Evaluating the Disconnect: Institutional Sentiment vs. C-Suite Capital Allocation in Discount Retail

For those covering the consumer staples sector, the current macroeconomic environment presents a modeling nightmare. Sell-side analysts are constantly adjusting their terminal growth rates based on lagging CPI data and aggregated credit card spending. However, these top-down models frequently fail to capture the ground-level reality of opportunistic retail models. While the broader institutional sentiment remains cautious on retail equities due to margin compression fears, a starkly different narrative is unfolding within the boardroom. Recent Form 4 filings show a noticeable increase in executive accumulation across the defensive consumer sector, contrasting with broader institutional outflows. This divergence between sell-side hesitation and internal corporate confidence offers a compelling data point for fundamental analysis.

The Mechanics of Opportunistic Sourcing and Information Asymmetry

Unlike traditional supermarket chains that rely on predictable, low-margin distribution contracts, the opportunistic sourcing model thrives on supply chain inefficiencies. Companies operating in this niche acquire excess inventory, packaging transitions, and order cancellations at steep discounts. Because this inventory pipeline is highly volatile and opaque to the public market, the management team possesses a significant information advantage over external analysts. When executives running this specific business model choose to deploy their personal capital into the company's equity, it generally indicates that their current procurement pipeline is yielding higher-than-expected gross margins. They are effectively front-running the delayed visibility of the institutional market.

💼 CAPITAL ALLOCATION: THE FORM 4 DIVERGENCE 💼

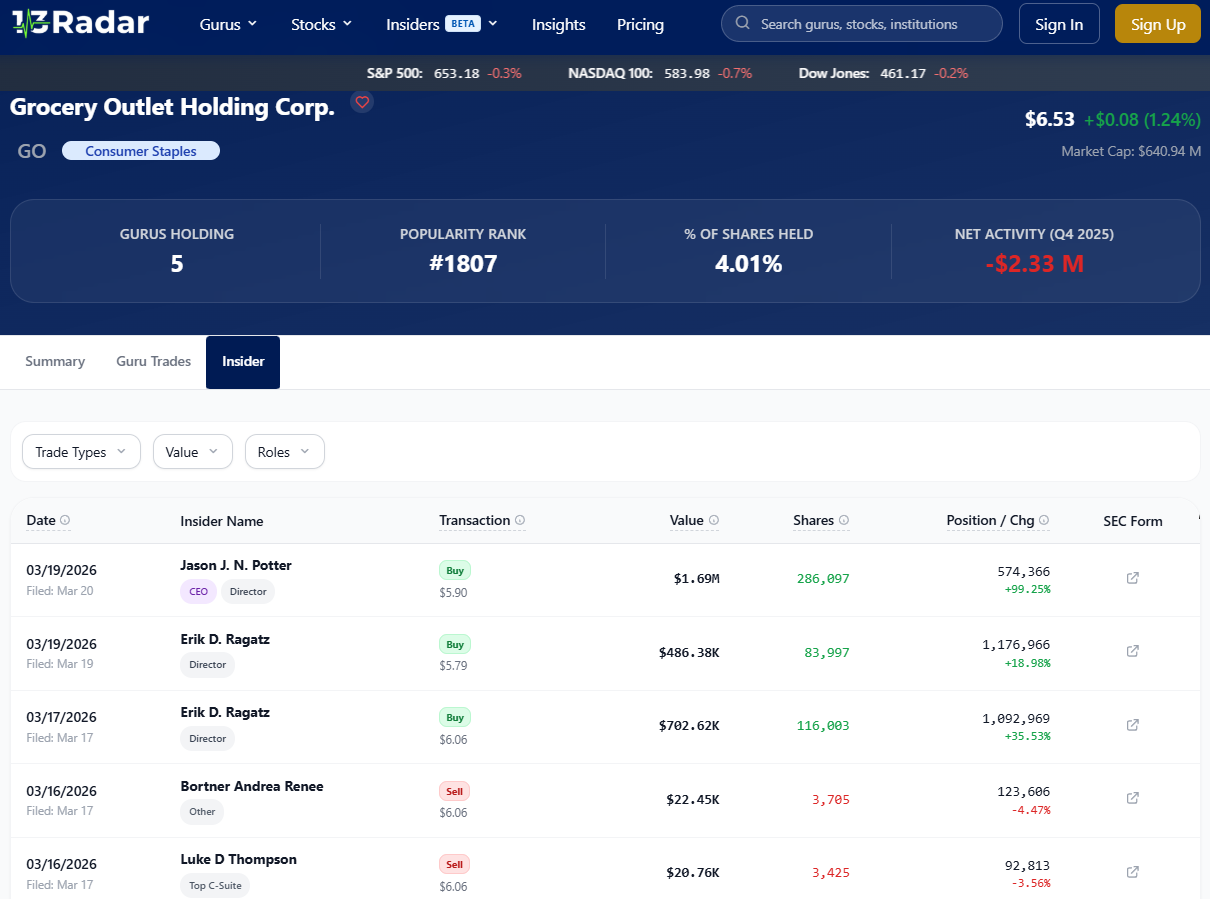

Analyzing the exact nature of these transactions is critical for understanding the underlying corporate conviction. A routine option exercise holds little analytical weight, but pure open-market purchases reflect a deliberate asset allocation decision. For professionals evaluating grocery outlet insider buying, the recent multi-million dollar open-market acquisitions by top-tier management serve as a significant fundamental anchor. When a Chief Executive Officer allocates a substantial portion of their liquid net worth into the company's stock during a period of broader sector volatility, it establishes a verifiable benchmark of internal confidence. It suggests that the internal cash flow projections and store-level unit economics are robust enough to withstand current macroeconomic headwinds.

Forward-Looking Implications for Margin Expansion

In an efficient market, large-scale insider accumulation should theoretically reprice the asset immediately. However, the complexity of the discount retail supply chain often causes a delayed reaction from fundamental funds. By the time the expanded gross margins are officially reported in the quarterly earnings, the risk-reward ratio has typically already shifted. Observing these Form 4 filings provides a real-time proxy for the company's operational health. Rather than relying solely on historical earnings data, observing how the architects of the business allocate their personal wealth offers a more immediate reflection of where the company's fundamental valuation is truly heading, providing a distinct edge in assessing true enterprise value.

Cupiditate blanditiis occaecati voluptatum. Vel ut velit vel. Dolorem deserunt ut adipisci fugiat amet est velit. Excepturi similique magnam alias eligendi unde. Nisi accusamus in reiciendis omnis voluptatibus. Quos rerum alias quas est aut accusantium. Asperiores dicta sint veniam quod molestiae incidunt.

Libero dolores animi nostrum ducimus ipsam tempora molestiae. Aut omnis ut officia sapiente. Vitae non ut quia.

Laboriosam placeat asperiores et eius. Qui nobis officia et nulla ut inventore qui. Nisi aliquam deserunt debitis.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...