How to Choose Comparable Companies

Companies for CAA can be selected based on the relevance of their business and financial profiles to the target.

How to Choose Comparable Companies

Bankers in investment banking, private equity, or venture capital use a slew of valuation methods. One of the most widely used is comparable companies analysis. It is also known as “comparable companies,” “trading comps,” or simply “comps.”

Trading comps rely on listed companies. This is because the information about listed companies is readily available, unlike that of private companies.

The first and most crucial stage in doing a comparable company study is selecting a group of comparable businesses or a comparable universe.

The group of similar companies you discover at the start of your study serves as the foundation for the remainder of your analysis and valuation.

As such, it is critical to ensure that you select the appropriate comparable universe; if not, you run the risk of having your valuation and the effort you put into creating your model invalidated.

The idea of comps is premised on similarities. For example, similar companies share financial and business characteristics, risks, performance drivers, and other factors. Due to these similarities, a sample of comparable companies is a relevant reference point to derive a value for a given target.

Hence, selecting the appropriate companies to build an accurate, comparable universe is fundamental. Otherwise, your analysis may be skewed and unreliable.

Mastering choosing a universe of comparable companies is also beneficial for succeeding in your banking interviews.

This is a common technical question that can be asked. However, cultivating a more profound knowledge of this matter would be necessary to satisfy the recruiter’s expectations.

- Selecting an accurate comparable companies universe is essential for successfully conducting a trading comps valuation methodology.

- Comparable companies can be selected based on the relevance of their business and financial profiles to the target.

- The business profile comprises characteristics related to the core business model, such as sector, product and services, customers and end markets, distribution channels, and geography.

- The financial profile comprises characteristics related to the financial spectrum of companies, such as size, profitability, growth profile, return on investment, and credit profile.

- A thorough and detailed analysis of each component is critical to finding similar companies.

Framework for selecting comparable companies

As mentioned, we aim to choose companies with as many common traits as possible. For this, we should analyze them through the lens of their business and financial profiles.

Please remember that the characteristics we will discuss aren’t definitive and versatile.

They can be altered and completed depending on your specific needs and criteria. Different industries, timings, and trends may require specific approaches. Something that works in one environment can be inappropriate in another.

Therefore, before performing trading comps, understand the most relevant traits for the company/industry you work on.

The business profile includes such characteristics as:

- Sector

- Product and Services

- Geography

- Distribution Channels

- Customers and End Markets

As you can see, we seek companies with core business traits and similar business models.

The financial profile includes such characteristics as:

- Size

- Profitability

- Growth Profile

- Credit Profile

- Return on Investment (ROI)

We seek companies with similar key financial characteristics and metrics.

Business profile in detail

A company’s business profile transmits much information about its risks, key drivers, and opportunities. The shared core business traits are an excellent criterion for spotting comparable companies.

Sector

The term “sector” describes an industry or a market in which a company operates. So, for instance, Johnson & Johnson will belong to the healthcare industry.

Apple will belong to the technology industry, and Wells Fargo to the financial industry. The identification of a sector is only the first layer.

We can further divide companies’ sectors into sub-sectors, simplifying a search of the peer companies. For example, the industrial sector is composed of numerous sub-sectors.

The industrial sector includes:

- Automotive

- Chemicals

- Healthcare

- Building products

- Paper and packaging

Within the healthcare industry, you have sub-sectors such as:

- Pharma/biotech

- Health tech

- Medical device

- Health consulting

Moreover, even these sub-sectors can further be segmented. For instance, the health tech sub-sector contains streams such as:

- Genomics

- Robotic surgery

- Telehealth

- Drug development/AI

Note

For companies with separate business divisions, sub-sectors segmenting is essential for successful valuation.

Product And Services

The company’s products and services are central to its business model. Hence, companies with similar products and services can be considered good comparables.

Companies can provide both products and services to clients or be pure players. Also, some companies can offer an extensive range of products and/or services, whereas others are less focused.

Products are articles or substances that are manufactured or refined. Services are acts or tasks performed by one party to benefit another, with an expectation to be paid for. The integration of AI in manufacturing has transformed the industry by enabling companies to leverage advanced data analytics and automation to enhance their product development and service delivery processes. Oil, sugar, and steel are examples of products, whereas consulting and banking are examples of services.

