Double Entry

A method of recording both the debit and credit sides of an accounting transaction.

What Is Double Entry?

A double-entry system of accounting is a method of recording both the debit and credit sides of an accounting transaction. For instance, when paying cash, things are received, and currency is exchanged.

Receiving items and paying cash are the two transaction components that must be recorded using the double-entry system. Receiving things is one element of the debited transaction, and paying cash is the other.

In other words, if only accounts are impacted (like in the case of the cash purchase of a building), the sum is debited from one account, Building, and credited to the other account, Cash.

When a transaction affects more than two accounts, the total of the debit entries and the total of the credit entries must match. As a result, the total amount deducted and credited on any given day is equal.

Let’s take a look at the features of the double-entry system:

- It keeps an accurate record of every transaction.

- This system recognizes two components in every transaction: a receiving component (value in) and a providing component (value out).

- In this system, following the rules of debit and credit, one element is debited, and the other aspect is credited.

- The sum of all debits is always equal to the sum of all credits since each transaction has one debited and one credited component. Creating the Trial Balance aids in proving mathematical accuracy.

The following three steps make up a complete double-entry bookkeeping system:

- Keeping a journal of the transactions.

- Creating the Trial Balance after classifying transactions in the Journal by publishing them to the appropriate ledger accounts.

- Compiling the final accounts and closing the books.

Double Entry: Charts Of Accounts

In a double-entry accounting system, a chart of accounts is a list of all the accounts an organization uses to record its financial transactions. It is a complete listing of all the accounts used by a company to classify and record its financial transactions.

The chart of accounts provides a systematic and structured approach to bookkeeping, ensuring that financial statements are accurate, reliable, and comprehensive.

The chart of accounts typically includes a series of categories and subcategories that help organize the company's financial data. These classes include assets, liabilities, equity, revenue, and expenses.

Assets

Assets are resources a company owns or controls, expected to provide future economic benefits. Those benefits can come in the form of expanded sales, decreased expenses, or multiplied asset costs over the years.

Here are some examples of asset accounts that might be included in a chart of accounts:

- Cash

- Accounts Receivable

- Inventory

- Property, Plant, and Equipment

- Investments

- Prepaid Expense

Each of these asset accounts has a normal debit balance, which means that an increase within the account is recorded as a debit, and a reduction is recorded as a credit.

This maintains the balance of the accounting equation (Assets = Liabilities + Equity) and ensures that the financial statements accurately reflect the company's financial position.

Liabilities

Liabilities are obligations that a company owes to external parties, such as suppliers, lenders, or customers. These obligations can arise from transactions such as loans, accounts payable, or taxes owed.

The liabilities category in a chart of accounts is usually divided into subcategories, each representing a specific type of liability. The subcategories may include:

- Current Liabilities

- Long-term Liabilities

- Contingent Liabilities

When liability is incurred, it is recorded in the appropriate account within the chart of accounts using the double-entry accounting system.

NOTE

The liability account is credited, representing the increase in the company's obligation, while the corresponding account is debited, representing the decrease in assets or increase in expenses.

Revenue

Revenue is a critical account in the chart of accounts for any company that generates income. In the double-entry accounting system, revenue is recorded as a credit entry, indicating that it increases the company's equity.

NOTE

The revenue account is typically classified as an income statement account and is located within the "revenue" category of the chart of accounts.

This category may also include subcategories:

- sales revenue

- service revenue

- rental revenue

- Depending on the nature of the business' operations, interest revenue.

Since the revenue account is a nominal account, it is closed at the conclusion of each accounting period to ascertain the business's net income or loss.

When a sale is made, revenue accounts are credited, and the amount credited represents the revenue made by the business. For instance, if a corporation sells things worth $1,000, the revenue account will receive a $1,000 credit.

Expenses

They represent the expenses an organization incurs in carrying out its daily activities, including wages, rent, utilities, and supplies. Expenses must be properly classified and recorded for accurate financial reporting and decision-making.

