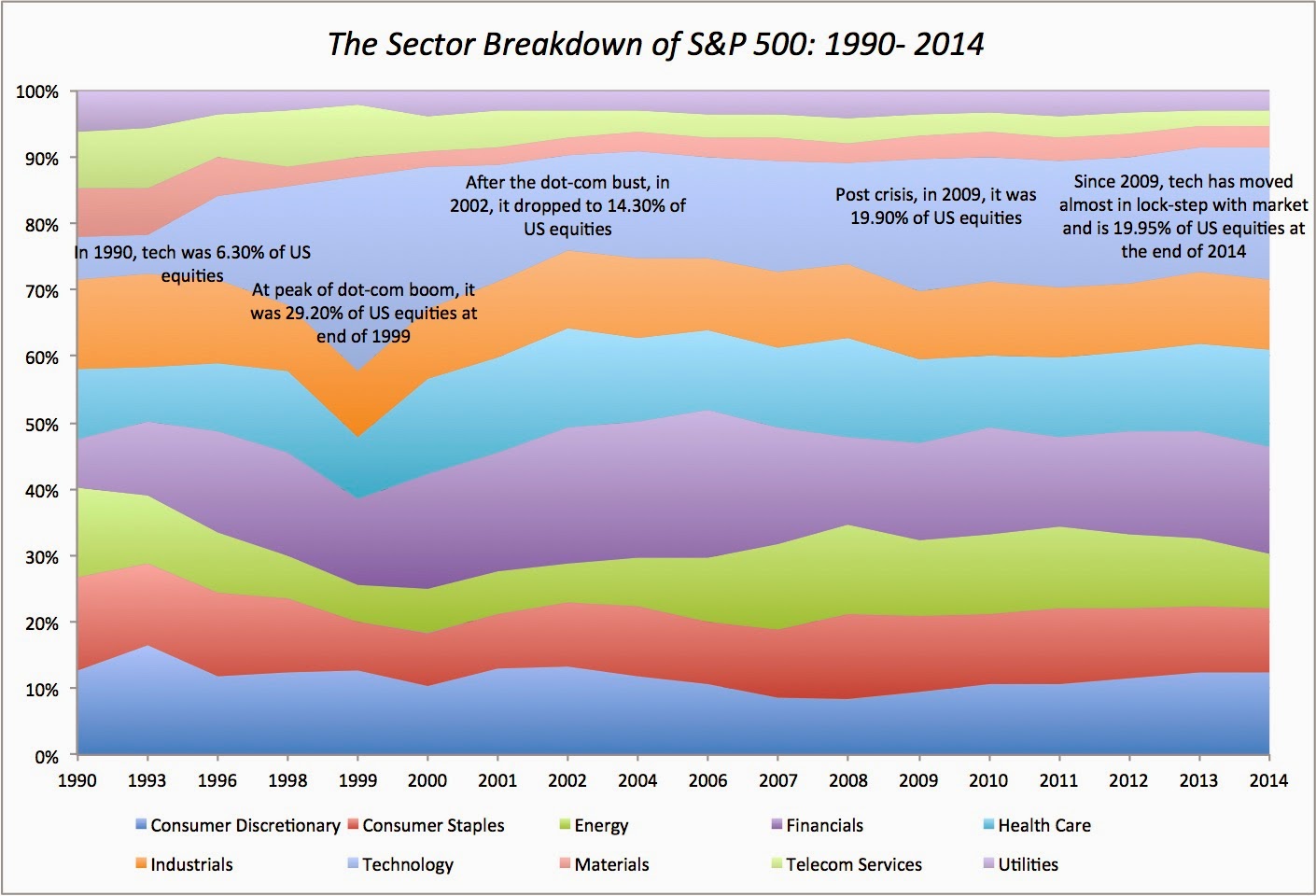

There are two things to note in this graph.

- The first is that technology as a percentage of the market has remained stable since 2009, which calls into question the notion that technology stocks have powered the bull market of the last five years.

