Stock Based Compensation

A non-cash remuneration that is provided to a company’s employees

Stock-based compensation, also known as share-based compensation, is a type of non-cash remuneration that is provided to a company’s employees which gives them a chance to reap the benefits that result from the growth of the company.

A well-structured stock-based compensation arrangement can be one of the easiest ways to align the interests of the employees with those of the owners of an organization without touching the company’s bank account.

It can encourage employee retention and loyalty, especially in the presence of vesting clauses. While it is generally seen as a way to supplement cash-based pay, it can also be accompanied by lower cash salaries.

However, before freely offering stock-based remuneration to employees, companies must consider an entire host of factors such as tax law, corporate law, securities law, accounting considerations, as well as its impact on investors.

The most common stock-based remuneration schemes include stock options, performance shares, and restricted stock. All of these structures allow employees to enjoy ownership-related benefits in their company.

- Stock-based compensation aligns employee and owner interests without using cash.

- Common provisions in stock compensation plans include vesting and change in control clauses.

- Stock-based compensation promotes retention, aligns interests, and preserves cash for companies.

- Disadvantages include dilution for shareholders and potential loss during stock price decline.

- Types of stock-based compensation include restricted stock, performance shares, stock options, SAR, and phantom stock.

Stock-based compensation: Common provisions

The following provisions are commonly part of stock compensation plan agreements.

1. Vesting

Before handing out stock incentives, companies must consider vesting plans. Stock compensation may vest based on time, predetermined performance metrics, or based on a mix of the two. Vesting schedules normally span between three and five years.

2. Change in control

Amidst dynamic business environments, it is necessary to have some terms in such compensation agreements that allow for flexibility in the event of a change in control of the company (generally occurring as part of mergers and acquisitions or takeovers).

This flexibility may allow the company to accelerate the vesting schedule, to convert the company’s stock awards into that of the acquirer’s stock, or to even terminate the compensation program altogether upon the occurrence of such an event.

Accelerating vesting schedules leads to a decrease in the value of the acquirer’s investment. Thus, when exercising flexibility, the board needs to maintain an equilibrium between offering incentives to the workforce and issues pertaining to investor relations.

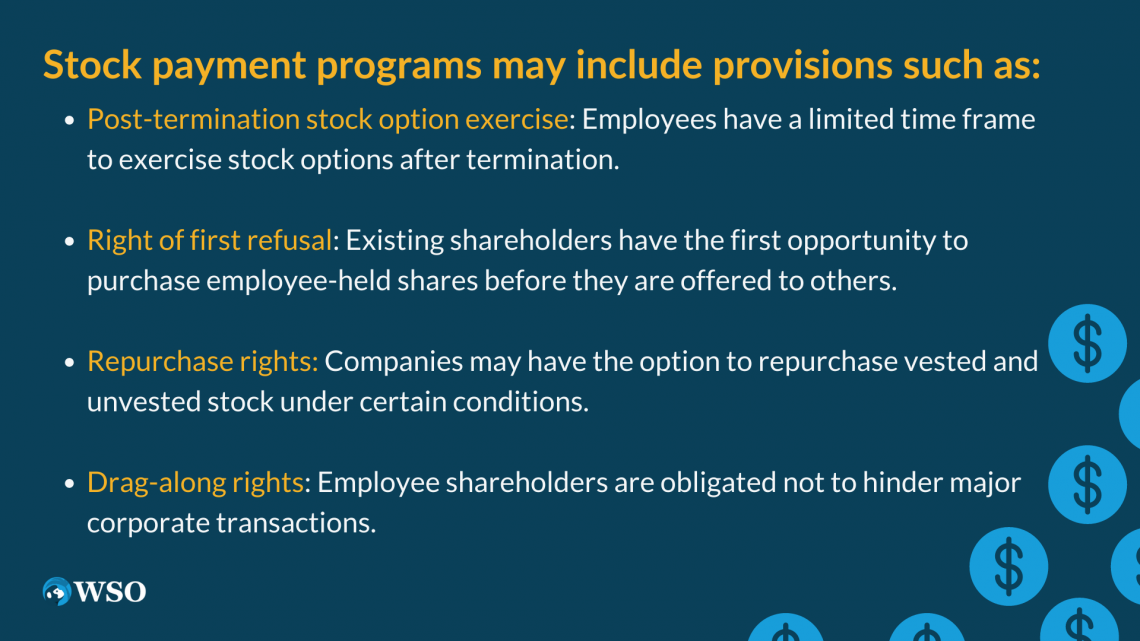

Additional Provisions in Stock Payment Programs

Stock payment programs may also have certain added provisions to protect the interests of the employers.

