Savings and Loan Crisis

Commonly known as Thrift, it was a cooperative institution that provided first-time house buyers with mortgages in the U.S.

What Was the Savings and Loan (S&L) Crisis?

The Savings and Loan Association (S&L), commonly known as a thrift, was a cooperative institution that provided first-time house buyers with mortgages in the US.

During the 19th century, banking was used mostly by those with assets or wealth that needed safekeeping. However, savings banks were established in the USA and UK for the first time in 1816 and 1810, respectively.

In their early years, savings and loan associations worked as cooperatives, in which everyone who deposited money was a shareholder.

Depositors would receive dividends or interest on their savings by lending a portion of the deposit to the same depositors who wanted to buy a house.

The savings and loan crisis is a part of history mostly overshadowed by other big economic crises, such as the 2000 dot-com bust, the 2008 global banking crisis, or the Great Depression.

This crisis can teach us valuable lessons by helping us understand the relationship between the market condition at the time and the policies enacted that led to the crisis.

- The Savings and Loan (S&L) crisis was a financial crisis that occurred in the United States during the late 1980s and early 1990s.

- It primarily involved the failure of savings and loan associations (S&Ls) or thrifts, which were financial institutions specializing in accepting savings deposits and providing mortgage loans.

- While the S&L crisis shares some similarities with other financial crises, such as the subprime mortgage crisis of 2007-2008, it was unique in its causes and regulatory response.

- The U.S. economy eventually recovered from the S&L crisis, aided by regulatory reforms and economic expansion in the 1990s. However, the crisis left a lasting impact on the financial industry and regulatory landscape.

History of Savings and Loan Association

In the early days, banks did not provide home mortgages. Only insurance companies provided mortgage services, and the terms of the mortgages, let's just say, were not favorable to the average American at the time.

The mortgages had some kind of balloon payment at the end of their term. In addition, some were interest-only loans, which made paying the principal very difficult. This created a lifelong cycle of refinancing or, in most cases, led to the house's foreclosure.

Due to these unfavorable terms, people needed help getting mortgages to buy houses. So, communities established S&Ls as an alternative to help their constituents buy houses.

The Savings and Loans Association was like a cooperative in which a community pooled their savings, gave home loans to people who wanted to buy a house in the same community, and charged interest on the loans.

The depositors were the shareholders in the association and had voting rights on its decisions.

During the Great Depression, the US government wanted to kick-start the slowing economy and boost home ownership to increase economic activity.

To achieve this, US Congress took the following steps:

- The US Congress enacted the Federal Home Loan Bank Act in 1932.

- The Federal Home Loan Bank Board (FHLBB) was established to assist other banks in providing long-term funding.

- The Federal Savings and Loan Insurance Corporation (FSLIC) was established under the FHLBB.

- This made the deposits in S&L insured by the federal government up to a certain amount, just like the FDIC, which was used to insure bank deposits.

Note

Savings and Loan Associations were like banks, but a community established them to promote home ownership among its members.

A booming economy, the growing middle class of the 1950s, and the new governing body created an environment in which S&L grew exponentially. Further regulations in the 1960s and 1970s made it so that by the 1980s, S&L was working like regional banks.

They were no longer established non-profit institutions to help their constituents buy houses; they were now full-fledged financial institutions.

Early Stage of Savings And Loan Crisis (1966 - 1979)

The Sine of Savings and Loan Crisis started in late 1970 when the Federal Reserve raised interest rates sharply due to high inflation and a slowing economy.

Until 1982, the federal government banned adjustable-rate mortgages. So, when the interest rate rose sharply, there was a situation of asset-liability mismatch; the short-term cost of S&L rose, but their returns remained unchanged due to fixed-rate mortgages.

This caused them to charge higher mortgage interest, and the demand for new loans fell.

As demand for new mortgages fell, the S&L could not increase their earnings and the interest rate on savings to retain deposits and attract new ones.

The creation of money market funds created more problems for the banking industry. The higher interest rate on these funds made the depositors take their money out of S&Ls, creating more pressure on the industry.

In 1979, doubling oil prices and high inflation took the S&Ls to their limit; most S&Ls were almost on the verge of bankruptcy. In addition, the housing market dried up, and S&Ls could not grow as they needed to be more extensive in where to invest.

Note

The savings and loan crisis started because of rising interest rates, which created an asset-liability mismatch in S&Ls books, and competition from new money market funds, which drained their deposits.

Reaction to Growing Stress in the Saving and Loan Associations

In the 1980s, the US Congress passed regulations to help S&Ls. These new regulations gave S&Ls the capabilities of commercial banks without the same regulations as banks. The Carter Administration passed the Depository Institutions Deregulation and Monetary Control Act.

