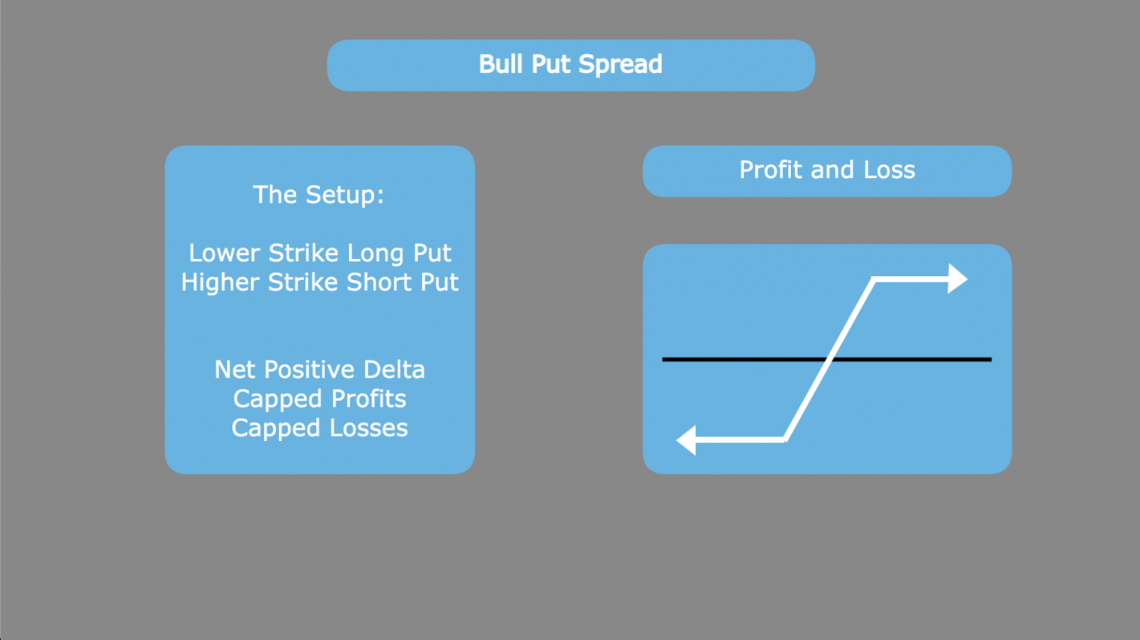

Bull Put Spread

An options strategy involves buying and selling a put option at two strike prices that expire on the same date.

What is a Bull Put Spread?

A bull put spread is an options strategy that requires multiple legs. It involves buying and selling a put option at two strike prices that expire on the same date. The bull put spread is considered to be an advanced options strategy.

In this type of put spread, the investor’s long put option is at a lower strike than their short put. The premium gained from the trade is the difference between the premium collected for selling the short-put option and the premium spent on the long-put option.

Because investors see returns as long as the short put is not too far in the money, choosing this strategy demonstrates a mildly bullish outlook on the underlying stock. It can also be said that the spread as a whole has a net positive delta.

- A bull put spread is an options trading strategy used by investors who expect a moderate rise or stability in the price of the underlying asset.

- It involves selling a put option at a higher strike price and buying another put option at a lower strike price with the same expiration date.

- The strategy has limited risk and profit potential. The maximum profit occurs if the asset's price stays above the higher strike price at expiration, while the maximum loss is if the price falls below the lower strike price.

- This strategy is typically employed by investors with a moderately bullish outlook on the underlying asset. They expect the asset’s price to stay steady or rise slightly but not necessarily make significant gains.

Understanding a Bull Put Spread

This strategy can be compared well to a naked put, which also hopes to collect a premium from a rise in stock price. The bull put spread, however, allows the investor to limit the risk associated with the short position and, in turn, lowers the premium collected.

Investors can think of the long put leg as strategic because it lowers the maximum loss on the trade.

This is because the investor has an asset in the form of the long put that increases as the price of the underlying decreases. The cash earned from selling this long put serves much like the cash held in reserve in a cash-secured put. It lowers the risk of the trade overall.

By purchasing the long put option as a hedge against the potential losses of the short put, the investor profits less from the passage of time, which would help decay the value of the short position. This, in turn, raises the break-even point when compared to a simple short put.

Furthermore, the premium paid for the long put option lowers the max profit. With a typical short put that expires worthless, the investor is able to exit the position with the full premium of the contract sold.

