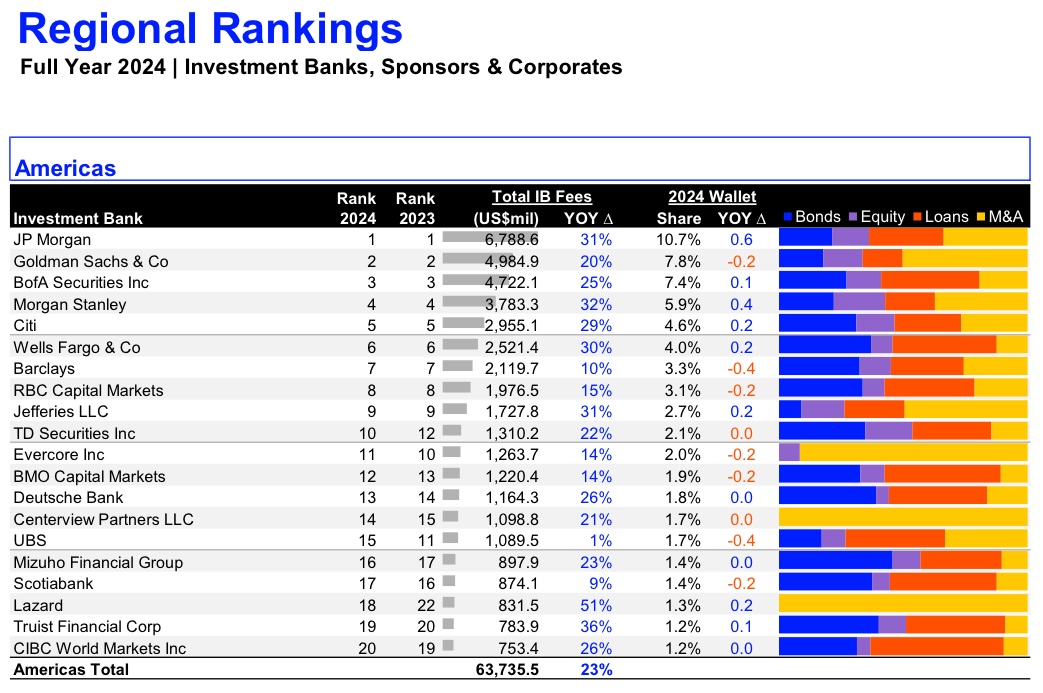

Insiders shocked as UBS drops to #15 in America’s IB Fees

Previously 11th with a 2.1% Wallet Share

Flat when markets up 20%…

Bonuses will suck…

Layoffs will be brutal…

Previously 11th with a 2.1% Wallet Share

Flat when markets up 20%…

Bonuses will suck…

Layoffs will be brutal…

| +157 | ONLY THESE BANKS OR YOU STRUCK OUT | 39 | 3h |

| +127 | Why UBS Is the Worst Place to Start Your IB Career | 15 | 46m |

| +115 | IB Energy Drink Tier List / Ranking | 74 | 2h |

| +65 | Firm Thinks I'm Lying About Offer | 20 | 3h |

| +54 | Indiana University Fraternity Pipelines | 34 | 2h |

| +39 | Stay at Weak Dealflow Team or Lateral? | 12 | 1d |

| +36 | Rogo AI | 15 | 2h |

| +36 | Elite Boutique interview questions | 8 | 1d |

| +34 | Suspended for a Year | 12 | 1h |

| +23 | 1st Half 2026 (1H26) RX IB & RX Co. Rankings | 14 | 2d |

Career Resources

Get instant access to lessons taught by experienced private equity pros and bulge bracket investment bankers including financial statement modeling, DCF, M&A, LBO, Comps and Excel Modeling.