Geography

Different regions of the world often present differences. Fundamental business drivers and characteristics vary from one continent to another.

Companies that operate in and sell to various locations are subject to varied macroeconomic environments, competition, paths to market, organizational and cost structures, and potential opportunities and risks.

It stems from local factors that are unique for every region. Examples include

- Demographics

- Economic Drivers

- Regulations

- Consumer Preferences

- Cultural Norms

Suppose a banker is looking for comparable companies for a U.S. retailer. He would mainly focus on domestic companies in this situation. In contrast, this approach might not suit global industries like oil and aluminum.

The location of these companies is not as important as the global commodity prices and supply/demand dynamics. However, even in these cases, there may still be differences in valuation based on location.

Distribution Channels

The term "distribution channels" refers to a company's tangible or intangible paths to distribute and sell its products and services. These channels are central to a company's operating strategy, performance, and, ultimately, its value.

For example, a company primarily selling to wholesale channels will have different organizational and cost structures than those selling directly to retailers or end users.

Some companies sell their products through multiple channels instead of one. For example, a flooring manufacturer may sell its products to wholesale distributors, retailers, homebuilders, and end-users.

Customers And End Markets

The terms “customer” or “client” refer to individuals or organizations who purchase a company’s products and services. Companies that serve a similar customer base have similar risks and opportunities. This is because they tend to be impacted by identical market trends and economic conditions.

Companies manufacturing automotive pieces for automobile manufacturers comply with manufacturing and distribution requirements. They are also subject to cycles and trends in the automotive industry.

The quantity and diversity of customers a company serves are also important. Some companies have a broad customer core, while others are focused on a niche market or are specialized in something very narrow.

A low customer concentration is good from a risk management perspective. But it is also beneficial to have a stable customer base. In addition, it gives better visibility and predictability of future revenues.

Note

The term “end market” refers to the broad markets where a company sells its products and services. For example, a plastics manufacturer may sell its products in several end markets. These markets could be automotive, construction, consumer products, medical devices, and packaging.

Difference between customers and end markets

Understanding a slight but subtle difference between end markets and customers is vital. For instance, a company may sell its products to the housing end market rather than directly to homebuilders.

It can sell to retailers or suppliers who sell the products to homebuilders. So the housing sector is our end market, while retailers or suppliers are our customers.

A company's performance is closely linked to various macro and micro factors that affect its end markets.

For example, macroeconomic factors significantly impact the housing industry and, consequently, a company that sells products used in this industry. These are:

- Interest rates

- Economic projections

- Fiscal et tax policies

- Unemployment levels

This means that companies selling products and/or services into the same end markets will likely have a similar performance outlook and cyclicality.

Understanding this is important when identifying comparable companies for investment or benchmarking purposes.

Financial profile in detail

Examining certain financial factors is essential to better understand a company. They can reveal crucial insights about the company's financial positioning and prop up a selection of comparables.

Size

Size really does matter. You wouldn’t buy the same clothing size for kids of 2 years and 12 years old, right? The same applies to companies.

Companies of similar size in a given sector often have similar valuation multiples. This is because they share other characteristics such as customers, growth prospects, economies of scale, purchasing power, and price sensibility.

Thus, peers are often ranked based on their size categories. For example, companies with $10bn in revenue would eventually be in another tier list than companies with $100m in revenue, assuming a sufficient number of comparable companies to distribute them through subsets.

Note

Market valuation comprises equity value and enterprise value. Key financial metrics include sales, gross profits, EBITDA, EBIT, and net income.

Profitability

Profitability measures a company’s capacity to convert sales into profit. Profitability margins are typically calculated by dividing measures of profit by sales.

The most used measures of profit are gross profits, EBITDA, EBIT, and net income.

To give an example, if Company A has:

- Gross sales of $10

- Sales of $100

Its gross profit margin would be $10/ $100 = 10%.

Frequently, companies with higher profit margins tend to benefit from higher valuation multiples, all else being equal.

Growth Profile

A company's financial performance and projected growth are crucial in determining its value. As a result, investors tend to reward companies with higher growth rates.