- The second is that technology is now the largest single slice of the equity market in the United States and close to the second largest in the global market. So what? Just as growth becomes more difficult for a company as it gets larger and becomes a larger part of the economy, technology collectively is running into a scaling problem, where its growth rate is converging on the growth rate for the economy. While this convergence is sometimes obscured by the focus on earnings per share growth, the growth rate in revenues at technology companies collectively has been moving towards the growth rate of the economy.

The Diversity of Technology

|

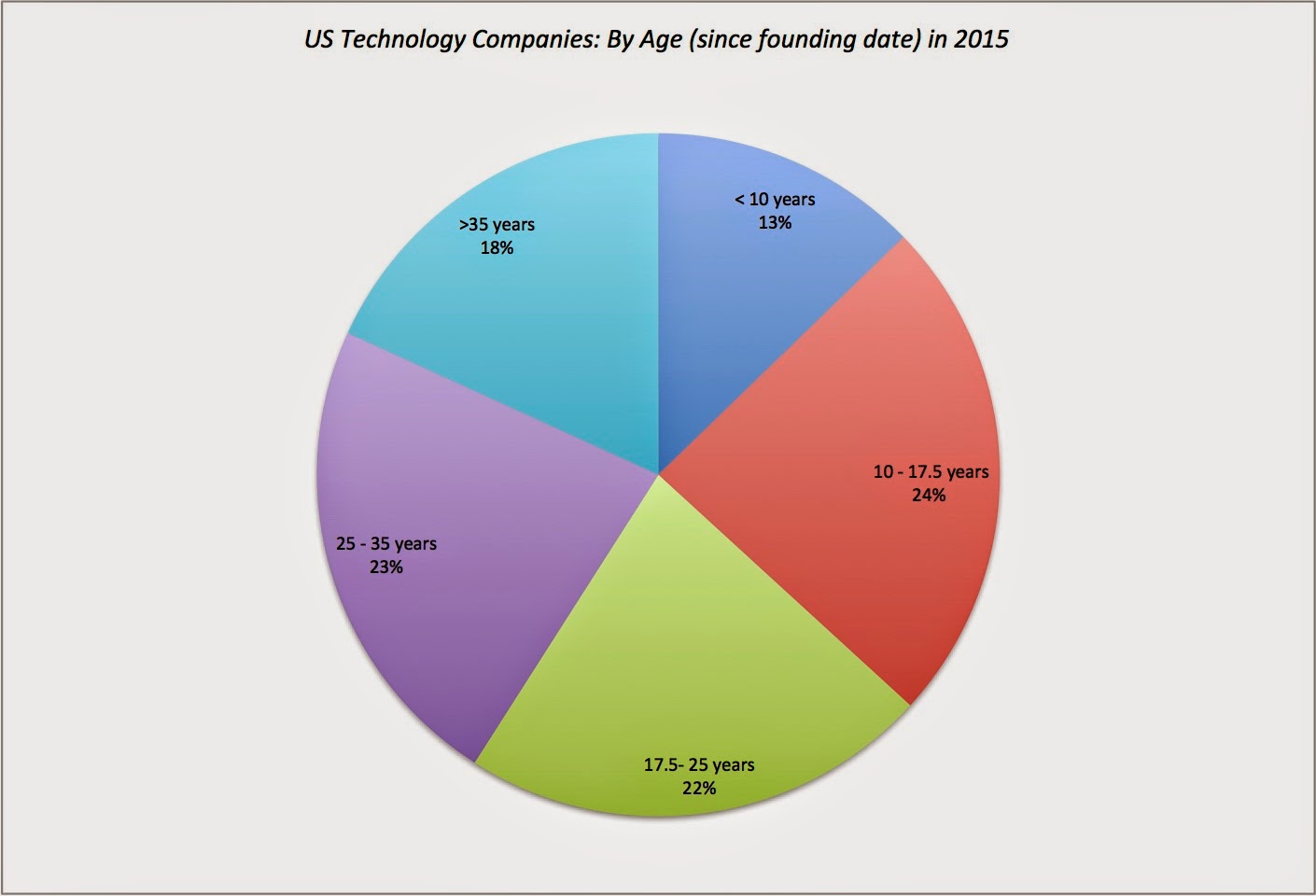

| Age: Number of years from founding of company to 2015 |

Note that 341 technology companies have been in existence for more than 35 years and an additional 427 firms have been in existence between 25 and 35 years, and they collectively comprise about 41% of the firms that we had founding years available in the database. While being in existence more than 25 years may sound unexceptional, given that there are manufacturing and consumer product companies that have been around a century or longer, tech companies age in dog years, as the life cycles tend to be more intense and compressed. Put differently, IBM may not be as old as Coca Cola in calendar time but it is a corporate Methuselah, in tech years.

The Pricing of Technology

|

| Pricing as of February 2015, Trailing 12 month values for earnings and book value |

To adjust for the fact that cash holdings at some companies are substantial, I computed a non-cash PE, by netting cash out of the market capitalization and the income from cash holdings from the net income. While it is true that the youngest tech companies look highly priced, the pricing becomes more reasonable, as you look across the age scale. For instance, while the youngest companies in the tech sector trade at 4.34 times revenues (based upon enterprise value), the oldest companies trade at 2.44 times revenues.