1. Exercising stock options post-termination

A limited time frame is allowed for the employees to exercise their stock options post-termination when the termination is due to death or disability or is voluntary or without cause.

The window may be up to 3 months if the termination is voluntary or without cause, and up to 12 months if it is due to death or disability. On the contrary, stock options generally lapse in case of termination of employment with cause. In the case of restricted stock, the vesting ceases and shares are forfeited or repurchased.

2. Right of first refusal

Shareholders of private companies prefer to have shares held among a few known and connected persons. Hence, private companies generally have provisions in place to prevent loss of control.

These provisions may require employees to first offer the shares for sale to existing shareholders, giving them the right of first refusal before offering them to unconnected parties.

3. Repurchase

Private companies prefer to have terms for repurchase rights for both vested and unvested stock. In the case of vested stock post-termination for cause and unvested stock, the terms may dictate repurchase at cost or at the lower of cost and fair market value.

On the other hand, in the case of vested stock, companies may retain repurchase rights under all circumstances until the company goes public or under fewer circumstances (such as voluntary termination or bankruptcy). Repurchase may then be at fair market value.

4. Drag-along rights

These provisions ensure that employee shareholders are contractually obligated to not interfere with major corporate transactions, such as mergers and acquisitions. This keeps employee shareholders from hindering corporate actions.

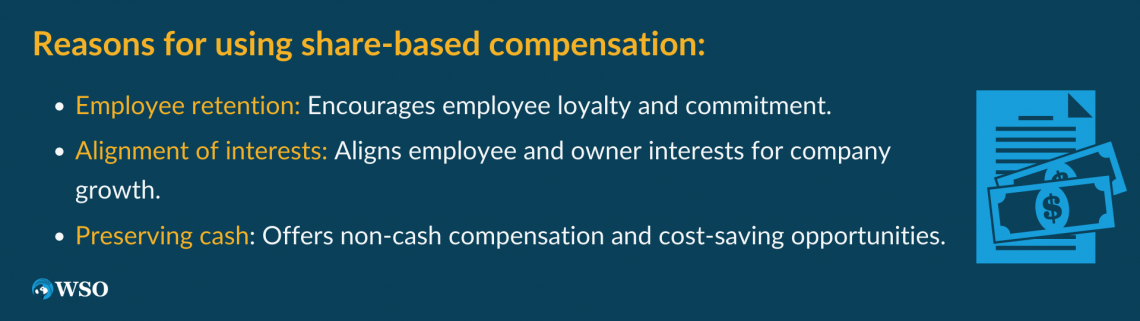

Why is share-based compensation used?

There are several good reasons why companies might prefer to grant a portion of the equity to their employees.

1. Employee retention

Share-based compensation structures encourage higher employee retention by increasing their personal financial interest in the growth of the company, especially when implemented with vesting requirements.

2. Aligning interests

It aligns the interests of the employees and the owners. When employees are granted stock-based pay, they gain a financial interest in the company with unlimited upside, unlike their salaries which are fixed. It is then in the best interest of the employees as well as the shareholders that the company grows, leading to an increase in the value of its shares.

3. Preserving cash

Startup and early-stage companies may lack the resources to pay competitive salaries to attract good talent. For such companies, non-cash compensation is the best option since it does not require companies to directly spend financial resources, but only to share some of the company’s returns with the employees in the future.

Not only that, companies can often bargain to pay cash salaries lower than the market rates when offering equity to employees. Even though it is well known that companies in the start-up stage grant equity more liberally, mature companies don’t shy away a lot from awarding it either.

Disadvantages of stock-based compensation

Given the advantages, it certainly can be tempting to pay employees using equity instead of cash. However, due to the disadvantages, this mode of payment is used in moderation at best.

1. Dilution

An increase in the number of outstanding shares does not bode well with investors. More outstanding shares mean that the investors would need to give up a part of their share of the earnings and control of the company.

For instance, let’s assume that company ABC is expected to earn $100 in an accounting period, and there are 20 outstanding shares before equity-based pay is granted to employees. The earnings per share (EPS) would be $5.