This legislation brought many changes, but the most important of all was the following:

- It removed the interest rate ceiling on deposits, preventing the S&Ls from offering higher interest rates to attract new deposits.

- It increased the deposit insurance limit of federally chartered S&Ls to $100,000 from $40,000

- It also allowed them to make consumer loans up to 20% of their assets and invest up to 20% of their assets in commercial real estate loans.

In 1981, the Economic Recovery Tax Act made it so that S&Ls could sell their mortgage loans and use the cash to generate more returns, the loss incurred during the early sale of mortgages could now be offset against tax paid over the preceding ten years.

In 1982, more deregulation took place. The Federal Home Loan Bank Board reduced the net

worth the requirement for insured S&Ls from 4 to 3% of total deposits.

They were allowed to report their net worth using more relaxed Regulatory Accounting.

Principles (RAP) and GAAP, or Generally Accepted Accounting Principles, were not mandatory.

The Bank Board changed the structure of S&Ls, now allowing a single person to own the organization.

States also started to pass their deregulations of S&Ls, under the state's chart to match the regulation of the federal government-chartered S&Ls.

California passed the Nolan Bill, which allowed its S&Ls to invest 100% of their deposits in any venture. These deregulations made three states, California, Texas, and Florida, become hotbeds for S&Ls.

In 1982, the Garn-St. The Germain Depository Institutions Act was passed as the Reagan administration wanted to deregulate the S&Ls even more.

Due to the previous regulation change and the lower interest rate, S&Ls showed some stability, and the White House pushed for more deregulation. However, 9% of all S&Ls were still insolvent under GAAP standards, and 35% were still sustaining losses.

Most S&Ls were insolvent but were kept afloat by accounting tricks. The Bank Board, responsible for regulating the S&Ls, needed more staffed and paid. A starting S&L examiner was paid only $14,000 a year by the Office of Management and Budget (OMB).

The industry grew rapidly due to deregulation, and the regulatory bodies needed help to keep pace.

This lack of oversight made it easier for S&Ls to make risky investments.

Appointment of the new chairman of the Federal Home Loan Bank Board

Edwin Gray became the new chairman of FHLBB in March 1983 for a partial term, then again for a full term in 1984.