This is not the case with a bull put spread. The long put cuts into the premium earned from the short put, reducing the spread’s maximum profit.

The main things to remember about the bullish version of a put spread are the following:

- The strategy reflects a mildly bullish outlook

- The method allows the investor to collect a premium for selling the put spread

- Both losses and profits are capped

Relevant Options Details

When trading using advanced options strategies such as spreads, investors must understand the core components of options contracts. However, beyond just the basics, this strategy hinges on a strong understanding of the options of the greek delta.

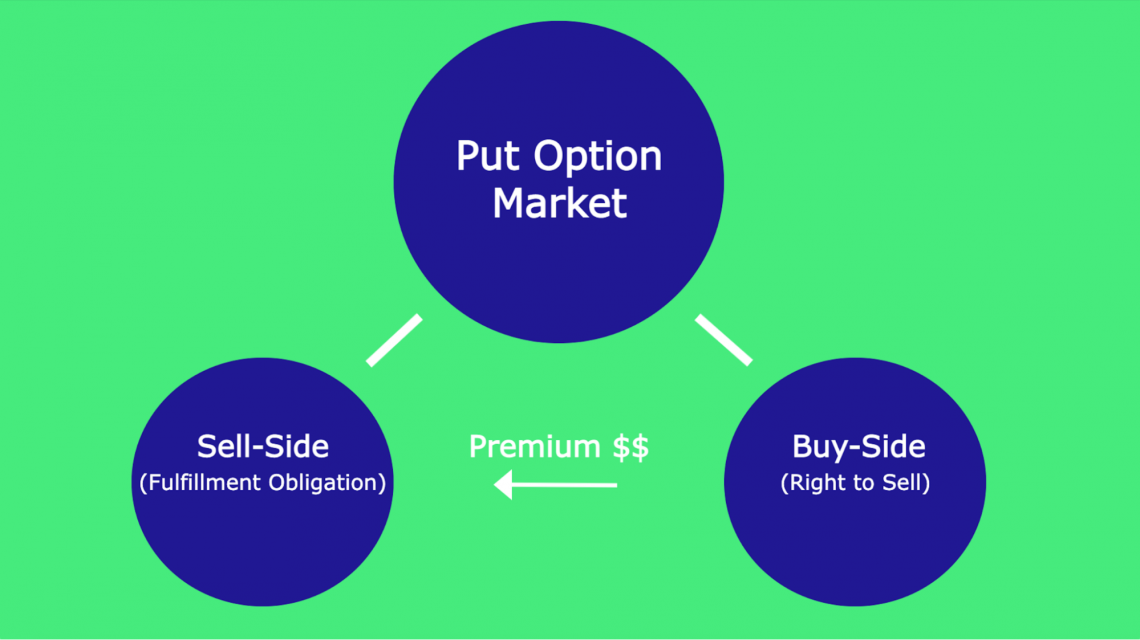

For any given options trade, there is both a long and short position. For a given put option, these two positions have the following rights and responsibilities:

- Long position - Right to sell

- Short position - Selling/fulfillment obligation

Traders on the buy side of a put option pay a premium to purchase the contract. Ownership of the contract gives the buyer the right to sell 100 shares of the underlying security at the strike price at or before the expiration date.

On the sell side of the trade, the seller writes the contract and collects the premium from the buyer. In return, they take on the risk of the trade.

In this case, the risk is a fulfillment obligation to the buyer. This would be purchasing the shares of the underlying stock to the buyer of the contract for the specified strike price up until the contract’s expiration date.

Because the bull put strategy involves buying and selling put options at different strike prices, each leg of the contract gains or loses value at different rates.

In an option contract, the greek delta tells us how much the premium of the option contract changes for each dollar shift in the price of the underlying stock.

Call options have a positive delta, and put options have a negative delta. This is because call options gain value with a rise in price, while put options decline in value with a rise in price.

For options contracts sold, we reverse the delta. This is because the goal for sellers is a worthless contract expiration. Increasing the premium would mean repurchasing the contract, and closing the position is more expensive.

We look at the net delta for an option contract with multiple legs, such as the spread we created. This tells us how the price of the spread overall changes with respect to the change in the underlying.

Because the long put position has a lower strike, the delta will have a lower magnitude. Therefore, for put options, price decreases in the underlying have a greater probability of impacting the higher-strike option than the lower-strike option.

