Why does consensus matter?

Have seen a bunch of posts recently on consensus and being contrarian etc. Probably from people like me in private investing looking to switch to a pod.

But really why does it matter? It feels like there are two things that matter: the market’s view (current price) and your view (which will be different than price if you’re pitching something). Seeing sell side models and commentary can help pull out what the current market price is implying in terms of KPIs and financials but I’m finding it hard to understand what “role” sell-side consensus plays on thinking about valuation.

Is it all about earnings? That’s the one use case I could take away. And then deciding if what consensus earnings estimates are (quarter, yearly) and making my own assumption on if the company will beat or miss that. That would then drive price and makes sense to have a view on.

Consensus matters because it serves as a benchmark for understanding the market's expectations and helps you identify where your differentiated view can create alpha. Based on the most helpful WSO content, here’s why consensus is critical:

Market Expectations vs. Your View: Consensus, particularly sell-side consensus, reflects the aggregated expectations of analysts regarding a company's performance (e.g., earnings, revenue, KPIs). While the sell-side doesn't allocate capital, their estimates influence the broader market sentiment. If your view diverges from consensus and you’re correct, that’s where the opportunity lies.

Role in Valuation: Sell-side consensus helps you back into what the market is pricing in. For example, using a DCF model, you can approximate the range of outcomes embedded in the current stock price. This allows you to assess whether the market is underestimating or overestimating certain factors, such as growth potential or risks.

Earnings as a Catalyst: As you mentioned, earnings are a key use case. Stocks often trade on EPS momentum—whether a company beats or misses consensus estimates can drive significant price movements. By forming your own view on whether a company will outperform or underperform relative to consensus, you can position yourself ahead of these moves.

Buy-Side vs. Sell-Side Dynamics: The buy-side often has a different perspective than the sell-side. While the sell-side may be cautious about upsetting management or overly optimistic, the buy-side focuses on making money and may price in risks or opportunities earlier. Understanding this dynamic helps you gauge where the real opportunities lie.

Differentiated View: The value of consensus lies in giving you a baseline to challenge. If you can identify areas where consensus is wrong—whether due to flawed assumptions, overlooked catalysts, or mispriced risks—you can develop a contrarian thesis that generates returns.

In summary, consensus is not just about earnings but about understanding the broader market narrative and finding gaps where your insights can add value. It’s a tool to frame your analysis and identify mispricings, especially in a pod environment where differentiated views are critical.

Sources: Understanding Concensus & Differentiated View, Thinking Like an Investor, Q&A: HF Analyst, Observations of an Equity Research Associate, https://www.wallstreetoasis.com/forum/private-equity/a-guide-on-how-to-navigate-on-cycle-pe-recruiting?customgpt=1

Consensus is in the name - it’s what the majority of people think will happen. This includes earnings estimates and other expectations. You can come up with your own view but if you don’t know if it differs with other people then is it differentiated? Comparing to consensus helps you see if you’ve got an edge or if the market is already pricing it appropriately. There’s been plenty of times where I thought I had something on a new name only to compare my estimates and end up largely at consensus. I’ve also had the inverse - thought I had a consensus view only to discover that the street wasn’t modeling correctly.

The real trick is to figure out buyside consensus. Sellside consensus is helpful but if all the pod bros all have the same non-sell side consensus view then you’d still be piling into a consensus trade. It’s not always the easiest to figure out but understanding buyside consensus is where you can generate real alpha.

Thanks, super helpful. Makes sense that consensus is then somewhat priced in.

Why does it matter if you agree with buyside consensus if it’s not priced in? Couldn’t a couple pods or funds generate alpha in the same trade? Or will that dilute your trade if the other pod bros are piling in too

There can be multiple winners on a stock. It’s not whether 1 or 2 people agree with you, it’s getting a sense of the spread of outcomes different players are baking in to the stock

If it’s truly not priced in then sure you can all make money but there’s a reason that there’s “hedge fund hotels”. Some times the risk/reward makes sense to hide out there long or short (there’s specific stocks in my coverage that everyone perpetually loves/hates and you just kind of have to be there because there’s a reason it basically always works) but the real money is generally made when you can figure out when the tide is coming in/out on those names. And understanding where you differ from the rest of the buyside should give you the path to monetize.

