Thesis Discussion: Sector Rotation from Semi Hardware to "TechBio" & Application Layer

The consensus trade over the last 24 months has explicitly favored the "Picks and Shovels" of AI—specifically Data Center infrastructure and GPU fabrication. However, current valuation multiples in the semiconductor space are beginning to imply a perpetual exponential growth rate that historical Capex cycles rarely support. From a risk/reward perspective, the "Hardware Trade" appears increasingly overcrowded.

The emerging debate on the street is centered on a capital rotation into sectors that have been compressed by rate expectations but stand to benefit from the actual application of these new hardware capabilities. Specifically, the intersection of AI and Biology ("TechBio") and the margin-expansion story in SaaS.

The "TechBio" Arbitrage: Pricing R&D Efficiency

The market seems to be pricing biotech largely on legacy drug discovery timelines, potentially underestimating the deflationary impact of LLMs on the research process. If AI reduces discovery costs by orders of magnitude, the ROIC (Return on Invested Capital) for genomics companies fundamentally changes.

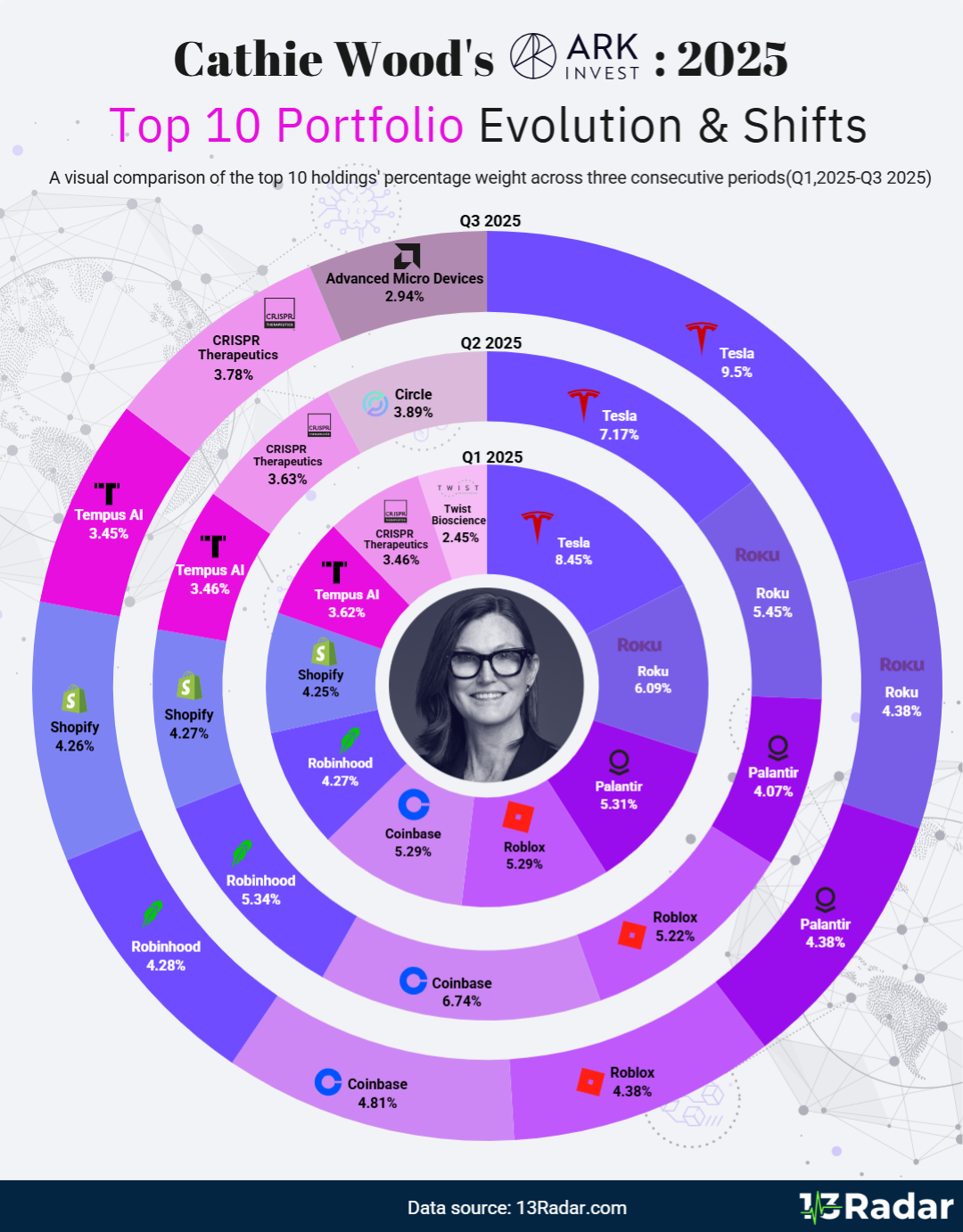

We are seeing some high-beta funds positioning for this outcome. A review of the catherine wood latest portfolio adjustments shows a notable pivot: selling liquid mega-cap tech proxies to accumulate deeper positions in multi-omics and molecular diagnostic firms. Whether one agrees with the ARK thesis or not, the flow data indicates a specific institutional bet on the "convergence" of biological data and compute power, essentially treating these bio-platforms as software companies in disguise.

SaaS Unit Economics: The Efficiency Narrative

The bearish case for SaaS was that "AI will replace software." The bullish counter-thesis—which is beginning to show up in earnings transcripts—is that AI acts as a deflationary force on SG&A and R&D expenses. Software companies that successfully integrate autonomous agents are seeing a path to meaningful operating margin expansion without linear headcount growth.

Institutional interest appears to be moving away from pure hardware exposure (where margins may have peaked) toward the application layer, where the "deployment phase" of the technology cycle typically generates the most durable cash flows.

🧐 Valuation Disconnect & Risk Factors

The Contrarian Monitor

For those tracking the rotation, the key metrics to watch in Q1 2026 involve divergence:

- Relative Strength: XBI (Biotech) vs. SMH (Semis). A breakout in this ratio often signals the start of a "risk-on" rotation into long-duration assets.

- Insider Activity: Notable lack of selling in mid-cap growth vs. record selling in mega-cap tech.

- Macro Sensitivity: These sectors remain highly sensitive to the 10-Year Treasury yield; the thesis relies heavily on yield stabilization.

This isn't a call to short hardware, but rather an observation that the asymmetric upside may have shifted. The "easy" beta trade is likely behind us, and alpha in 2026 will likely come from identifying mispriced adoption curves in the biological and application layers.

Itaque sed beatae quae veritatis porro. Magni illum facilis dolor vel. Soluta quibusdam expedita cum accusamus saepe nostrum. Quia laudantium in sit et eius accusantium magni accusantium.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...