As we can see in the option chain for VOO, strikes closer to the last price of 375.21 have a higher magnitude delta than the highlighted 355 strikes on Oct 21, 2022, put option. This highlighted put a delta of -.29, for example, while the 375 put is -.47.

Because the second leg is a short put, we reverse the sign of the negative delta and are left with a positive value for this leg. Because this strike is higher, it will always be closer to the money than the long position or more in the money.

This means that when we add the two deltas together, the short-put positive delta outweighs the long-put negative delta. Therefore, the resulting spread has a net positive delta. This means the spread gains value overall as the underlying stock price rises.

Example of a Bull Put Spread

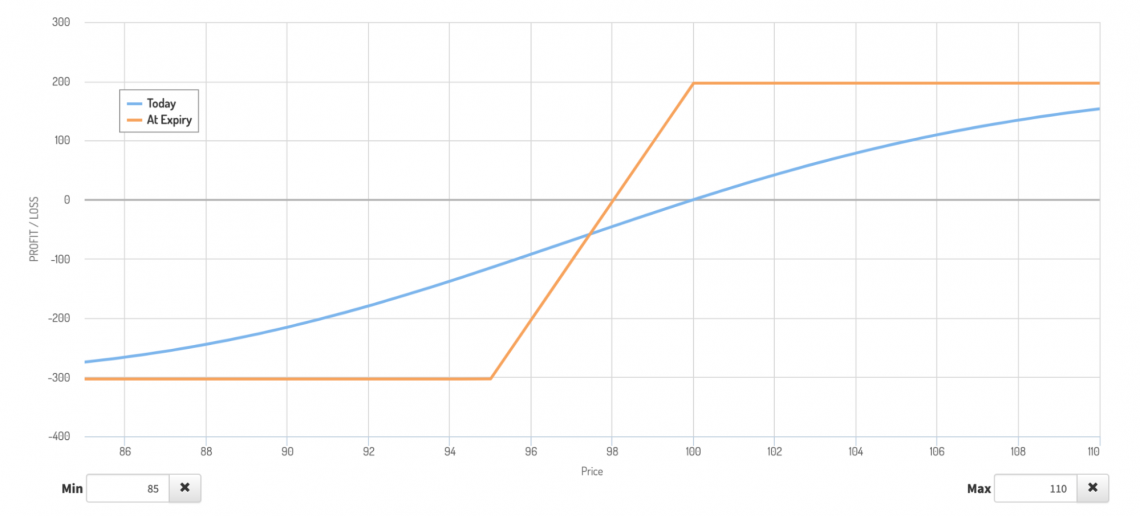

In this example, bull put spread. The investor is purchasing a put at 100 strikes and selling a put at 95 strikes. Both options expire in 30 days, and the pricing model assumes implied volatility of 30. The current price of the underlying is $100.