The company then grants 5 equity shares to its employees. Now, the EPS would be $4. The EPS for the shareholders reduces from $5 to $4 - a 20% decrease. Further, they now own only 80% of the company (20 / 25 shares) compared to an earlier 100%, which reduces their claim on all future earnings.

Hence, investors may find it acceptable to issue shares only if they are issued with differential voting rights, which at least prevents dilution of control.

2. Falling stock prices

If a company sees a slump in its stock price, its share-based compensation may not be perceived as valuable compared to before the slump. Employees might prefer to earn a slightly higher cash salary without share-based compensation than to earn a lower cash salary with such compensation in times of falling stock prices.

Different Types of stock-based compensation

There are different forms of stock compensation, each granting ownership benefits differently. While some stocks offer ownership outright, others are subject to fulfillment of some conditions. Some provide preferential tax benefits to certain categories of receivers but not to others.

1. Restricted stock

This is stock issued to employees today but is subject to future vesting requirements. It can be granted to all employees, consultants, and non-employee directors.

Restricted stock is considered to be outstanding since the time of issue, which means that the stock recipient may exercise voting rights and receive dividends.

Vesting requirements of the stock may be framed with the aim of retaining good talent and/or achieving certain performance metrics. In the event of non-fulfillment of vesting conditions, the stock shall be forfeited and the grantee shall cease to participate in the ownership of the company.

Restricted stock may be granted outright without any payment, or employees may be required to purchase the stock at either its par value or at or below its fair market value.

2. Performance shares

These shares are granted if some prespecified metrics are achieved. The targets could be earnings-related, profitability-related, returns-related (return on investment, return on assets, etc.), and/or any other internal measures of the company’s performance.

Performance is measured over years for this purpose. This helps the company to assess its long-term performance and to avoid basing stock compensation on temporary fluctuations in the numbers.

Performance stocks are different from restricted stocks due to the fact that in the latter, the vesting requirements are fulfilled after the stock is issued. Hence, the benefits of restricted stock can be enjoyed even before meeting the vesting conditions.

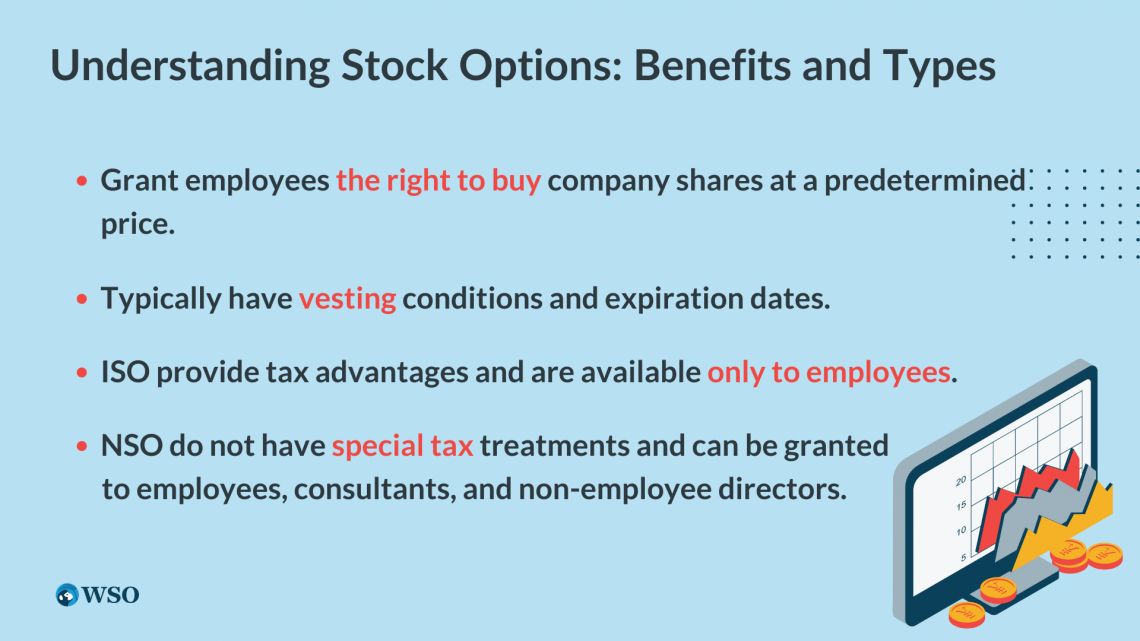

3. Stock options

Stock options offer employees the right to buy shares in the company at a pre-specified price (the exercise price). More often than not, they are offered with time-based and/or performance-based vesting conditions.