Hard pass

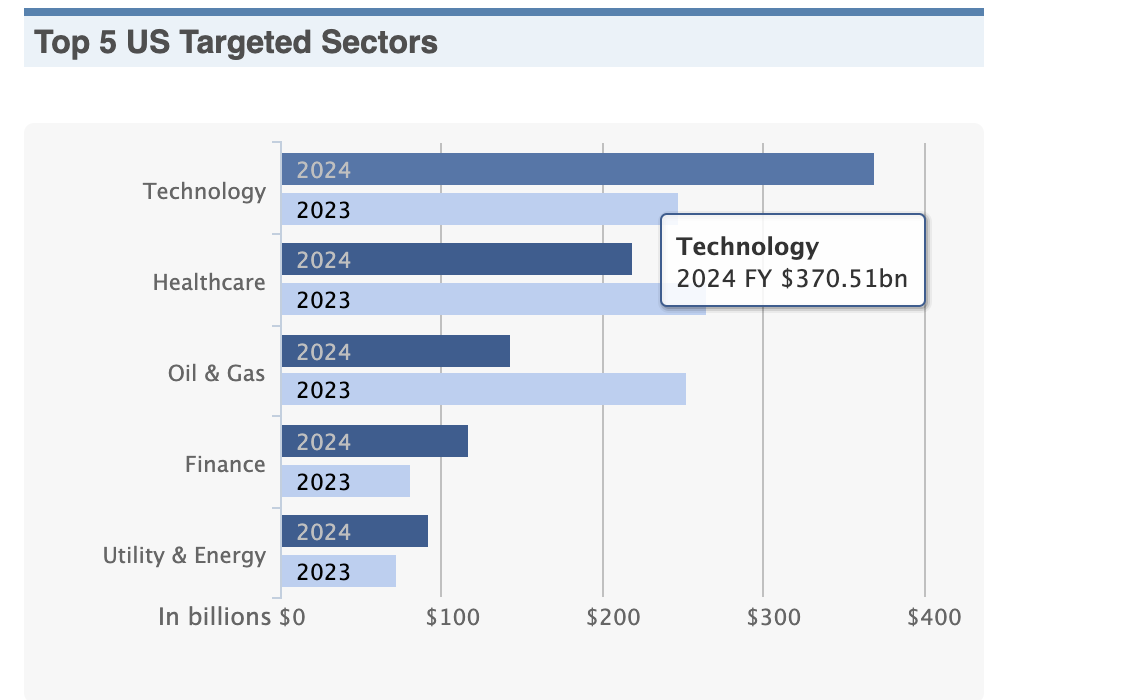

Each team gets its own bonus pool. UBS tech is a massive reason for their lower rankings than last year. Tech should take up 30-40% of a bank's wallet and was the big industry this year, it takes up 5-10% of UBS. This alongside a lack of energy business, one of the largest sectors this year, means UBS is going to do worse overall. Certain groups improved such as Industrials and LevFin, they will get fine bonuses. Some groups dramatically dropped the ball like Tech and M&T which will reflect in their bonuses.

Honestly impressive that it's even up 1% b/c that 2023 number includes some tech and M&T deal flow, primarily from the old CS franchise whilst there is none this year outside of ECM + LevFin-led things.

Edit: Just want to note that basically, no competing bank has Tech underperformed as much as UBS has, which is super relevant given it was by far the largest sector seeing almost $ 100B increase in M&A volume. That's basically all the transaction volume of the financials industry combined for 2024. UBS's strong suit industries in Industrials and Financials saw significantly less increase in overall deal flow, despite UBS's market share increasing. HC also saw a slight UBS market share increase but the healthcare M&A sector actually shrunk this year from ~$265Bn to ~220Bn. UBS outside of tech was better than last year.

WSJ league tables for reference:

Check FactSet for additional data; but UBS Tech had a decrease in market share whilst other groups such as LevFin, HC, GIG had increased. The problem for UBS is that this year was so Tech dominated that the bank saw a nearly flat overall bottom-line with only low single-digit fee growth because the tech team did so much worse when the broader tech world did so much better.

To summarize: UBS performed roughly the same as last year with some improvements in some groups market share wise, but the tech group massively dragged it down in a year dominated by tech transactions.

Thank you. It was the only logical and non-emotional answer about UBS I've read recently.