They assign them higher trading multiples. Organic growth is generally preferred over growth achieved through acquisitions.

The analysis of financial metrics should be performed to evaluate a company's growth profile (e.g., sales, EBITDA or EPS - earnings per share).

For well-established companies, earnings per share growth rates are typically the most meaningful. However, sales or EBITDA growth trends may be more relevant for emerging companies with little or no earnings.

Credit Profile

The credit profile of a company refers to its creditworthiness. It is a company's capacity to borrow money and pay it back. There are two typical metrics bankers take into account for this exercise.

A company's indebtedness ("leverage") and capacity to service interest payments on borrowed money. The latter is also known as an interest coverage ratio. These two factors are highly relevant to determining the risks and benefits of a given company and its sector.

There are three primary independent credit rating agencies elaborating on companies’ credit profiles:

- Moody’s (Moody’s Investors Service)

- Fitch (Fitch Ratings)

- S&P (Standard & Poor’s)

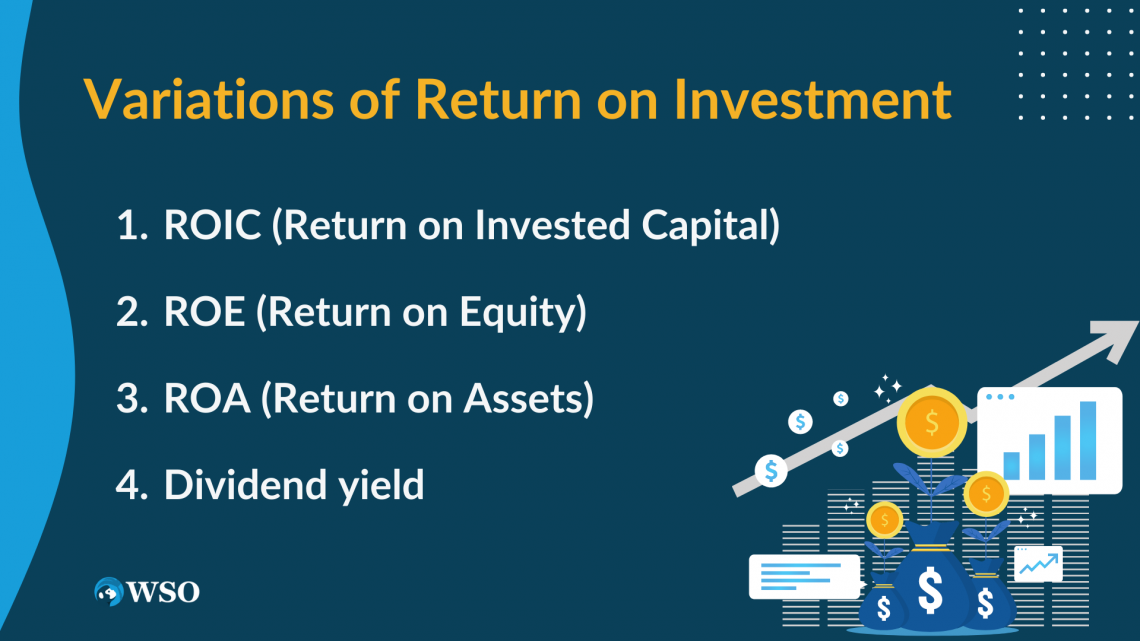

Return On Investment

Return on Investment (ROI) measures a company's ability to generate earnings for its capital providers. Capital providers are both equity and debt investors.

There are several commonly used variations of ROI:

- ROIC (Return on Invested Capital): Return on invested capital is the return generated by all available capital provided to a company. It is measured by dividing EBIT by the sum of Average Net Debt and Equity.

- ROE (Return on Equity): Return on Equity is the return generated by the capital provided to a company by its shareholders. It is measured by dividing Net Income by the Average Shareholders' Equity.

- ROA (Return on Assets): Return on Assets measures the return generated by a company's asset base, pointing out the asset efficiency of a business. It is calculated by dividing Net Income by the Average Total Assets.

- Dividend yield: Another type of return metric is the dividend yield. A dividend is a payment that a company's shareholder receives for each share owned. A dividend yield is measured by dividing a year's total dividend by a company's share price.

or Want to Sign up with your social account?