Upon vesting, the option holder gains control over the option. The holder may then exercise, sell or transfer the rights to buy the company’s shares at the exercise price. Stock options also carry an expiration.

Especially in early-stage companies, stock options align the interests of the employees with those of the shareholders to a significant extent by allowing employees to participate in the upside, thereby incentivizing them to propel the company’s growth.

- Incentive stock options (ISO): These are only available to employees. They cannot be offered to consultants or directors who are not employees of the company. Being the special creations of the tax code, they provide special tax advantages upon satisfaction of certain conditions.

- Non-qualified stock options (NSO): These do not provide special tax treatments to the option-holders. Like restricted stock, they may be granted to any employees, consultant, or non-employee director of the company.

Stock-linked cash compensation

Companies may allow employees to participate in the upside that ownership offers without actually granting equity shares, which result in permanent dilution in the earnings or control from the shareholders’ perspective.

1. Stock appreciation rights (SAR)

Under SAR compensation agreements, employees receive cash equal to the company’s stock price appreciation over a pre-specified period. Like stock options, SAR are beneficial when the stock price rises.

However, unlike stock options, employees are not required to pay any amount (the exercise price) upfront to acquire the shares. Thus, they can be particularly lucrative when the company is seen to be growing rapidly.

2. Phantom stock

Phantom stock plans are also known as synthetic equity or shadow stock. These offer a greater degree of flexibility, given that there are no restrictions regarding their use.

They bestow employees with the benefits of owning actual stock while not actually owning it. Employees receive mock stocks under this plan. Shadow stocks are not real but they do track the price movements of the company’s stock and, despite being hypothetical, may still distribute dividends.

They are often offered to the senior management. They make it easy to ensure that the equity of the company is not diluted.

At the end of a predetermined period, the company may distribute the benefits under the plan in cash. The benefits depend on the type of phantom plan.

- Appreciation-only plans: These plans are similar to stock appreciation rights. Employees under this plan are eligible to receive a sum equivalent to the appreciation in the stock price. They do not include the value of the underlying stock.

- Full value plans: At the end of a predetermined period, these plans not only pay the stock appreciation but also the value of the underlying stock.

The significant point of difference between SAR plans and phantom stock plans is that the latter normally accounts for stock splits and dividends.

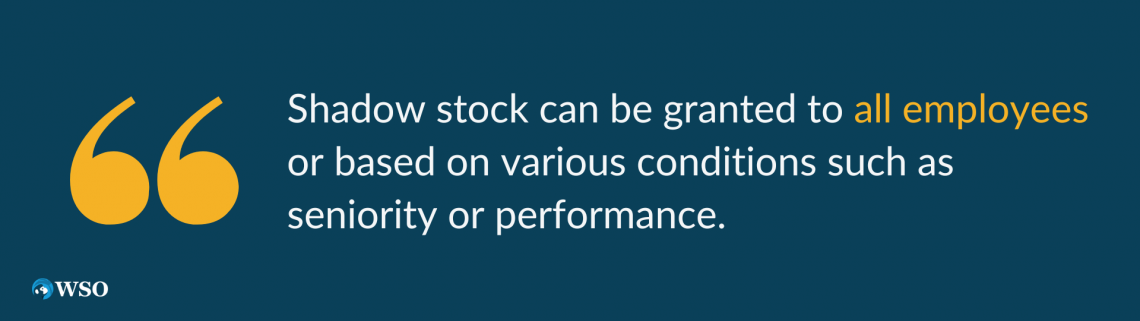

Shadow stock can be granted to every employee, or be granted based on a broad spectrum of conditions relating to seniority, performance, or other factors.

Moreover, they also allow companies to offer equity-based incentives to employees when there are restrictions in place, for example, relating to the number of shareholders. These plans can offer great flexibility in such use cases.