Expenses are generally categorized into different categories, depending on the nature of the cost. These categories may also include:

- cost of goods sold (COGS)

- Operating Expenses

- Non-Operating Expenses

By properly classifying and recording expenses, businesses can analyze their spending and identify areas where costs can be reduced or eliminated.

NOTE

The chart of accounts for expenses provides a structured approach to accounting for these costs, making it easier to track and manage them. It also helps businesses prepare accurate financial statements, which is essential for making informed business decisions.

Equity

Equity is a fundamental category in the chart of accounts within the double-entry accounting system. Equity refers to the residual interest in a company's assets after deducting liabilities. It represents the company's value that belongs to the owners or shareholders.

Equity accounts are important in determining an enterprise's financial health. Together with the balance sheet and the statement of changes in equity, they are used to prepare financial statements.

Within the equity category, several subcategories provide more detail on specific transactions. Some common equity accounts include:

- Capital Stock

- Retained Earnings

- Treasury Stock

- Dividends

When recording transactions in the equity category, the double-entry accounting system requires that every transaction affecting equity must have a corresponding debit and credit entry.

What Is Debit And Credit

It is based on the idea that each monetary transaction has equal and opposite effects, recorded in distinctive accounts—a debit account and a credit account—and is equal and opposite in nature.

The double-entry system ensures that the accounting equation is consistently balanced and the accounting records are error-free.

In the double-entry system, debits and credits are two types of entries made in the accounts books. Credits are entries that raise liabilities and equity or reduce assets and costs, whereas debits increase assets and expenses or decrease liabilities and equity.

Every financial transaction is recorded in at least two accounts, with one account debited and the other credited.

For example, when a company purchases inventory on credit, the inventory account is debited while the accounts payable account is credited.

This means that the company has increased its inventory assets by purchasing inventory but has also increased its liabilities by owing money to its suppliers.

Similarly, when a business sells products on credit, the revenue account is credited while the accounts receivable account is debited.

By registering the debt owed to the business by its clients, the corporation has increased its assets and raised its revenue by closing a sale.

Real-World Example Of Double Entry

The financial records of a retail store provide a practical illustration of the double-entry system. For example, let's say that the store sells clothing and accessories and uses the double-entry system to keep track of its financial transactions.

When a customer purchases a shirt for $50 using a credit card, two entries are made in the store's books of accounts. The first entry is a debit entry, which increases the store's cash account by $50, representing the amount received from the credit card transaction.

The second entry is a credit entry, which increases the store's sales revenue account by $50, representing the revenue earned from the shirt sale.

In this example, the double-entry system ensures that the accounting equation remains balanced, as the total assets (cash) increase by $50 and the total equity (sales revenue) also increases by $50.

The transaction also affects the inventory account, which is credited for the cost of the shirt sold, reducing the inventory asset by the same amount.

Another example is when the store purchases inventory on credit for $500. In this case, the inventory account is debited by $500, representing the increase in inventory assets.

The accounts payable account is credited by the same amount, representing the liability owed to the supplier for the purchase of inventory.

These examples show how the double-entry system records every financial transaction in two accounts, ensuring that the accounting records are accurate and that the financial statements provide a true and fair view of the company's financial performance and position.

Advantages And Disadvantages Of Double Entry

Since ancient times, double-entry bookkeeping has been a common practice in accounting. However, it offers some benefits and disadvantages, which can be important to remember.

The advantages are

- Accuracy: The double-entry system ensures accuracy in the accounting records by requiring every financial transaction to be recorded in two accounts. This makes it simple to find and amend any mistakes or omissions.

- Financial Reporting: The double-entry method provides a clear and accurate image of a company's financial situation, performance, and cash flows. Making informed decisions is important for tasks like determining a firm's value or evaluating its creditworthiness.

- Internal controls: The double-entry system offers a framework for internal controls that could help prevent fraud, embezzlement, and other monetary irregularities. By separating the duties of recording and approving transactions, the system can help detect and deter fraudulent activity.