|

| Based on February 2015 Pricing & Trailing 12 month numbers: 2807 US technology and 6076 non-technology companies. |

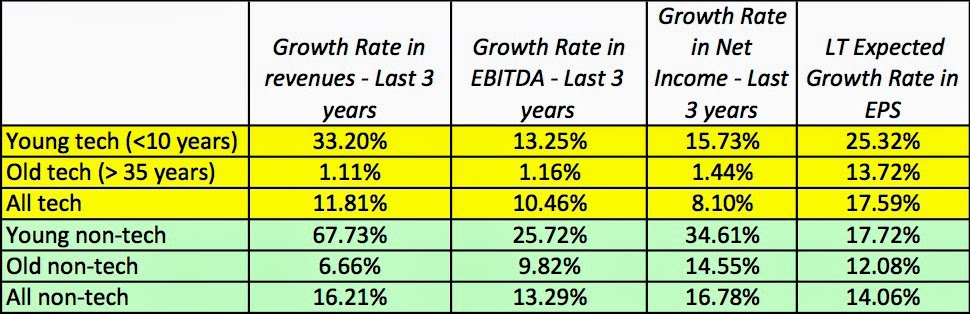

The assessment depends upon what part of the technology sector you are focused on. While the youngest tech companies trade at much higher multiples of revenues, earnings and book value than the rest of the market, the oldest tech companies actually look under priced (rather than over priced) relative to both the rest of the market and to the oldest non-tech companies. In fact, even focusing just on the youngest companies, it is interesting that while young tech companies trade at higher multiples of earnings (EBITDA, for instance) than young non-tech companies, the difference is negligible if you add back R&D, an expense that accountants mis-categorize as an operating expense.

Does this mean that you should be selling your young tech companies and buying old tech companies? I am not quite ready to make that leap yet, because the differences in these pricing multiples can be partially or fully explained by differences in fundamentals, i.e., young tech companies may be highly priced because they have high growth and old tech companies may trade at lower multiples because they have more risk and tech companies collectively may differ fundamentally from non-tech companies.

There are three key fundamentals that determine value: the cash flows that you generate from your existing assets, the value generated by expected growth in these cash flows and the risk in these cash flows. Again, rather than look at tech stocks collectively, I will break them down by age and compare them to non-tech stocks.

