Institutional Floor Building: Dissecting the Recent Form 4 Flow in HealthTech

The current macro environment has effectively nuked valuation multiples in the healthcare software and SaaS space. Between shifting hospital budgets and prolonged sales cycles, the street has priced in a near-doomsday scenario for mid-cap health-tech. However, while the broader market is busy trying to catch a bottom based purely on technicals, the actual tape tells a much more concentrated, fundamental story. If you look past the sell-side downgrades and retail noise, there is a very distinct divergence between public sentiment and actual insider capital allocation.

The Form 4 Divergence: What the Tape is Showing

Recent Form 4 filings show a noticeable increase in major stakeholder accumulation across the battered tech and healthcare software sectors. To be clear, this isn't just routine equity vesting or RSU distribution. We are seeing actual, heavy open-market purchases. When executives, board members, and 10% owners lock up significant fund capital during a major drawdown, they are essentially signaling that the valuation disconnect has become too mathematically wide to ignore. These entities have direct visibility into ARR (Annual Recurring Revenue) pipelines, churn rates, and operational leverage that external analysts simply do not possess.

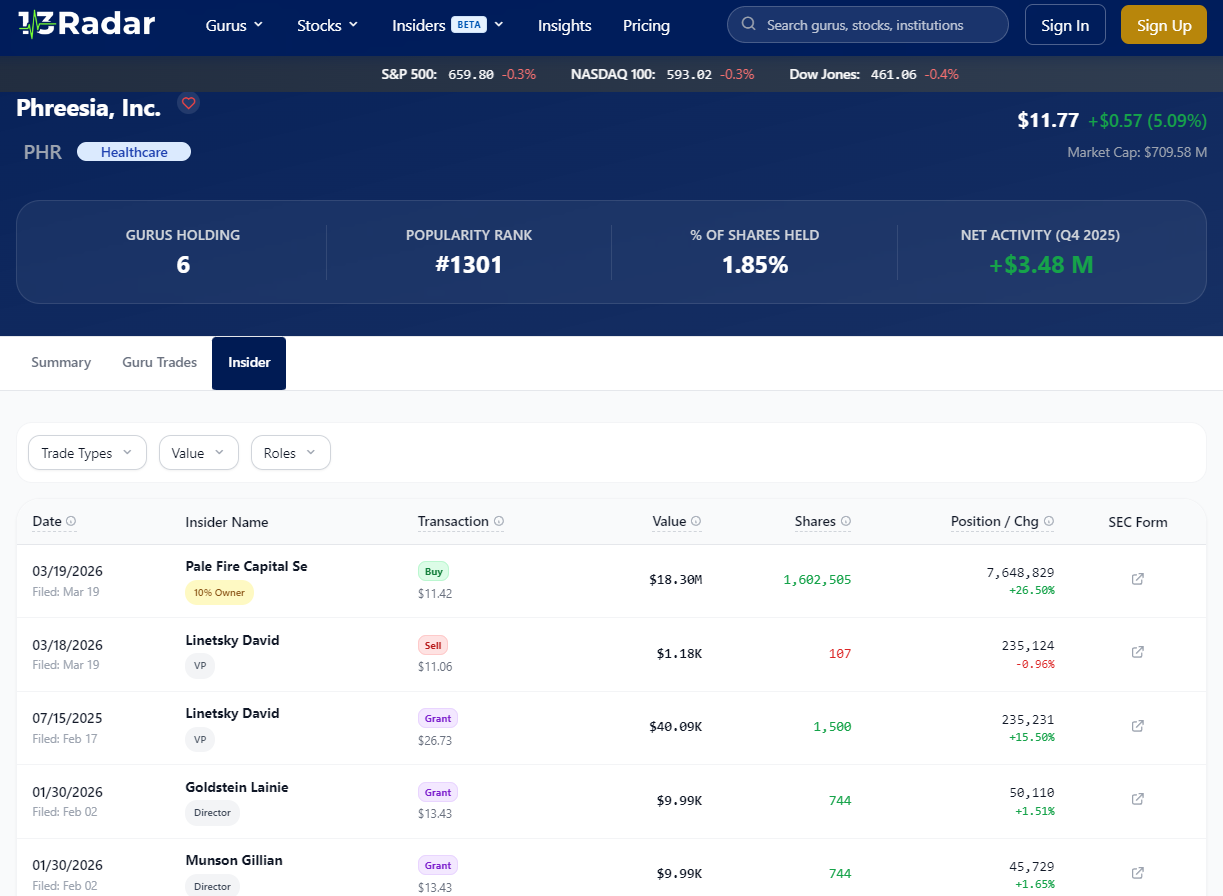

🔥 DEEP DIVE: The $PHR Liquidity Absorption 🔥

One of the more glaring examples of this dynamic right now is Phreesia ($PHR). The equity has been taken to the woodshed along with its peer group, but the institutional footprint being established at these levels is hard to ignore for anyone tracking the flow. If you look at the recent PHR insider buying, it’s not just token, optics-driven purchases by mid-level directors. We are looking at major 10% owners executing relentless, multi-million-dollar block buys, effectively stepping in to absorb the retail and passive ETF selling pressure. This level of concentrated size typically indicates that a hard fundamental floor is being established by the entities with the deepest understanding of the company's unit economics.

The Trade Mechanics: Why This Matters for the Buy-Side

From a structural and trading standpoint, heavy insider accumulation during a period of broader sector capitulation fundamentally alters the risk/reward asymmetry. It doesn't guarantee that the equity will rip higher tomorrow, but it drastically reduces the downside tail risk and creates massive friction for short sellers. As short interest remains relatively elevated across the mid-cap software sector, these massive insider blocks effectively remove active float from the market. It creates a structural powder keg for a potential mean reversion once the macro headwinds slightly pivot. It’s an interesting structural dynamic worth monitoring as we head into the next earnings cycle. Curious to hear if anyone else on the buy-side is tracking this specific Form 4 flow, or if the consensus here is that it's just catching a falling knife.

Eaque est dolores consequuntur voluptates maiores vel. Omnis labore excepturi enim id. Quisquam eligendi excepturi laborum corporis tempore. Quis adipisci culpa laboriosam in.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...