It's a good question. I can answer from the perspective of a market neutral l/s analyst. Consensus is basically the metric everyone models around because it's viewed as the barometer for alpha generation (if beat or miss). Conceptually, it's what's viewed to be priced in but not always the case. I think the way people go about building a variant view from consensus today is WAY more robust than I've ever seen and it's partly because all the tools we have access to. I started a thread on this actually that listed some tools we use to find holes in consensus. Try any of these:

www.tegus.com,

www.variantmkt.com,

www.bamsec.com, visiblealpha.com, thirdbridge.com.

Here's a thread that may help youhttps://www.wallstreetoasis.com/forum/hedge-fund/key-tools-for-hf-analy…

Consensus matters because IR communicates to analyst teams and they put into model

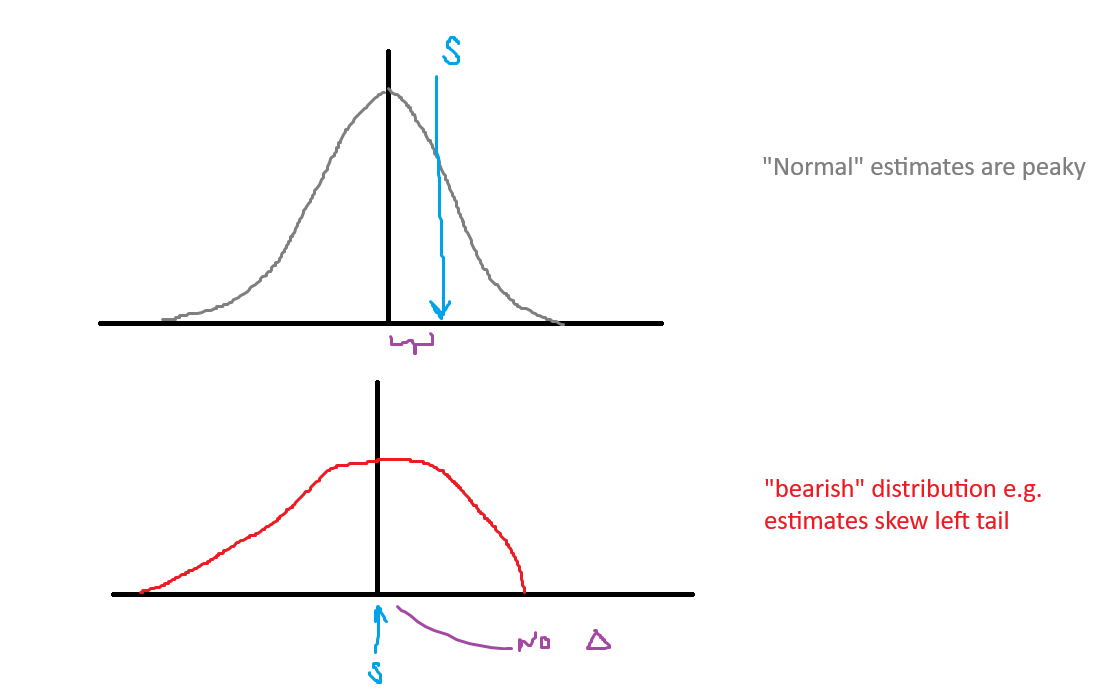

You need to have a benchmark of estimates in order to determine if an opportunity should pay more than, less than, or equal to beta.

In classical thinking, a stock should move, ceterus paribus, by the surprise to estimates:

In the above, the bearish scenario prints in-line (s= surprise), so the stock price "doesn't move", while in the "normal" setup, there is a positive surprise to estimates, which would move the stock by the surprise. This is a super simplistic example.

Consequatur qui aliquid odit perspiciatis sit assumenda inventore. Dolor dolor quibusdam dolor fugiat illo dolor. Ut eaque nisi dolorem ad. Velit voluptatum earum nihil consequatur deserunt numquam eos. Ea non officiis porro omnis omnis ut voluptatem. Non aut rem necessitatibus illo sit. Vero dolorem reprehenderit laborum eos nisi quia occaecati molestias.

Dolores molestias omnis aut qui. Vitae et omnis enim iusto quisquam hic. Reiciendis consequatur vel sint numquam qui. Nesciunt dolor quasi quia vel ab aut.

Ex rerum laboriosam sint cumque. Harum necessitatibus nam maxime aut. Quisquam non molestiae impedit est dolores quas consequatur. Ratione cupiditate ipsam iure beatae quis voluptatem aut.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...