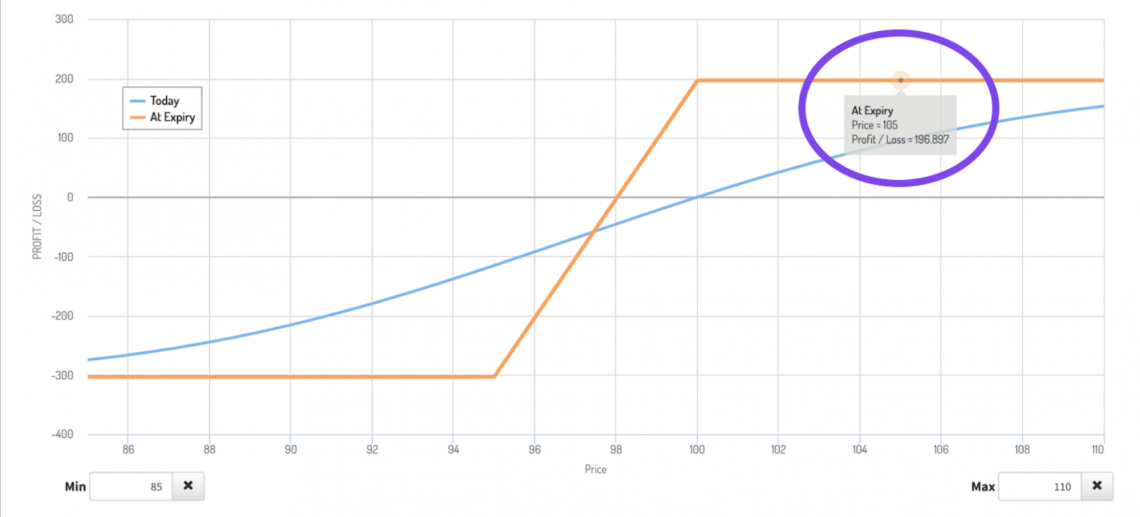

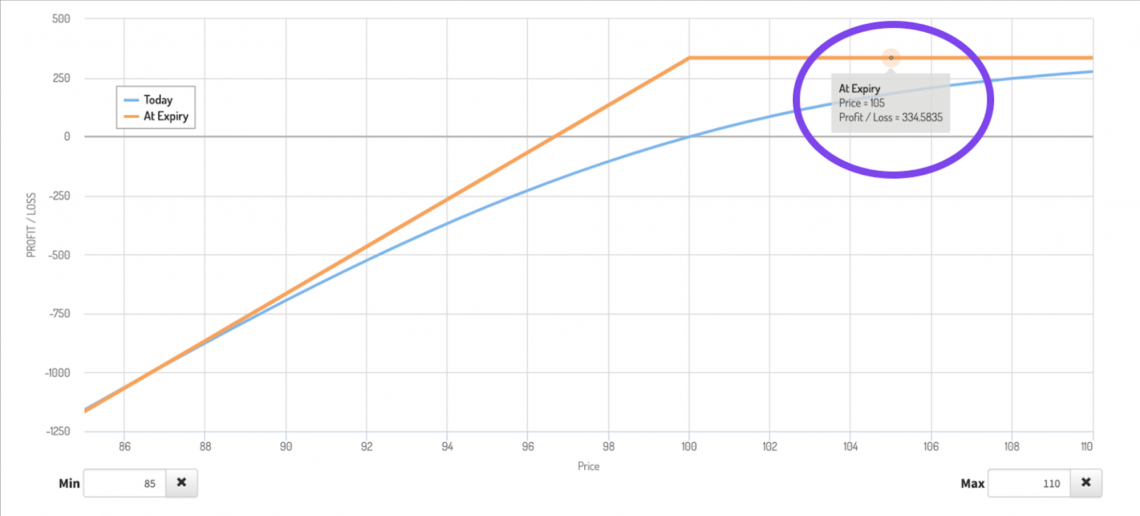

As we can see, the short position earns the investor $334.58 in premium. Subtracting the $137.68 from the long put position purchased to hedge risk, the investor has credited a net of around $196.90.

Looking at the profit and loss graph, the bullish sentiment is clear. The investor remains profitable if the stock price stays above $98.10. The premium collected gives the investor some buffer below the upper strike price.

The amount the stock can fall below the short put strike is the net premium of the spread. Note that the premium is 1/100th of the total cost, as the cost to enter is the premium multiplied by the number of shares the contract represents. The investor collected around $196.90 in net premiums.

Break Even = Short Strike - Net Spread Premium

The premium also determines the max loss but includes the distance between strikes.

Max Loss = (Long Strike - Short Strike) x 100 + Net Spread Price

Finally, The max profit also relates to the premium, as the premium determines the amount the investor earns from writing the spread.