- Audit trail: The double-entry system creates a clear and complete audit trail that can be easily traced back to the original transactions. This is essential for compliance with accounting standards and regulations.

The disadvantages are:

- Complexity: Putting in and maintaining the double-entry system can be hard and time-consuming, especially for small businesses with confined assets. In addition, it necessitates proficiency with accounting software and tools and knowledge of accounting principles and procedures.

- Cost: The double-entry system may be high-priced to enforce and hold, especially for corporations with an excessive volume of transactions. This includes the cost of software, training, and hiring accounting professionals.

- Human error: Despite its accuracy, the double-entry system is still vulnerable to human error. For example, errors in data input, coding, or classification errors may significantly impact the financial accounts' accuracy.

- Limited flexibility: The double-entry system can be inflexible, especially when making adjustments or corrections to the accounting records. This might be difficult for companies that must change their financial statements frequently or quickly in response to changing conditions.

Double Entry Summary

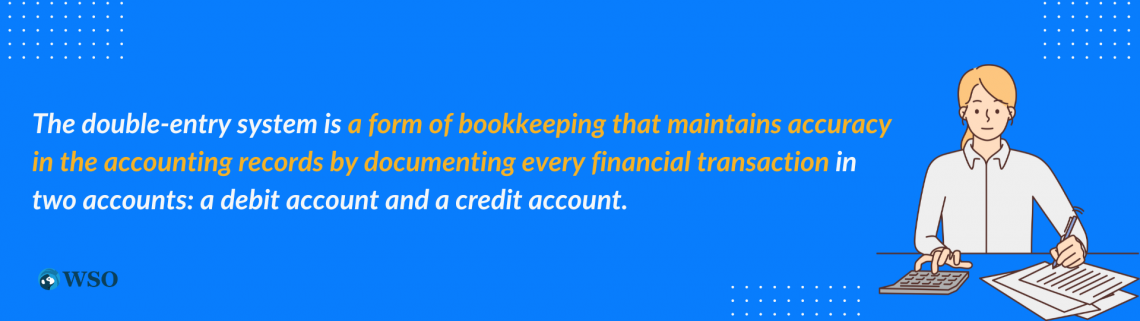

A double-entry system is a form of bookkeeping that maintains accuracy in the accounting records by documenting every financial transaction in two accounts: a debit account and a credit account.

While credits increase liabilities and equity or decrease assets and expenses, debits either increase assets and expenses or decrease liabilities and equity.

The chart of accounts is a key element of the double-entry accounting system that offers a framework for classifying and documenting financial transactions.

It enables businesses to categorize and record their financial data precisely and consistently, assuring the accuracy and thoroughness of financial reporting.

By implementing a chart of accounts, businesses can speed up their accounting processes and reduce the likelihood of errors and inaccuracies.

NOTE

Before establishing the double-entry method in a business, thoroughly weigh its benefits and drawbacks.

While it offers accuracy, financial reporting, internal controls, and an audit trail, it may also be expensive, rigid, complicated, and prone to human error.

As with any accounting technique, the suitability of the double-entry system depends on the particular requirements and circumstances of the business.

Double Entry FAQs

For every financial transaction, two accounts are affected. One account is debited, and another is credited. The total debits must always equal the total credits, ensuring the accounts are balanced.

Examples include recording the purchase of inventory, the payment of salaries, or the receipt of cash from a customer.

While double-entry accounting isn't required through regulation, it is the usual accounting exercise for most businesses and is strongly recommended by means of accounting professionals.

Single-entry accounting only records one side of a financial transaction, while double-entry accounting records each transaction's debit and credit sides. As a result, double-entry accounting is more accurate and provides a clearer picture of a company's financial health.

Double-entry accounting can be done manually using a ledger and pen/pencil. However, the software is recommended as it can automate the process, reducing the risk of errors and saving time.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?