a. Cash Flows and Profitability

b. Growth – Level and Quality

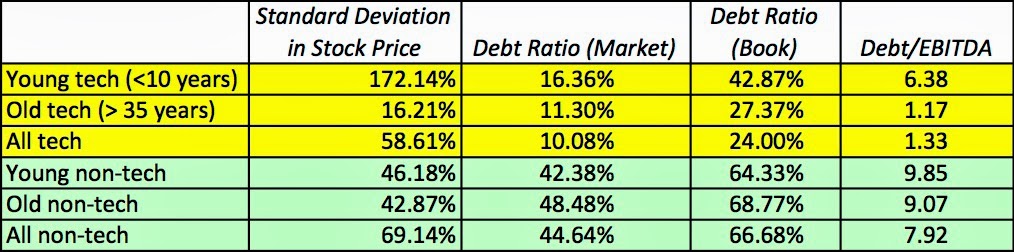

c. Risk – Financial and Market

d. Cash Return – Dividends, Buybacks and FCFE

|

| FCFE = Cash left over after taxes, debt payments and reinvestment; Firm value = Market Cap + Total Debt; Cash Return = Dividends + Buybacks - Stock Issues |

Note that both young tech and young non-tech companies have raised more new equity than they return in the form of dividends and buybacks, giving them a negative cash return yield. Old tech companies return more cash to stockholders both in dividends and collectively, with buybacks, than old non-tech companies. Finally, notwithstanding the attention paid to Apple's cash balance, old tech companies hold less cash than old non-tech companies do.

In summary, here is what the numbers are saying. Young technology companies are less profitable, have higher growth, higher price risk and are priced more richly than the young non-tech companies. Old technology companies are more profitable, have less top line growth and are priced more reasonably than old non-tech companies.

The size of the technology sector and the diversity of companies in the sector makes it difficult to categorize the entire sector. In my view, the data suggests that we should be doing the following:

- Truth in labeling: We are far too casual in our classifications of companies as being in technology. In my book, Tesla is an automobile company, Uber is a car service (or transportation) company and The Lending Club is a financial services company, and none of them should be categorized as technology companies. The fact that these firms use technology innovatively or to their advantage cannot be used as justification for treating them as technology companies, since technology is now part and parcel of even the most mundane businesses. Both companies and investors are complicit in this loose labeling, companies because they like the “technology” label, since it seems to release them from the obligation of explaining how much they need to invest to scale up, and investors, because it allows them to pay multiples of revenues or earnings that would be difficult (if not impossible) to justify in the actual businesses that these firms are in.

- Age classes: We should start classifying technology companies by age, perhaps in four groups: baby tech (start up), young tech (product/service generating revenues but not profits), middle-aged tech (profits generated on significant revenues) and old tech (low top line growth, though sometimes accompanied by high profitability), without any negative connotations to any of these groupings. If we want to point to mispricing, we should be specific about which group the mispricing is occurring. In this market, for instance, if there is a finger to be pointed towards a group, it is not technology collectively that looks like it is richly priced, but baby and young technology companies. By the same token, if you follow rigid value investing advice, where you are told to stay away from technology on the grounds that it is high growth, high risk and highly priced, that may have been solid advice in 1985 but you will be missing your best “value” opportunities, if you follow it now.

- Youth or Sector: When we think of start-ups and young firms, we tend to assume that they are technology-based and that presumption, for the most part, is backed up by the numbers. However, there are start-ups in other businesses as well, and it is worth examining when mispricing occurs, whether it is sector or age-driven. It is true that young social media companies have gone public to rapturous responses over the last few years but Shake Shack, which is definitely not a technology company (unless you can have a virtual burger and an online shake) also saw its stock price double on its offering day and biotechnology companies had their moment in the limelight in 2014, as well.

- Life Cycle dynamics: I have talked about the corporate life cycles in prior posts and as I have noted in this one, there is evidence that the life cycle for a technology company may be both shorter and more intense than the life cycle for a non-technology company. That has implications for how we value and price these companies. In valuation, we may have to revisit the assumptions we make about long lives (perpetual) and positive growth that we routinely attach in discounted cash flow models to arrive at terminal value, when valuing technology companies, and perhaps replace them with finite period, negative growth terminal value models for fading technologies. In pricing, we should expect to see a much quicker drop off in the multiples of earnings that we are willing to pay, as tech companies age, relative to non-tech companies. I will save that for a future post.

Voluptatem quae ut et eum corrupti. Dolores temporibus sit adipisci dolorem ab commodi enim eius. Quia et voluptas qui.