Impact of Stock-Based Compensation on financial statements

The impact on financial statements is primarily reflected in the following:

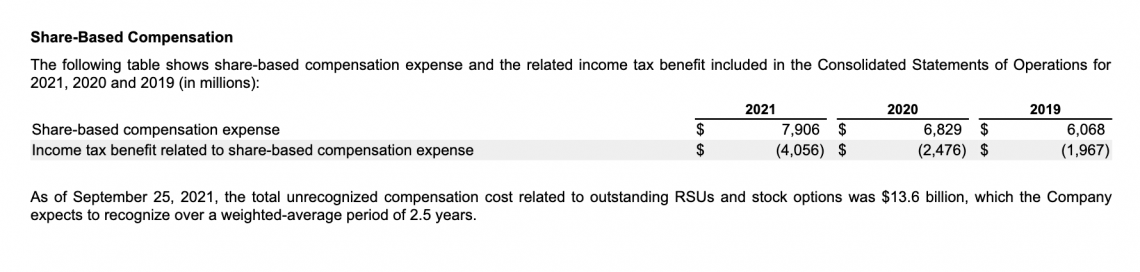

Decrease in earnings: The stock compensation expense is recorded in the income statement, which lowers net income. In the case of time-based vesting requirements, the expense may be recorded on a straight-line basis over the vesting period.

For a real-life example, please see the below segment from Apple Inc.’s 10-K filing dated October 2021.

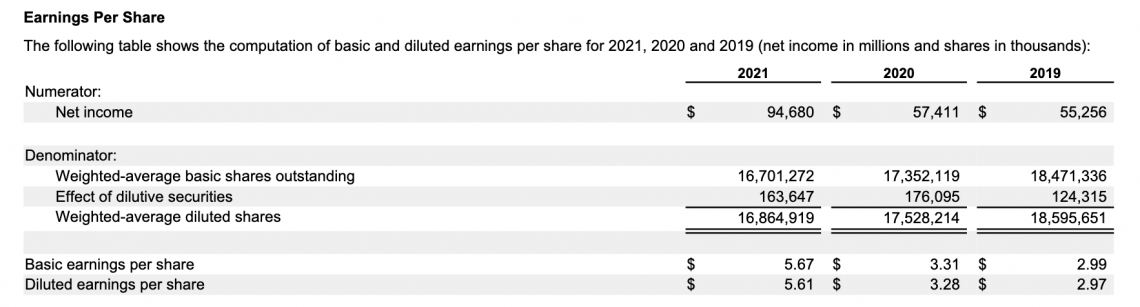

Decrease in earnings per share (EPS): Issuing restricted stock increases the number of outstanding shares. With a larger denominator base and lower earnings, basic EPS falls.

Diluted EPS may be even lower based on other dilutive securities and other stock compensation plans in place, like stock options. From Apple’s 10-K filings, please note the effect of dilutive securities (including stock compensation awarded) on EPS. It increases the weighted-average shares in the denominator in the EPS formula.

When a company issues stock payments, the paid-up capital on its balance sheet increases owing to an increase in the number of outstanding shares. The effect of stock compensation expense over the years shows in the form of reduced shareholders’ equity due to reduced net earnings.

In the case of stock-linked cash payments, the company is obligated to make cash payments. There is a cash outflow, which offsets the stock compensation expense, which further leads to reduced shareholders’ equity.

Stock-based compensation has no effect on the cash flow statement of the company. This is because there are no cash inflows or outflows in this kind of transaction. The stock compensation expense is, in fact added back to the net income while calculating cash flow from operating activities, since it is a non-cash expense, much like depreciation.

Contrarily, when companies compensate their employees in cash, based on an increase in share price, there is an obvious cash outflow. This cash outflow will reflect in the cash flow statement, thus reducing “cash flows from operating activities”.

Share-based compensation: Considerations while valuing companies

Let’s suppose that a business pays its employees only by way of share-based compensation instead of cash salaries. Assuming that the company grants a 5% equity stake to employees every year, it does so by taking away the 5% from existing shareholders.

Every subsequent year, the shareholders own a smaller share of the company, leaving them entitled to lesser profits.

When investors expect companies to grant stock compensations in the future, they must adjust their valuation of the company’s equity by adjusting future earnings downwards during discounted cash flow analysis.

If the company has options that have not yet expired or vested, their value should be deducted from the value of the total equity to arrive at the true post-dilution value of the common stock.

Investors should also be wary of per-share numbers reported by researchers and analysts as they can be pre-dilution or post-dilution depending on the share base considered in the denominator while calculating the same.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?