Valuation

Valuation is the process of estimating a company’s worth using financial models and structured analysis.

What is Valuation?

Valuation is the process of estimating a company’s worth using financial models and structured analysis.

It can be based on:

- Intrinsic Value: the Company’s own ability to generate cash flow. This approach is used to calculate the true worth of the business, most often through discounted cash flow (DCF)

- Relative Value: how it compares to similar companies in the same industry. This is similar to checking other house prices in the neighborhood when thinking about real estate.

- Asset-Based Value: what the Company owns minus what it owes (Assets - Liabilities). This applies to asset-heavy firms or distressed businesses.

Although people often use the words “price” and “value” interchangeably, they are not the same thing. As Warren Buffett said, “Price is what you pay. Value is what you get.”

Valuation is the foundation of investment decisions. Whether you are a private equity firm or an investor seeking stocks, valuation is a disciplined approach to measuring the worth of financial choices.

- Valuation is the process of estimating the economic worth of a business, asset, or investment.

- Three primary approaches are used: intrinsic (DCF), relative (comps), and asset-based.

- The core valuation methods include Trading Comparables, Precedent Transactions, and Discounted Cash Flow analysis, each offering a different perspective on value.

- Valuation helps investors, analysts, and managers assess whether an investment is reasonably priced, guiding their decisions in acquisitions and strategic planning.

Understanding Valuation

Valuation means linking models to real-world decisions, which is critical for investors, analysts, and strategists seeking to see beyond market noise and uncover a company’s true potential.

Valuation is context-dependent, meaning that a high-growth company startup could look expensive today but be considered cheap after projecting its future cash flows.

A mature manufacturing firm may appear stable, but if growth opportunities are limited, investors may value it conservatively, potentially making it seem undervalued compared to peers with higher growth prospects.

Valuation can be complex and requires judgment and analytical skill, but it is necessary for the correct insights. It is a decision-making tool that helps investors, entrepreneurs, and corporate leaders make informed choices, avoid overpaying, raise capital effectively, and justify mergers and acquisitions.

Types of Valuation Methodologies

There are various types of valuation, each used in different contexts. It is not one-size-fits-all.

As mentioned above, valuation is the process of determining the value of a potential investment, asset, or security, and its methods can be grouped into three broad categories.

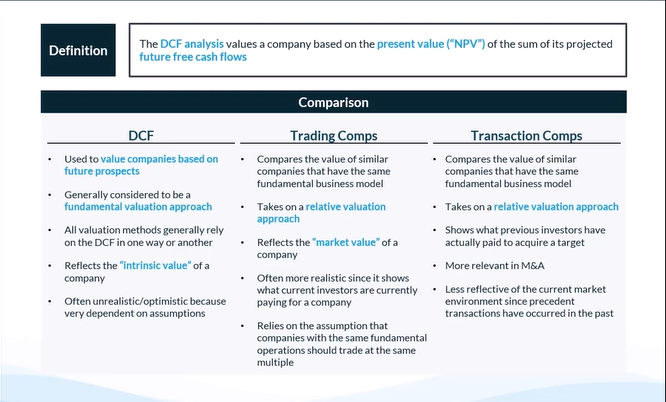

Intrinsic Valuation

It is based on a company’s future cash flows and is discounted to today’s dollars. Long-term investors should understand the fundamental drivers (e.g., DCF). Intrinsic valuation seeks to measure a company’s true worth based on its own ability to generate future cash flows.

Discounted Cash Flow (DCF) is the most common tool for projecting a company’s free cash flows over time and discounting them to present value, using a discount rate (usually the Weighted Average Cost of Capital, WACC) that reflects risk.

This method focuses on fundamentals, rather than just market perception. It is relevant for long-term investors who want to know whether the market price reflects or deviates from the Company’s intrinsic value.

Relative Valuation

It compares companies using ratios (such as EV/EBITDA, P/E, and EV/Sales) and helps benchmark them within the same industry.

Relative valuation compares a company to its peers; it does not attempt to find the absolute value of the business but instead benchmarks its position against others to determine whether it is overvalued or undervalued.

Markets often price companies relative to peers, reflecting current sentiment and providing a quick, practical comparison.

