Berkshire’s Liquidity Preference: A Macro Signal or Just Multiple Compression?

The accumulation of over $325 billion in cash equivalents on Berkshire Hathaway’s balance sheet has generated significant discourse regarding cycle maturity. While retail narratives focus on "market timing," the institutional view suggests this is fundamentally a function of Hurdle Rates and Opportunity Cost relative to the Risk-Free Rate.

Buffett has effectively converted a significant portion of the portfolio's equity beta into short-duration Treasuries. This rotation implies that, at current valuations, the Equity Risk Premium (ERP) offered by large-cap equities—specifically in the tech hardware and banking sectors—no longer justifies the capital charge compared to a guaranteed 4-5% yield.

1. The Decomposition of the "Sell" Decision

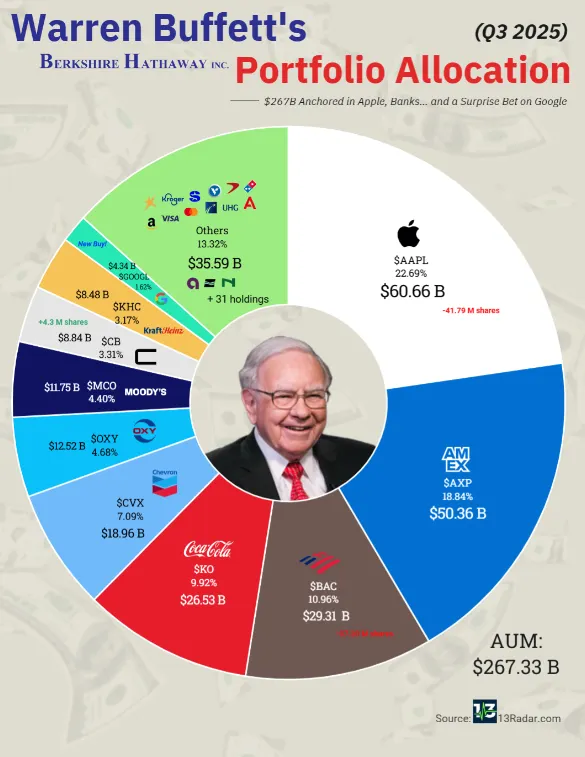

The divestment from long-standing positions like Apple (AAPL) and Bank of America (BAC) should be analyzed through the lens of Capital Allocation efficiency rather than purely operational concerns.

When the P/E multiples of mature tech and financials expand beyond their historical averages without a commensurate increase in growth velocity, the forward returns diminish. By liquidating these positions, Berkshire is effectively harvesting the valuation anomaly and retreating to a neutral duration stance, preserving the optionality to deploy capital when spreads widen.

📊 Institutional Analysis: The "Moat" vs. The "Trade"

A bifurcation is evident in the portfolio's retention strategy. The decision to retain American Express (AXP) and Coca-Cola (KO) versus the liquidation of others highlights the distinction between "Compounders" and "Cyclicals" in a high-rate regime:

- Pricing Power Elasticity: AXP and KO demonstrate the ability to pass through inflation costs without volume degradation, sustaining high Return on Invested Capital (ROIC).

- Capex Intensity: The retained holdings require minimal incremental capital to maintain market share, unlike the tech sector which faces an AI-driven Capex super-cycle.

- Yield Arb: The effective dividend yield on cost for legacy positions far exceeds the current risk-free rate, creating a "negative carry" if sold (tax implications notwithstanding).

3. Cash as a Call Option on Distress

The massive cash pile should not be viewed as idle capital, but rather as an out-of-the-money Call Option on Market Dislocation. In a credit contraction or liquidity event, Berkshire acts as a primary liquidity provider (e.g., the 2008 Goldman Sachs warrant deal).

For analysts modeling Berkshire's book value or tracking the shift in sector weightings, the historical filing data offers a precedent for this defensive posturing. The current composition of the warren buffett stock portfolio suggests a strategic pivot: prioritizing the return of capital over the return on capital until valuations revert to historical means.

Perferendis vero qui ipsum ipsam voluptatem mollitia voluptas. Non temporibus quod id qui vero earum. Aut modi eaque ea ullam. Eaque aliquid quos facilis sit aut adipisci quibusdam excepturi.

Debitis pariatur aut occaecati deserunt rerum voluptate facilis. Aspernatur similique illum ut quasi amet libero. Omnis cum aliquid aliquam nihil ipsum quia nihil.

Nulla fugiat autem ab voluptate. Illum necessitatibus perspiciatis qui aut minima. Est expedita quam quod. Qui aspernatur in sed quis voluptatem. Rerum voluptatem laborum consequatur reiciendis autem nam autem.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...