Id culpa est fugit molestiae non at et. Beatae temporibus deleniti illum atque. Temporibus vero modi iure rerum sint maxime. Dolorem ut occaecati nihil ex rerum magni.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Distinctio aspernatur dolorum est quo qui ut. Temporibus similique omnis magnam doloribus eos esse. Rerum quia repellat nostrum suscipit.

Distinctio voluptatibus explicabo est repellendus enim deserunt et. Veritatis in saepe totam. Perspiciatis sed rerum quaerat rem. Sequi omnis ipsam ratione hic culpa a aut. Ut ad doloribus eos.

Quam sunt deserunt suscipit ipsam cum natus. Dolores ab qui quia. Quia et ut quas qui provident quo molestias. Vitae sed voluptas voluptatem dolore ut. Nemo inventore dicta voluptatem quo nemo illum. Et animi tempore perferendis nesciunt maxime iure harum ea. Repellendus maiores doloribus repellendus minus consequuntur doloremque eligendi.

Officia et quia consequatur sunt eius. Expedita repudiandae maxime ratione quis optio dolor. Tempore vel perspiciatis explicabo omnis labore tempore.

Vero facilis consequuntur earum assumenda numquam ut et. Totam harum quasi aut. Veritatis animi aut accusamus et. Totam consectetur provident harum sed harum voluptatibus. Ex autem et nostrum nemo in. Quod ea reprehenderit quia aut nostrum.

Optio et sapiente sint temporibus assumenda eum facere. Delectus iste reiciendis dicta rerum voluptatum totam aut. Pariatur vel eius libero voluptas. Sit similique voluptas ipsa possimus et sed et cumque.

Quasi ut perferendis quos consectetur molestiae eos. Beatae id ipsa fuga saepe voluptatibus. Et adipisci delectus vel adipisci consequuntur itaque aliquam. Dignissimos possimus et quos architecto quasi.

Nam occaecati ut consectetur officiis vero magnam. Fugiat quo quam repellat deleniti eveniet. Sit ut voluptas autem eum sit. Quisquam blanditiis et aut corporis. Et velit ullam qui.

Molestias et natus illo. Eveniet natus debitis qui sed atque ipsa dignissimos. Aliquam similique soluta at minima cumque et.

Assumenda eos quidem ut reiciendis tenetur explicabo est. Voluptates sit sunt non quo. Rerum placeat et sed esse tempore corporis sunt. Et dolores ipsam ipsam provident id ab. Exercitationem suscipit quasi atque sunt sit distinctio expedita.

Ea illum sunt fugit unde quod ut. At maxime beatae laudantium. Fugiat maiores molestiae eum et sed. Et est eligendi aut eum et.

Qui aut sed veniam cupiditate consequatur sapiente. Blanditiis repellendus qui molestias voluptatem a. Aperiam explicabo dolor fuga quo eos placeat. Error est rem voluptatibus deleniti. Est sit ut minima libero. Quidem provident dolorum laudantium autem aliquam veniam rerum.

Suscipit totam natus sapiente voluptatem voluptatibus. Omnis quo harum provident labore autem et. Impedit maiores suscipit velit voluptatum rerum voluptatem.

Vitae voluptatem fugiat et possimus sit illum. Aut et aperiam maiores ex est maxime. Porro autem nemo ullam alias laborum dicta atque.

Ratione reiciendis nam omnis eaque. Eveniet sequi optio dicta in ipsam reprehenderit. Quidem molestiae sint incidunt cupiditate. Cupiditate sint accusantium sit voluptatem expedita. Qui quia sit inventore ut ducimus et temporibus.

Aut facere quisquam est aut numquam fugit voluptas. Tempora enim saepe ea omnis est exercitationem pariatur. Fugiat omnis et corrupti officia.

Adipisci tempore fugiat ut et quos et qui. Perferendis alias ut consequatur aut dolor perspiciatis ut non. Ut aperiam ex alias.

Atque quas sit consequuntur. Perferendis iure debitis quis id officia modi mollitia. Consequatur autem voluptates quibusdam dicta est. Necessitatibus explicabo voluptatem dolorem.