UBS Banking Disastrous 3Q - More cuts coming?

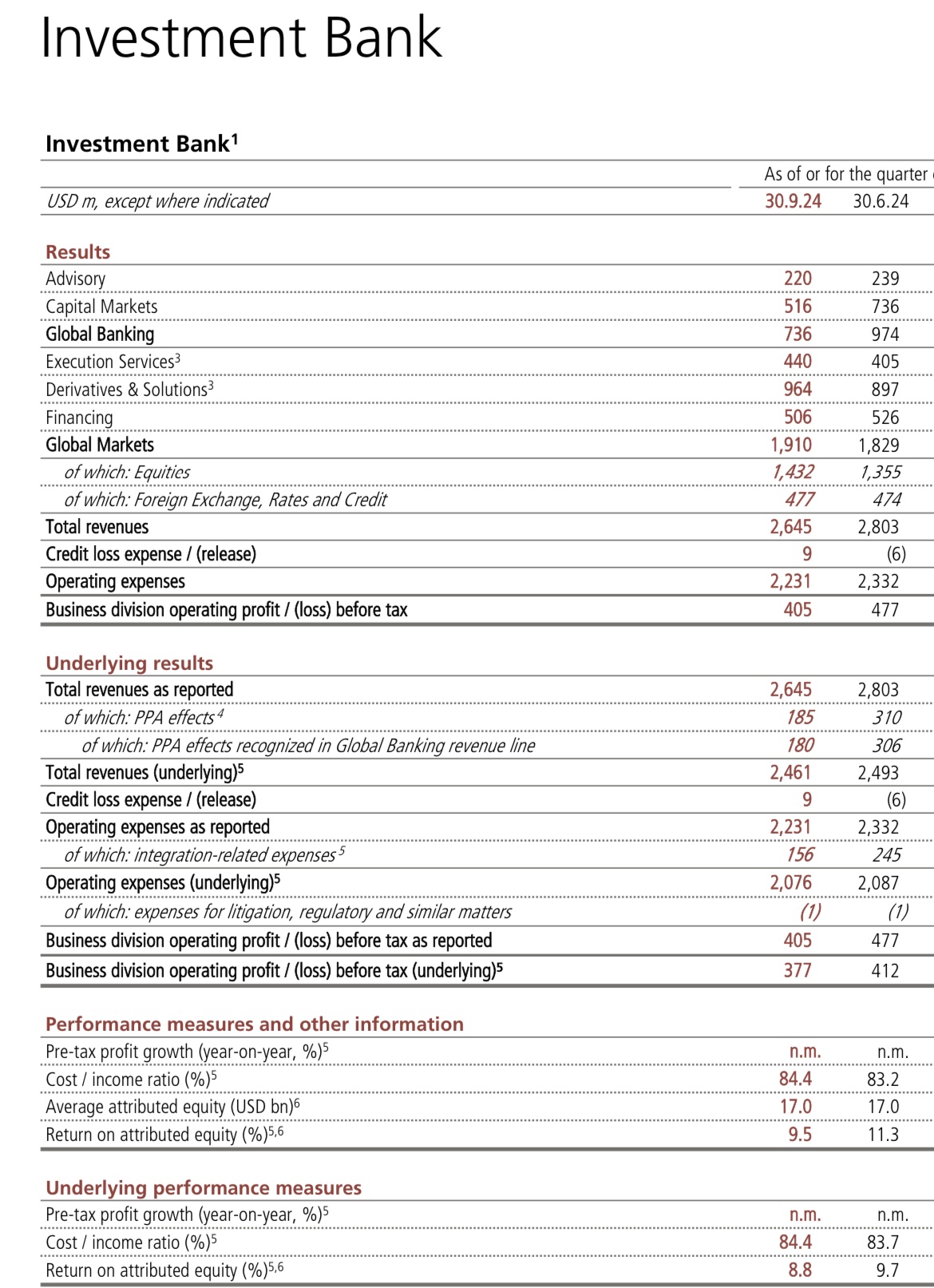

Revenue look down almost 10% QoQ and looks like advisory, capital markets, and financing all down. With cost / Income also going up they’ll have to do something about it…

ROE is less than 9%, is the investment bank even above the firms cost of capital?

