The Ultimate Tell: Why C-Suite Accumulation Trumps AI Hype in the Power Sector

The macroeconomic narrative surrounding the energy sector has been entirely hijacked by the artificial intelligence revolution. The street has aggressively allocated capital into utility equities, operating under the assumption that the exponential power demands of hyperscale data centers guarantee decades of frictionless revenue growth. However, while retail participants and passive indices blindly trust optimistic sell-side upgrades, institutional money managers demand empirical proof. In a sector currently experiencing extreme volatility and structural revaluation, the absolute most critical metric isn't a polished corporate press release—it is the specific, documented willingness of top executives to aggressively purchase their own stock on the open market.

Desk Note: The Information Asymmetry of Open-Market Actions

Evaluating the tape requires an understanding of the psychological asymmetry behind regulatory disclosures.

Executives frequently liquidate company equity for a myriad of mundane reasons: covering tax liabilities, funding real estate purchases, or simply diversifying a heavily concentrated portfolio. Corporate officers, however, only execute open-market purchases with their personal, post-tax wealth for one undeniable reason: they possess internal, asymmetrical data proving the stock is drastically undervalued. An executive buying the dip is the ultimate destruction of a bearish thesis, serving as a pure conviction signal that internal cash flow models are vastly outperforming public sentiment.

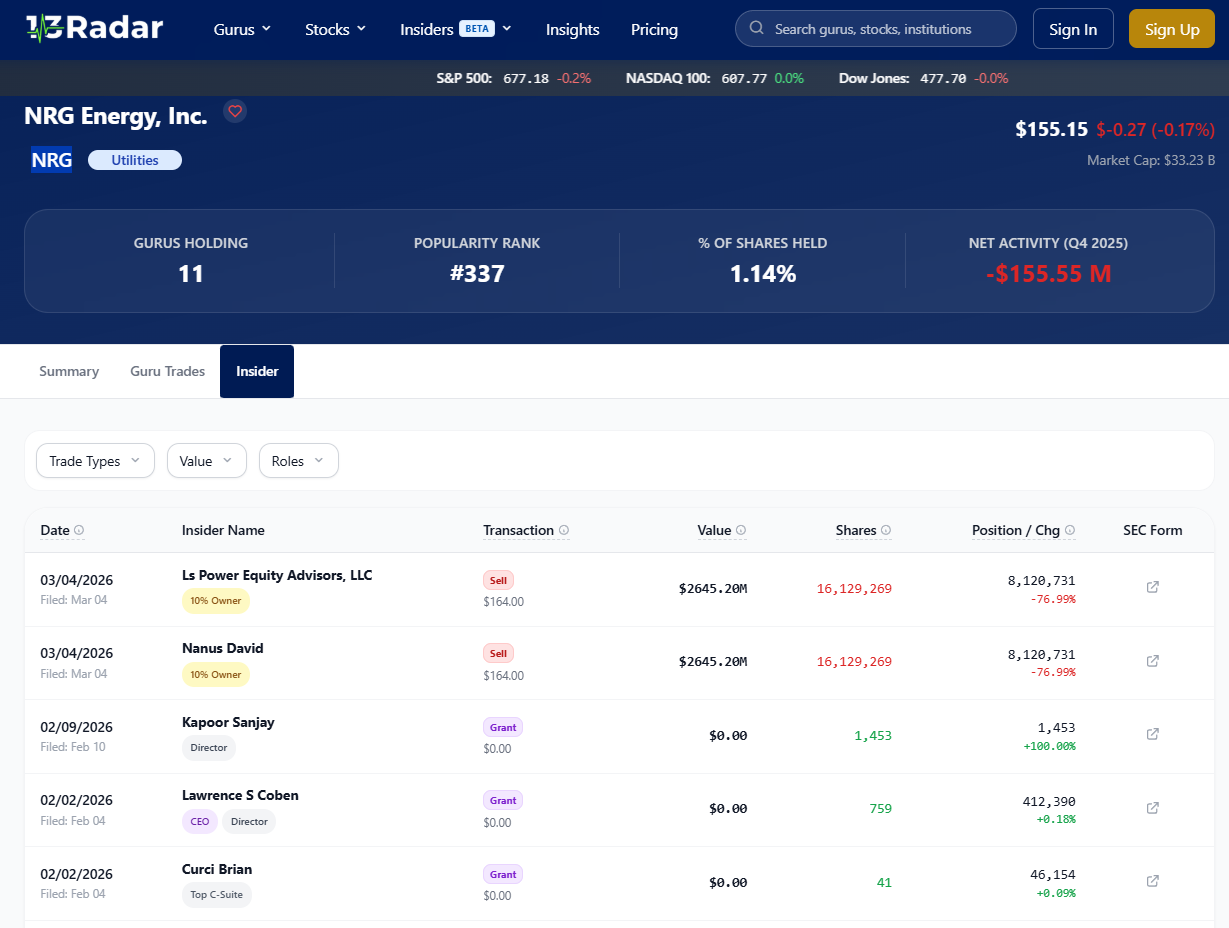

Analyzing the Macro Form 4 Environment

If the fundamental reality of the AI energy boom perfectly matched the media's euphoric projections, the transaction tape would theoretically be flooded with corporate accumulation. Instead, a sobering divergence is currently unfolding across the broader market. Recent Form 4 filings show a noticeable dominance of executive sales over open-market purchases across major utility and power generation companies. This widespread hesitancy from the C-suite forces quantitative funds to remain highly defensive. When the very individuals negotiating multi-billion-dollar power purchase agreements are unwilling to increase their personal stake at current multiples, it definitively signals that grid expansion bottlenecks, supply chain constraints, and regulatory costs are materially suppressing near-term margin expansion.

The Algorithmic Trigger for Capital Deployment

Sophisticated systematic funds do not rely on retail sentiment or lagging earnings whispers to price their entry points; they wait for the architects of the company to confidently draw a line in the sand. A major structural correction is typically only arrested when internal stakeholders decide the risk-to-reward ratio is far too lucrative to ignore. For trading desks modeling the eventual recovery of top-tier grid operators, the sudden appearance of verified NRG insider buying would act as a massive, immediate catalyst. If a Chief Financial Officer or Board Director steps into a volatile chart with a multi-million-dollar acquisition, it instantly telegraphs to the street that internal valuations are highly disconnected from the public sell-off. Ultimately, observing this specific type of accumulation signal remains one of the few mathematically sound ways to confirm whether the AI energy thesis is genuinely translating into tangible corporate value.

Eos eos magni consequatur et est magnam exercitationem rerum. Tempora non itaque veritatis itaque consequatur cumque. Accusantium modi culpa et autem.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...