Max Profit = Net Spread Price = Premium x 100

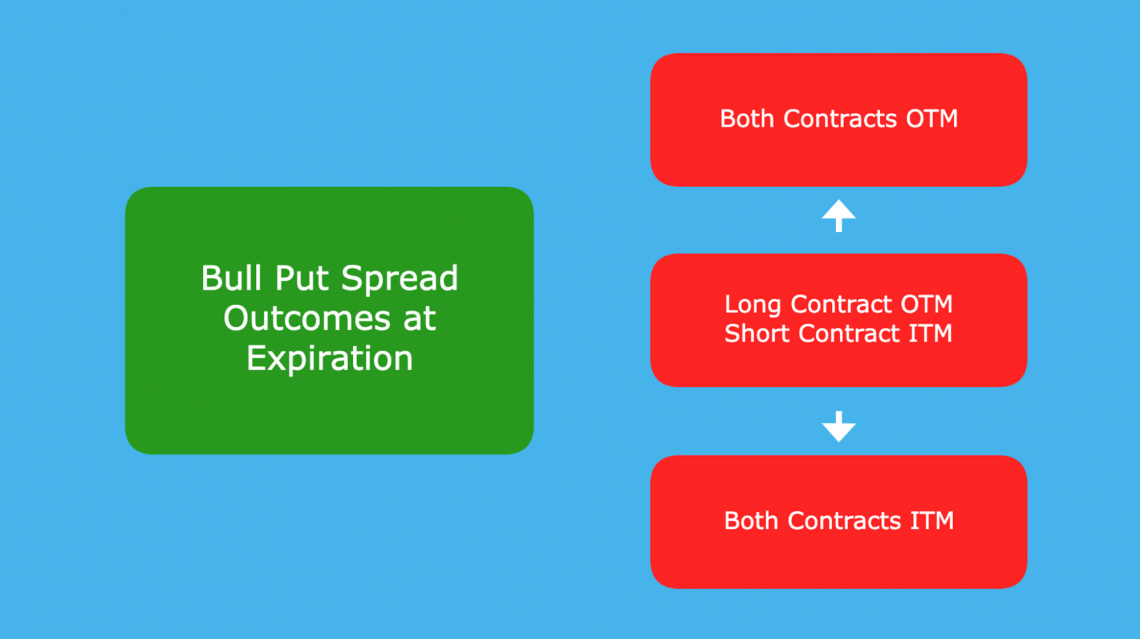

We can see exactly why each of these specific price points makes sense by looking at different expiration price scenarios.

Consider a situation where the price at expiration rose to $105, which is above the strike price of the short position.

The investor’s long position expires worthless. It is not exercised. The investor’s short position also expires worthless. It is not exercised. This means that the investor is left with the premium collected originally from selling the spread, around $196.90.

As we can see, this profit is less than that of a naked put, which would be an alternative bullish setup the investor could construct while being able to collect a premium. This reduced profit is explained by the reduced downside, which equates to less risk in the position.

Instead of having the $334.58 from selling the short position (as shown in the graph), the investor has their premium reduced from buying the 95 put.