Who looks at QoQ? Even MS was down from 2Q to 3Q because of seasonality in the summer months. The YoY is what matters and that was up 29% (21% when you exclude global markets)

Growth number is consistent with trend on the Street but below that of other banks which isn’t great

Barc: 58%

MS: 56%

Citi: 44%

JPM: 31%

GS: 20%

BofA: 18%

He does ->> Piers Brown - HSBC

Got two questions. I wanted to follow up on the previous Investment Bank question. But in terms of the Global Banking business, I mean you still obviously showing good year-over-year momentum but much weaker quarter-on-quarter as you guided into 3Q.

Pipeline sounds bad based on what Segio didn't say:

"As importantly, our M&A pipeline continues to build."

"we remain encouraged by the strength of our pipeline"

instead of saying strong, excellent, best its ever been etc...

Not going to speculate about Sergio’s exact choice of words since that seems pointless but here’s what the CFO said in response

“In terms of banking performance in the quarter, I still think it was a good performance. It outperformed the fee pool. We had a very strong first half of the year. 2Q was exceptionally strong. We had a bit of being forward as well as some deals that we were able to get done in 2Q and probably had the inverse dynamic happening in 3Q, where we had some deals pushed into the fourth quarter and this deals on the margin can make a difference on the performance in the comparative. But we remain very bullish on the pipeline.”

1 - Show me an example of a CFO saying their pipeline is very BEARISH. No consequence of using the wording BULLISH.

2 - Influencing the books between quarters? Tells me all MDs will push 4Q revenue to 1Q 2025 and an accepted practice. Lame excuse for bad banking 3Q quarter.

3 - UBS share price currently down 4%+ (Market didn't like what they saw) all while GS, EVR, CITI, BofA currently trading up today..

4 - Excuses already starting for 4Q:

"Yet the bank warned that geopolitical events, the US election and declining global interest rates would make the final quarter of the year hard to predict. The macroeconomic outlook for the rest of the world also “remains clouded,” it said. "

https://www.swissinfo.ch/eng/ubs-profit-outstrips-expectations-as-ceo-w…

Sergio: " We also maintain a top 10 ranking across the street and announced M&A volume."

Looks like they found the 1 data provider who says they are top 10?

#12 per FactSet on announced transactions:

https://go.factset.com/hubfs/mergerstat_em/quarterly/AdvisorQuarterly.p…

#11 per LSEG

https://thesource.lseg.com/thesource/getfile/index/343f6a50-49bd-43ec-9…

Outisde top ten per FT Times

https://markets.ft.com/data/league-tables/tables-and-trends/mergers-and…

Lol not sure why you care so much but it’s funny so keep it up.

Stock price is affected by the potential regulation not by the performance of one segment like the IB

https://www.reuters.com/business/finance/ubs-posts-bigger-than-expected…

**Lack of performance by one unit

typo fixed it

I prefer investment banks who earn more in each successive quarter

One year later still the same

Fuga consequatur repellendus rerum quis et saepe consequatur. Dolor totam eius aliquam quis aliquam voluptas. Distinctio quia ut rerum possimus sed aut est. Pariatur expedita ut sit.

Fugit dolore sapiente voluptatem. Aut ex id necessitatibus voluptatibus. Quod temporibus consequatur facere animi quia repellat harum. Minima necessitatibus provident quia voluptas. Provident voluptas ut maxime aut ut modi modi. Repudiandae fuga tempora asperiores illum dolores.

Nostrum ut magni exercitationem fuga pariatur. Voluptatem modi eaque et molestiae ullam non modi.

Rem fuga aperiam quam iste iure consequuntur laborum. Nostrum dolor ipsum at ut est aspernatur fuga.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...