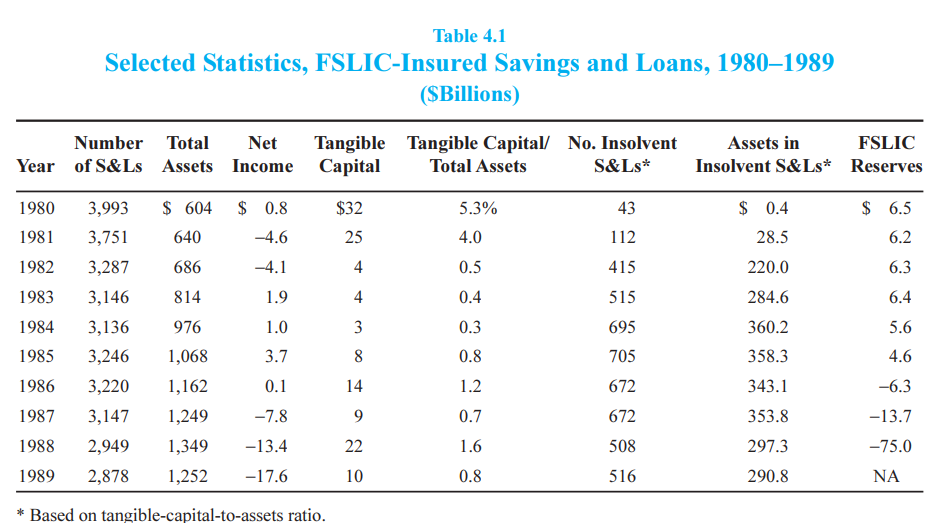

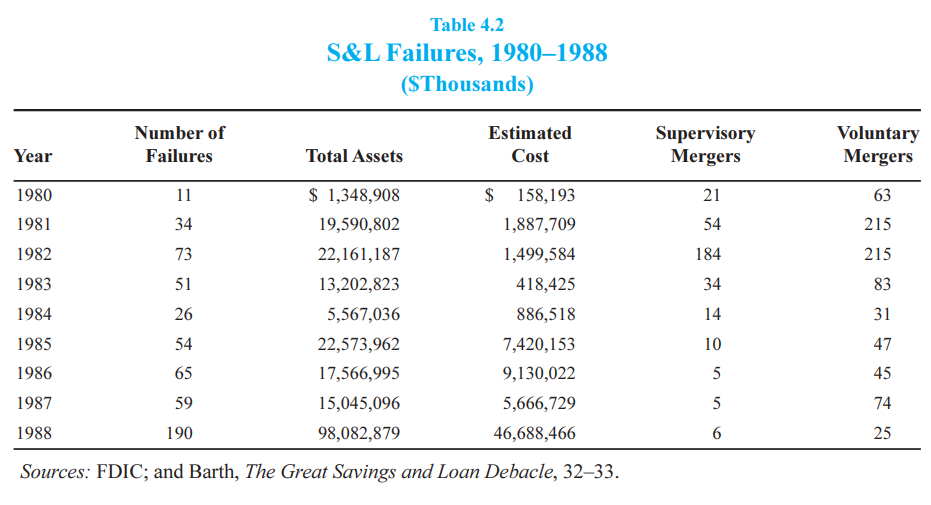

S&Ls' losses in 1981 and ‘82 were $4.6 billion and $4.1 billion, respectively. However, after deregulation, S&Ls recorded profits of $1.9 billion in ‘83 and $3.7 billion in ‘85. As the profit grew, tangible capital plummeted.

In 1980 and ‘81 S&Ls had $32 billion and $25 billion in tangible capital, respectively; in 1982 and ‘84, they stood at $4 and $3 billion. And the number of insolvent S&Ls based on the tangible capital to total assets ratio grew from 43 to 705 from 1980 to 1985.

In 1983, FSLIC had only $6.3 billion in its reserves to insure all the deposits in S&Ls, but the total assets in insolvent S&Ls stood at $284.6 billion.

Source for Tables: History of the Eighties - Chapter 4 (fdic.gov)

The FHLBB took the following steps:

- They transferred federal examiners to the regional FHLBs to remove OMB's influence, and the Bank Board was to pay their salaries directly.

- They began to reverse some relaxation given to S&Ls, but the lobbyists for S&Ls fought this hard in Capital Hill.

- In 1985, when some of the biggest S&Ls started to fail, Ohio declared a banking holiday to buy time to solve the Home State Savings Bank failure.

- The state government closed all the S&Ls that the state insurance fund insured, and later Ohio declared its state insurance fund bankrupt.

- In 1985, FSLIC had only $4.7 billion in its fund, and Chairman Gary tried to get recapitalization from Capitol Hill.

- The lobby of S&Ls fought hard because the Bank Board was pursuing harsh regulations and registered the regulator's efforts.

But the writing was already on the wall. The industry had become too toxic for the financial system; something had to be done on the legislative level.

Big Failures and Scandals during the Savings And Loan Crisis

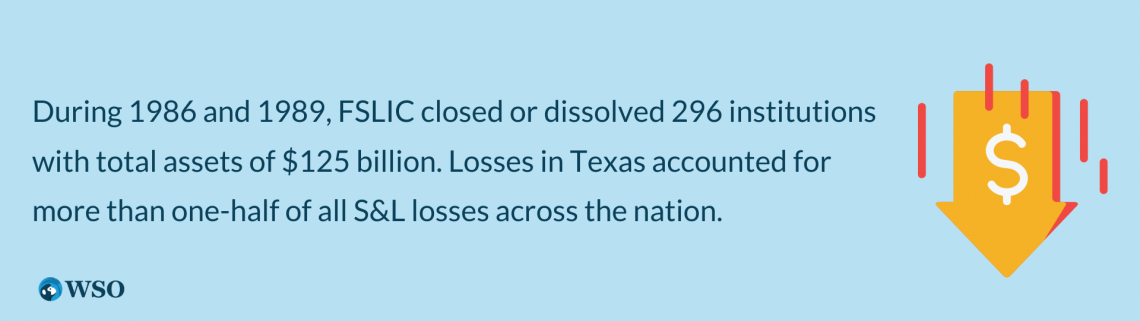

During 1986 and 1989, FSLIC closed or dissolved 296 institutions with total assets of $125 billion. Losses in Texas accounted for more than one-half of all S&L losses across the nation.

The scandal surrounding Jim Wright and the Keating Five drew the ire of Congress.

Enactment of the Competitive Equality Banking Act of 1987 provides a total recapitalization of $10.8 billion for the FSLIC, but only $3.75 billion was authorized in any 12 months.

The Bank Board proposes the "Southwest Plan" to merge and package insolvent Texas savings and loans and sell them to the highest bidder. The objective was to resolve insolvencies swiftly while conserving FSLIC's limited funds.