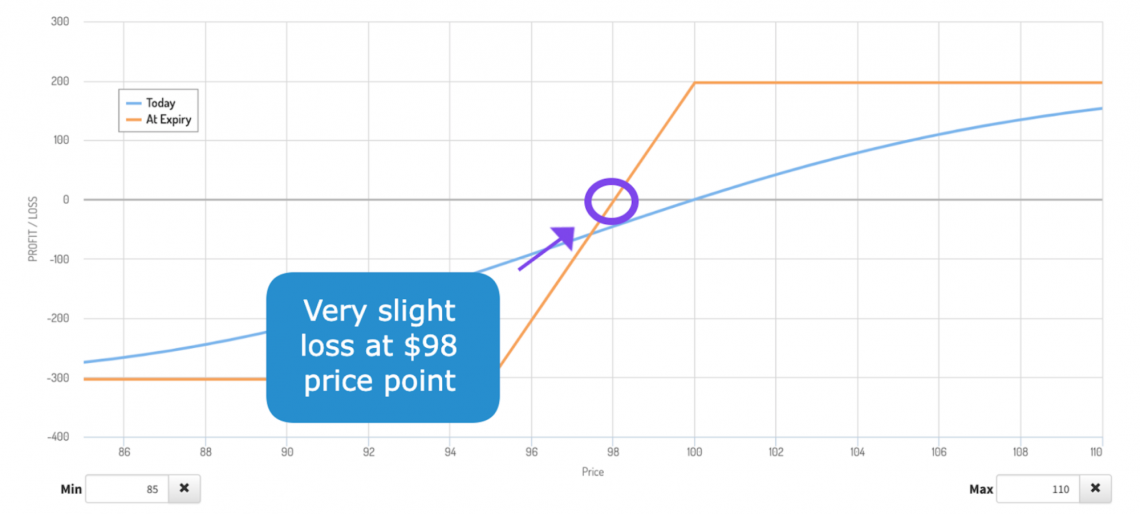

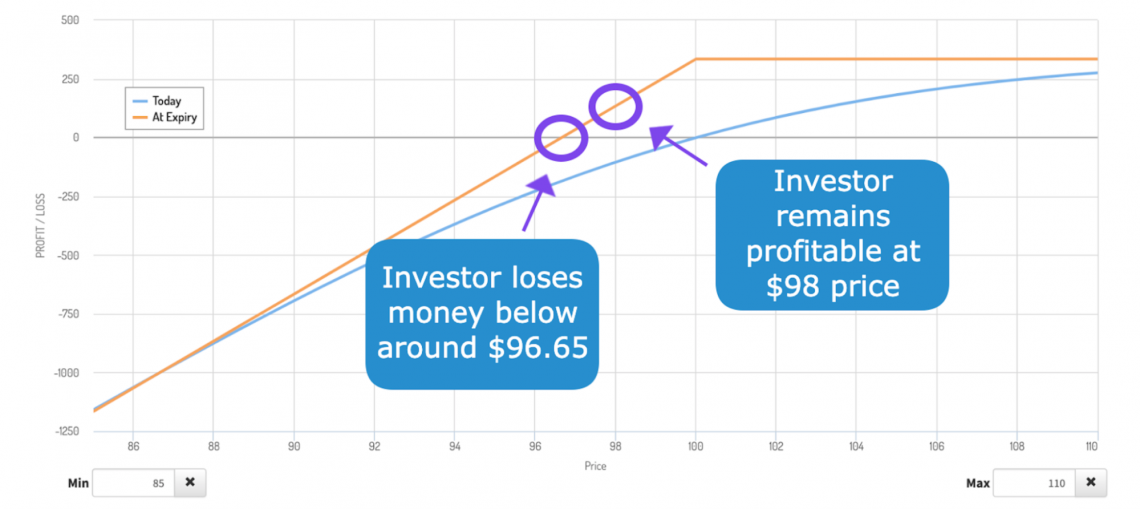

Another possibility is the underlying strike price at expiration is between the two strikes, in this case, between 100 and 95. Let’s say the closing price is $98.

In this situation, the short is in the money and is exercised. Therefore, the investor is liable for 100 shares at the $100 price.

The long put is out of the money, so the investor has no reason to exercise. The investor can sell those shares at the market price of $98. The investor loses $200 from the 2-dollar price difference.

Because the investor initially collected $196.90 from selling the spread, their loss is only $3.10.

Compared to the naked put counterpart, the investor using the bull put spread is again less profitable. If the investor had only sold the 100 puts, they would have broken even on the trade.

The collected premium with a naked put would be greater enough to cover the market price and strike price differential at expiration.

The outcome is one where the underlying market price is below the long put strike, in this case, below $95. Let’s assume that the market price is $90.

Because both puts are in the money, they are both exercised. For the investor who sold the spread, the extra premium sacrificed was worth it to hedge the downside of the short put leg.

The short put is exercised, meaning the investor must sell 100 shares at the $100 price point. Because the investor purchased the $95 put, they also have the right to sell shares to another investor for $95.

The investor loses $1000 from the short put strike price difference, buying shares at $90, but also gains $500 from their long put position. They lose $500 from exercising.

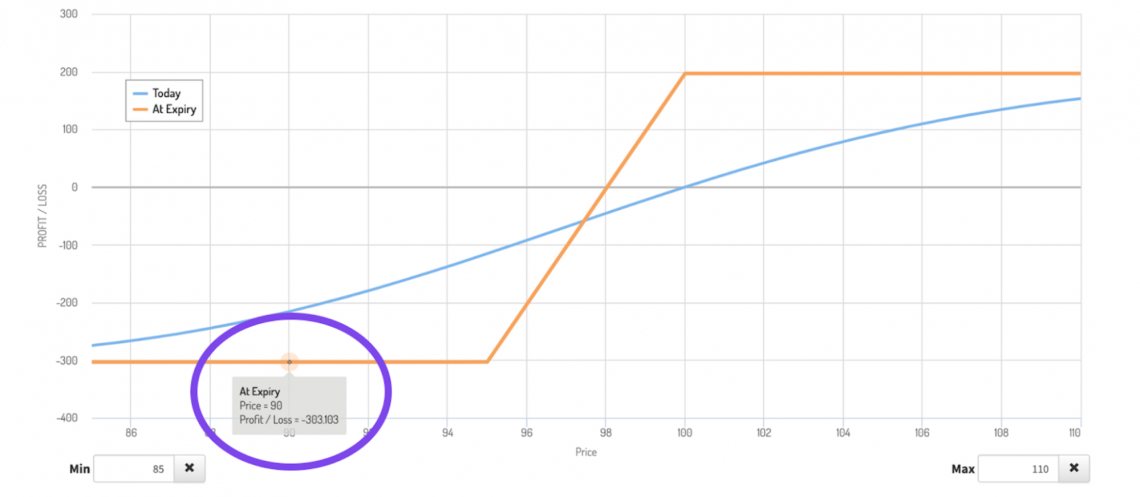

However, when the investor takes into account the premium collected, they are left with only a loss of $303.10.

