Debtholders In M&A Deals

Can anyone help me and explain why debtholders seem to lose when the company is bought out?

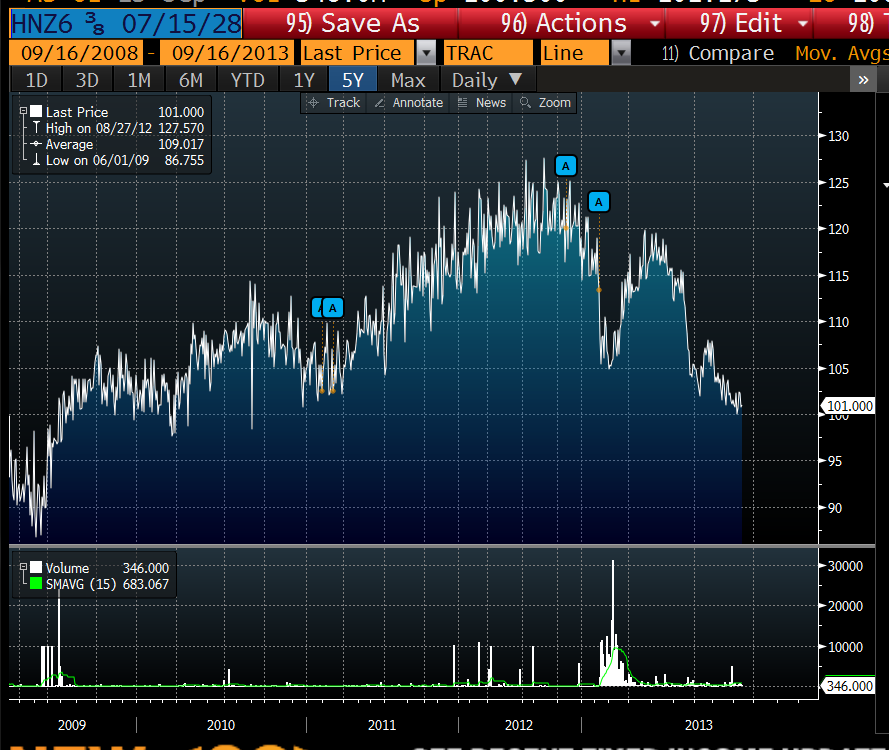

I'm looking at Heinz's for example and its price drops/yield rises when it was acquired.

| Attachment | Size |

|---|---|

| heinz acquired debt.PNG 114.4 KB | 114.4 KB |

{kind=link}

{kind=link}

i'm not as familiar with debt, but i think this is due to the YTM falling because of the change in control provisions in the indenture.

Probably has something to do w/the bond trading above par, but the value drops to/towards par when the debt gets retired from an acquisition.

The bond's prospectus says " The Company covenants that it will not merge or sell, convey, transfer or lease all or substantially all of its assets unless the successor Person is the Company or another Person organized under the laws of the United States (including any state thereof and the District of Columbia) which assumes the Company's obligations on the Debt Securities ". So I dont think a change in the control provisions is happening.

probably issue more senior debt (term loans, etc.) to fund the M&A?

The value of the debt to the debt holders (also the price of the bond) is the present value of the interest coupons on the cash flows discounted at the required rate of return. Since interest coupons on most debt instruments are fixed (even if it's floating doesn't matter because that just compensates for the market risk), the debt holders are getting the same return after the acquisition that they were before it. However now their required rate of return (RRR) has increased. Due to the new debt required to finance the acquisition being placed on the company's balance sheet, the risk to the existing debt holders of getting their money back has increased, and therefore RRR has increased.

So you are discounting the same stream of cash flows at a higher discount rate, meaning that the bond price should fall. It's the same mechanism that causes bond prices to fall when general interest rates increase, because now debt investors require a higher return to compensate them for their risk and opportunity cost of not investing elsewhere. That's why debt usually has clauses to be retired or assumed by the new owner during change of control scenarios such as in LBOs or acquisitions.

.

Whatever, I took a stab. Care to share what's so wrong about it?

Bonds are theoretically priced as the PV of future coupon payments + principal discounted at required yield. As yield goes up, prices fall (which is what seems to have happened in the Heinz case too).

I think the yield goes up because the existing debt holders are facing new risk - both of increased debt and of subordination to senior debt holders who provided capital to finance the transaction.

Change of control event triggered the 101 put, duh

Placeat recusandae et sunt voluptatibus voluptas totam recusandae. Occaecati neque est accusantium sequi inventore non. Recusandae dolore fugit maiores laboriosam. Corrupti quidem hic autem aut maiores. Mollitia a tenetur consectetur dolorem.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...