Asset-Based Valuation

It values a company by subtracting its liabilities from the fair market value of its assets and is often used for asset-heavy or distressed businesses.

It provides a floor for the Company and is useful when earnings are volatile or hostile. This method of valuation answers the question: if the Company were liquidated today, what would remain for shareholders?

Each method has its place depending on the situation, industry, and data availability.

Here is more on Relative and Intrinsic valuation in this article.

Key Valuation Methodologies

Three core valuation methodologies are commonly used.

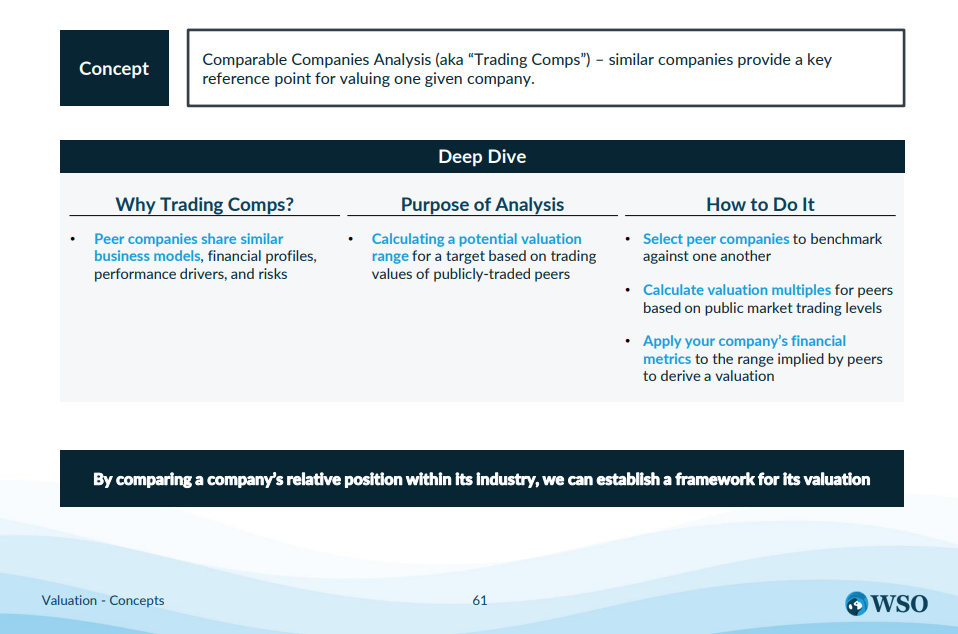

Comparable Companies Analysis (Trading Comparables)

First is trading comparables. This is where companies are valued based on the multiples of publicly traded companies that are similar in size, sector, geography, and business model, rather than in isolation.

When conducting trading comparables, valuations such as Price-to-Earnings (P/E) and Enterprise Value-to-EBITDA (EV/EBITDA) are used.

Key valuation multiples are used:

- Price-to-Earnings (P/E): Share price compared to earnings per share

- Enterprise Value to EBITDA (EV/EBITDA): Enterprise value relative to operating cash flow before interest, taxes, depreciation, and amortization

- Enterprise Value to Sales (EV/Sales): Common for high-growth companies not yet profitable

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): often used as a proxy for operating cash flow, but it excludes working capital and capex, so it’s only an approximation

You can learn more about the multiples here in this article.

Formulas to know:

