WSJ: Centerview Partners Considers a Deal of Its Own After Record Year

Surprised there isn't a topic on this already.

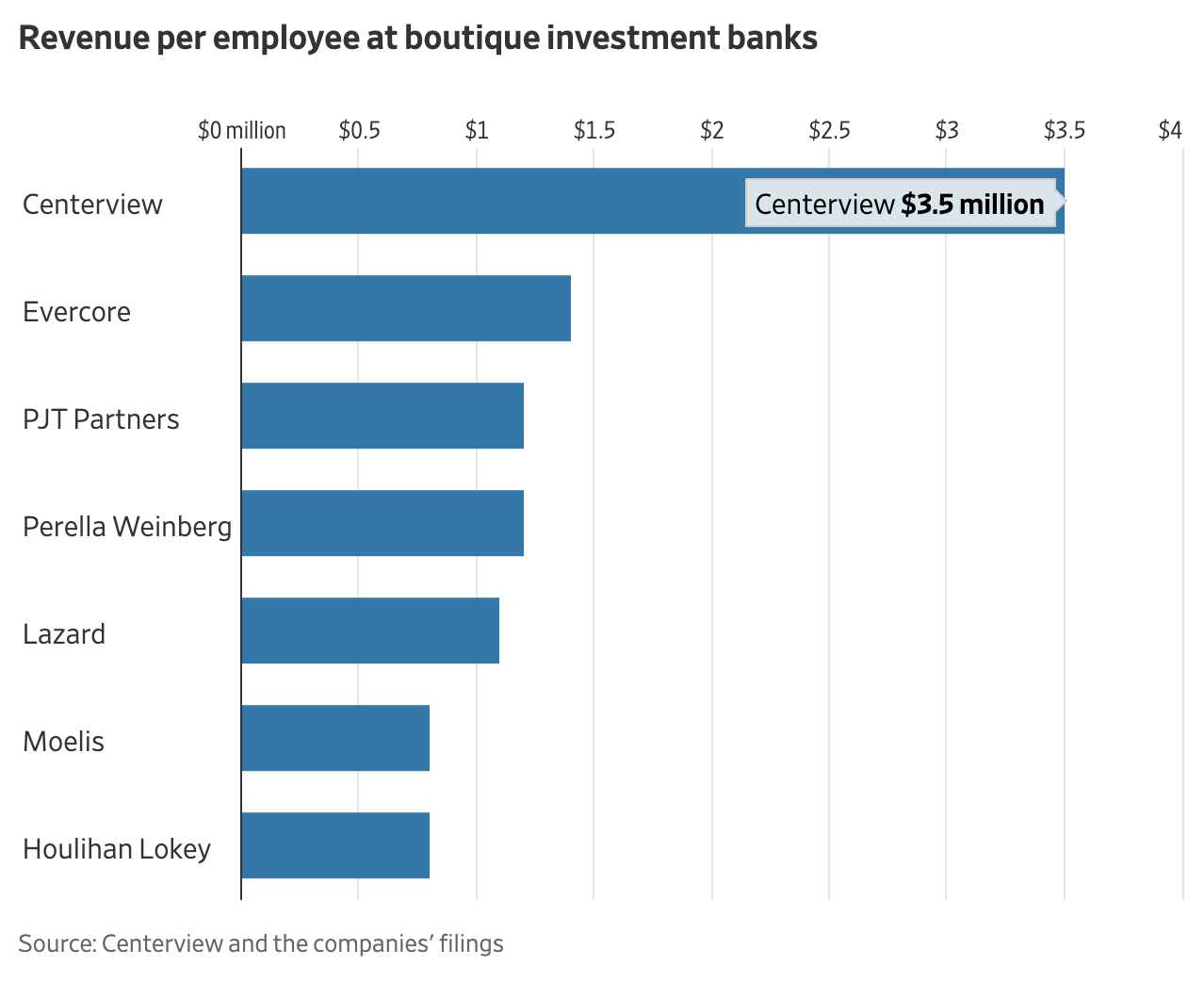

WSJ this morning reported Centerview is considering a sale:

The firm is becoming more open to exploring its options, Centerview co-founder Blair Effron suggested in a recent interview. Those could include selling a stake in the firm to an outside investor or going public.

Obviously an incredible year for a firm with a little over 600 staff – FT's league tables had them #4 just under BofA in terms of fees. Will be interested to see their performance relative to the other EBs as tech M&A picks up again but clearly they are well positioned for 2025.