I think there are quite a lot of fairly balanced takes on this forum tbh. Just ignore the Tech people posting who hate it or the fanboys of it. I think the idea of some groups such as LevFin and Industrials doing better than last year has been widely espoused throughout the forum, particularly for those 2 groups. The HC one was a bit more shocking to me as well since I didn't assume it to be the case originally, but it seems like the team had semi-decent success at least in the sense of improving market share with their strategy of focusing on deal volume/doing a lot of MM deals and relatively fewer larger cap deals. FIG had a bit of an outlier year with some mega deals both in the very tail end of 2023 and in 1H 2024, but it is one of the stronger sectors at UBS, and the decline in overall financials wallet comparatively hurt UBS's fee growth.

Are you sure each team gets their own bonus pool? Historically juniors all were paid on a grid and end up with very similar per person numbers. Thus good groups subsidize bad groups

At CS previously, there was a decent bit of variability for bonuses. Beleive some analysts, specifically top bucket or middle bucket ones, in good groups got a decent chunk more than those in bad groups. Speaking off of CS experience, but there should be if that model has been retained.

This is my speculation as well, and it’s how it works at the bank I’m at (and is a source of frustration). Everyone quits the good groups because they get crushed doing all the deals and subsidize the bum teams

Even if Tech was 30% of fees for the bank it would still be nowhere close to where it needs to be

This is an example of the unbalanced takes you get on this forum that truly bring down the quality of discussion massively. Let me spell it out for you in an easier way to understand: the biggest sector this year by far was tech; the sector was so large that it was basically the combination of the next 2 largest sectors in M&A. Now in this sector, UBS massively declined but improved in most other sectors including the second and 4th largest sectors in M&A. The thing that is not reflected because WSJ does not give as much data as Factset does, but WSJ is the best that I can post since Factset is work-related content and I do not want to post from there. Additionally, the 3rd and 5th largest sectors are sectors in which UBS does not do business. UBS has as mentioned improved market share in most of it's other sectors, it's pretty clearly tech that is a large part of the issue for UBS with a lot of the rest coming from a distinct lack of O&G deals since again UBS doesn't do O&G but O&G was a massive sector this year in the US for this specific year.

Good answer

Is each teams bonus pool based on the teams revenue?

Mizuho making slow and steady progress... soon all of America will bow to the Divine Emperor of Japan and his trusted Shogun, Scott Bok.

TENNŌHEIKA BANZAI!

Boss down to our true ruler

Cooked

RBC UP AND COMING RAHHH

Wells Fargo on the rise… surprised BofA pays so poorly given their solid performance…

RBC is four times as good as UBS because it has double the revenue with just half the drama

Its like every year for the past 10-15 years, it drops a spot most years. In 5 years time it probably won't even be top 20.

Lazard will pass you guys soon on just advisory

I remember when they use to be top 10… sad…

If you have been following along on wso the last year, you would not be shocked. Stories coming out of there are horrendous

Hot Take: They will do worse in 2025

IF MS and GS had bad bonuses even after fees were up 20%, then UBS with Fees up 1% is simply going to have pizza parites instead of a bonus

Monetary Bonuses? Some groups will end up with RIFs as their bonus.

Earum amet ea quaerat voluptas aut veritatis. Reprehenderit et voluptatibus et et vel. Vel libero dolores modi in dolorem autem.

Eius recusandae libero similique iste. A praesentium rem cum necessitatibus voluptatem incidunt voluptatem sit.

Et quae aut ut error. Ratione vitae accusamus voluptatem et maxime. Fugiat velit ipsam ab eaque qui.

Quod reprehenderit vitae quidem eum illum minus beatae dolores. Totam tenetur officiis sapiente nisi. Qui nihil aspernatur nostrum molestiae ipsa iure. Occaecati numquam molestiae doloremque molestias eius.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Delectus consectetur deleniti nobis reiciendis. Ut itaque iste ex inventore veritatis nobis vero. Eligendi esse sed et saepe veniam.