Enterprise Value (EV) = Market Cap + Total Debt - Cash & Equivalents

Market Cap = Share Price x Shares Outstanding

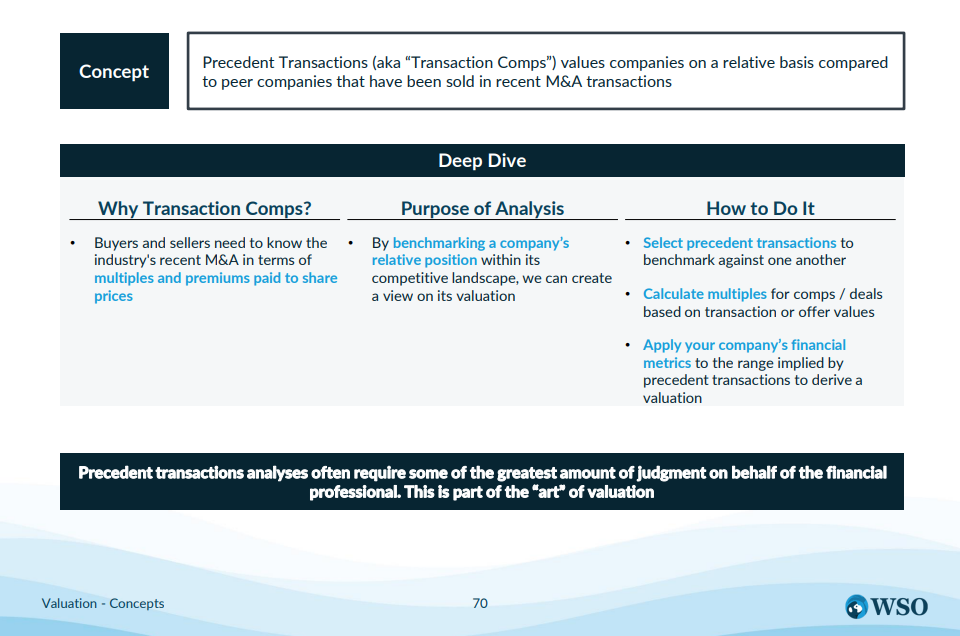

Precedent Transactions (M&A Comps)

The second core valuation methodology is Precedent Transactions, also called M&A Comps. This method values a company based on purchase prices paid for similar businesses in previous mergers or acquisitions.

How it works:

- Identify Relevant Transactions: Look for deals within the same industry, region, and size range within the last few years.

- Gather Deal Metrics: Gather information on purchase price, your target company’s revenue, EBITDA, and operational data at the time the deal was made.

- Calculate Transaction Multiples: Common multiples include EV/EBITDA and EV/Revenue, reflecting the acquisition price relative to the Company’s performance.

- Apply Multiples to the Target Company: You can estimate your valuation by applying your observed multiples to your Company’s metrics.

Precedent Transactions are helpful because they capture the control premium —the extra price buyers pay to own the whole Company. They also reflect real-world market sentiment for acquisitions in the sector and are relevant for M&A negotiations and exit strategy planning.

However, market conditions at the time of transactions can heavily influence multiples, skewing them and making them less reliable when applied across different economic environments.

Discounted Cash Flow (DCF) Analysis

Third is Discounted Cash Flow Analysis (DCF), one of the most widely discussed methodologies. This method enables us to project a company’s future free cash flows and then discount them back to their present value using a discount rate, typically the Weighted Average Cost of Capital (WACC).

Here is the DCF process simplified:

- Project Free Cash Flows

- Determine the Discount Rate (WACC)

- Calculate the Terminal Value (Estimate the value past 10 years using an exit multiple or the Gordon Growth Model)

- Discount All Cash Flows to Present Value (Converts future amounts into current dollars)

- Sum the Present Values (The total gives the intrinsic value of the Company)

Formulas to know:

Free Cash Flow (FCF) = EBIT × (1−Tax Rate) + Depreciation & Amortization − Capital Expenditures − ΔWorking Capital

Weighted Average Cost of Capital (WACC) = E/(E + D) × re + D/(E+D) × rd × (1−T)

Where:

- E = Market Value of Equity

- D = Market Value of Debt

- re = Cost of Equity (via CAPM, see below)

- rd = Cost of Debt

- T = Corporate Tax Rate

Cost of Equity (CAPM) = re = rf + β× (rm−rf )

Where:

- rf = Risk-free rate (e.g., Treasury yield)

- β = Company’s stock volatility vs. market

- rm−rf = Equity risk premium

Present Value of Free Cash Flows = PV(FCFt) = FCFt / (1 + WACC)t

Valuation FAQs

Valuation helps investors and analysts estimate the value of a company or asset, enabling them to make informed investment decisions, evaluate mergers and acquisitions (M&A) deals, and determine whether a stock is overvalued or undervalued.

There is no single “best” method, but analysts often employ a combination of techniques to support their work. Their choice depends on the industry they are in, the Company's stage, and the available data.

Intangible assets, such as brand value, can be included, but this is challenging. Because traditional asset-based valuation may overlook intangibles, analysts often adjust their valuations to account for these.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?