The thinking is the same at any point below the long put. The investor’s losses from the short put are offset by their returns from their long put. Any difference in price leaves them with the same $303.10 loss.

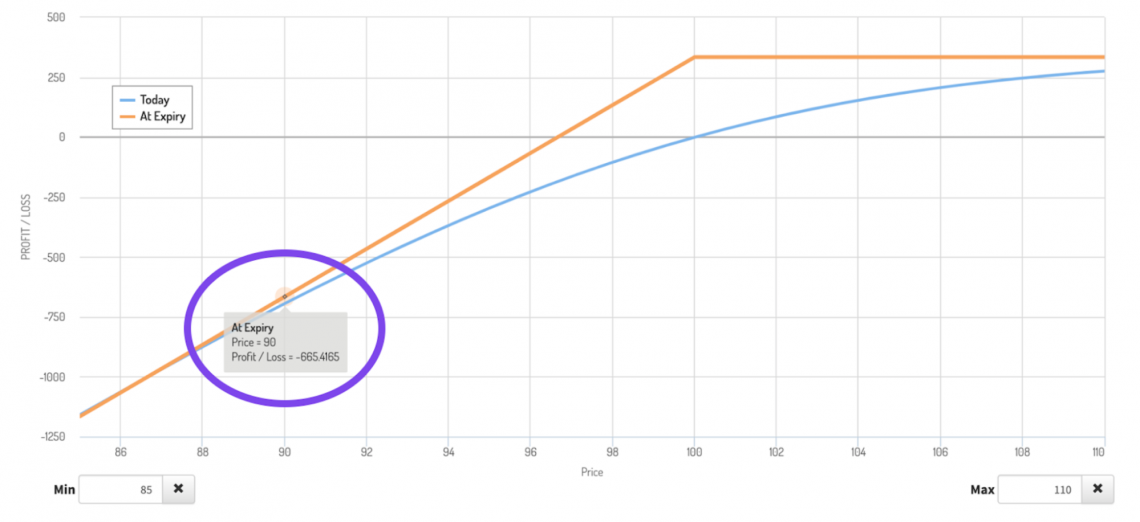

For this reason, we say the investor has a limited downside. This is extremely advantageous compared to a naked put position at certain price points, as the naked put has the potential for extreme losses.

In this case, the short-put counterpart would have lost more, around $665.41.

Conclusion

As we can see from the above profit and loss comparisons, the bull put spread is strategic in that it lowers a trader’s maximum loss with the sacrifice of smaller profits and higher break-even points compared to a naked put set up.

Because extreme price movements are less common than smaller price movements, a bull’s profitability may typically spread less than a naked put. Still, it is crucial to remember the risk is also significant.

Although the investor has a long protective put, they have to consider increased risk and responsibility for having a short leg in their investment strategy compared to just holding shares or purchasing options.

While it is true that the long put position hedges the risk associated with the short position, the possibility of an assignment before the expiration of the option is possible.

This is notable in cases where the underlying stock has a divided payment scheduled before the expiration of the put contract. An early assignment is likely if the put contract is in the money and has more time value than the expected dividend payment.

If the investor holding the spread is not paying attention, they may not realize that the assignment is likely. Forgetting to close their position by closing the entire spread or repurchasing the short leg (leaving the long position open) leaves an investor with fulfillment obligations.

In this situation, a long position is created on the investor’s account. These shares can be either resold on the market, or the long put can be exercised. The account will be liquidated if the account owner does not have enough money to purchase the shares.

These extra considerations and the complexity of detail associated with price movement are key reasons why this strategy is recommended for advanced traders.

Many brokerages will not allow investors to use this strategy without first verifying the investor’s familiarity with options and other financial information.

As with all options strategies, a greater degree of risk is associated with increased leverage when using a bull put spread. Beyond simply understanding the setup, investors should understand equity valuation based on fundamentals.

Feel free to check out our financial modeling course to understand these concepts better. Due diligence in the underlying and a strong conviction of price movement is a must-have when using strategies susceptible to extra volatility.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?