That's crazy. Seems it's being mostly driven by liquidity needs of their long-term partners, a la Greenhill.

Can you explain the Greenhill linkage? A cursory Google search doesn't show anything

.

Partners just want to cash out. They should consider an IPO, I'd buy

It’s not really a bussiness but a couple dozen rainmakers. When they cash out and leave it starts a sharp decline

This IMO. CVP has yet to prove that it can scale and dominate effectively in global M&A for eg like Evercore. Feels like the public markets will discount their smaller scale vs the larger EBs that are growing / scaling (PJT, MOE).

You know it's true because Blair Effron keeps going on tv to say that it is not true.

CVP will most likely sell at a premium to a large bank looking to grow their IB just as Greenhill did. It won't be super expensive given how much these banks make quarterly in pure profit and it can mean a quicker liquidity event for these founders vs IPO'ing. IPO'ing can also be dangerous as you have a lock-up period, much better for these founders to sale. Most likely the senior rainmakers will have to stay for 3-5 years as they are key employees, but after that they'll have tens of millions to spend as they wish if not even more.

The real question is who do we think would be possible buyers?

UBS

Please let this happen, and have the CVP people kick out the barclays people

Seems unlikely given that CVP spun out of UBS, Effron and the OG CVP people are ex-UBS. Not a good look to investors to buy back an IB firm that you could've had if you gave one dude more money back in the day.

Blackrock is acquiring all different firms to diversify revenue. Could they look to get into M&A?

Nah. Buying an advisory shop like CVP means they would have to divest a ton of their businesses due to conflicts of interests.

It would be funny if Blackstone was a buyer after carving off what became PJT

Does anyone know what this sentence means? “Close to 30% of the firm’s revenue today comes from general advisory, rather than deals.”

Advisory is M&A right? There can’t be that many defense assignments or Rx at CVP. Are they getting a subscription fee to be outside corp dev? I am lost

From my understanding, they’re on retainer with a number of clients

That's essentially a generic "strategic advisory" services which pretty much encompasses a wide range of corporate matters unrelated to M&A or transactions (e.g., advising on dividend policy, corporate governance, or other strategic matters). All EBs do that, to some extent (you don't think all day they're churning M&A / RX deals, right? There aren't that many deals for all these firms, even in the MM space that a lot of them operate in (e.g., (Moelis))

Thanks. In my experience, all of that advisory work is done for free so you get the M&A fee when it presents itself. I don’t know how you can expect to get paid on an ongoing basis for telling someone what you think their dividend strategy should be. Also really curious what they charge and how they get it so we can ask for it too.

The strategic advisory work at CVP is much more broad corporate advisory and quite differentiated vs. other traditional investment banks (both bulge brackets and boutiques that brand their M&A practices as “strategic advisory”).

Best way to think about it is a blend of strategy consulting akin to a mini Bain/BCG, shareholder messaging / investor relations, geopolitical advisory, and other non-transactional financial advisory services (e.g. capital allocation, capital structure, CEO transitions etc).

This is provided on a retainer basis and typically targeted at large cap F500 (example clients include Disney, Target, Honeywell, Capital One, etc.)

Sounds more like good old friends just taking care of friends. I mean CV advised WBA … and look what happened w that high value advice (can probably find 20 other examples)

Great answer, appreciate you sharing. Now, how do I sign up some clients for that…

Facere quae quas cumque et. Qui facilis a aut iure aut adipisci. Ut ad placeat modi nulla est. Quia molestias itaque a commodi quam ut.

Pariatur sint cum in nobis est magnam. Dolorum nostrum vero pariatur neque assumenda beatae in. Quis fugiat in rerum deserunt aut ratione dolorem. Doloribus eveniet et laboriosam perferendis illo qui velit. Consequatur necessitatibus explicabo totam dolor est iusto nemo. Occaecati ducimus quasi neque error sit dicta tempore expedita.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Rem praesentium unde molestiae ipsam qui saepe voluptatem. Et fuga ea non sequi qui. Sint adipisci expedita magnam molestiae magnam et. Enim necessitatibus aut eos veniam debitis.

Id unde vitae commodi fuga quo tenetur. Facere et natus porro necessitatibus velit et. Aliquam iusto unde ut autem molestiae cupiditate.

Sint libero facilis aperiam voluptas ea aspernatur. Earum placeat illo minus recusandae labore ipsa qui nesciunt. Qui et et rerum. Veritatis natus et quas fugiat quae iste sunt quasi.