The Bank Board employs various techniques to cover the difference between the assets and liabilities of insolvent banks, including FSLIC notes, tax breaks, income, capital value, and yield guarantees.

The Bank Board sells 205 savings and loans worth $101 billion through the Southwest Plan.

Resolution to Savings and Loan Crisis

The new chairman of FHLBB knew something had to be done as FSLIC was technically insolvent and could not meet its insurance commitment with its current reserves.

During the next presidential run, the savings and loan crisis was largely ignored by both parties' campaigns, as both sides could be blamed for the mess that was created. And no party wanted to admit that taxpayers' money had to be used to solve the problem.

Both sides knew the cost would be massive and decided to deal with it after the election. The resulting election made George Bush the president of the USA. He knew the S&L industry had to be controlled, and a total restructure was needed.

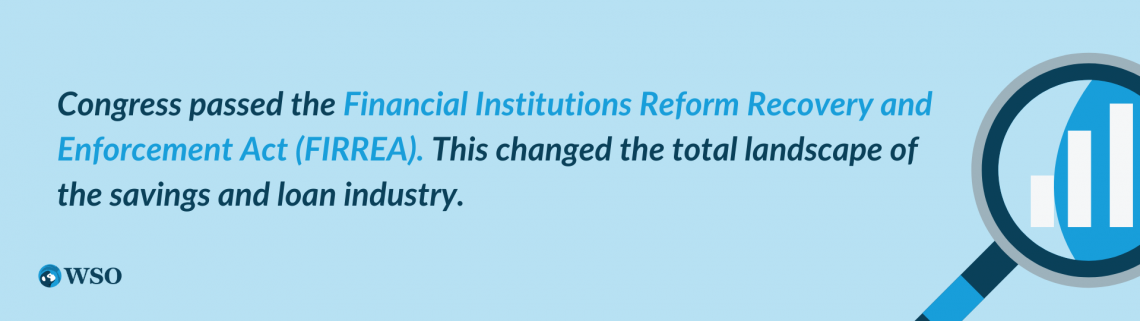

Congress passed the Financial Institutions Reform Recovery and Enforcement Act (FIRREA) to achieve this. This changed the entire landscape of the savings and loan industry.

Following are some of the highlights of FIRREA:

- The Federal Home Loan Bank Board (FHLBB) and the Federal Savings and Loan Insurance Corporation (FSLIC) were closed.

- The United States Treasury established the Office of Thrift Supervision (OTS) to charter, regulate, examine, and oversee savings institutions under FIRREA.

- The Federal Housing Finance Board (FHFB) was established as an independent organization to replace the FHLBB, i.e., to manage the 12 Federal Home Loan Banks (also known as district banks).

- The Savings Association Insurance Fund (SAIF) was established in place of the FSLIC. SAIF was to be administered by the FDIC.

- The Resolution Trust Corporation (RTC) was established to deal with failed thrift institutions that regulators took over after January 1, 1989.

- The RTC made it so that the insured deposits at these closed institutions were available to their customers.

- FIRREA gives Freddie Mac and Fannie Mae the job of supporting mortgages for low- and middle-income families.

Limits were placed on the portfolios of S&Ls, and standards were set to prevent concentrations of loans to single borrowers.

Junk bonds were to be completely removed from their portfolios by July 1, 1994, and investments in junk bonds were to be segregated and directed to separately capitalized subsidiaries.

Savings And Loan Crisis Summary

The Savings and Loan Crisis showed us how different aspects of regulations can affect and change an industry. Handling the crises shows us how deregulation without any oversight can have serious consequences for a whole industry and economy.

It highlights how it cannot be easy to regulate if an industry is deregulated without oversight and has a significant influence.

It highlights how even if a governing or oversight body is present, it lacks adequate resources and power. For example, the FHLBB was the governing body. Still, it could not do its job properly as it needed to be more staffed and underfunded and could not examine S&L assets properly.

It also shows how deregulation can be a double-edged sword.

At the start of deregulation, the S&Ls were showing signs of recovery. Still, with oversight, the whole industry soon went out of control, and due to their influence, it was very difficult for lawmakers to take corrective actions.

Fun Fact

The National Commission on Financial Institution Reform, Recovery and Enforcement estimated in 1993 that it would have cost the FSLIC approximately $25 billion to close all insolvent S&Ls in early 1983.

Which was only four times the FSLIC reserve at the time. But it cost taxpayers around $160 billion just because bureaucrats pushed the can down the road hoping the problem would solve itself given enough time.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?