The Alpha in Illiquidity: Why the $2B-$10B Market Cap Range is the Last True Arbitrage

For those of us tracking institutional flows, the efficiency of the large-cap market has made generating consistent alpha incredibly difficult. When 50+ analysts cover a single ticker like NVDA or AAPL, the information advantage is effectively zero. The consensus view is priced in within milliseconds. However, the narrative shifts dramatically as you move down the capitalization stack. The current market environment (Jan 2026) has created a significant dislocation in the small-to-mid-cap space, offering a classic arbitrage opportunity for fundamental stock pickers who are willing to do the actual diligence work rather than relying on sell-side notes.

The thesis is simple: Information Asymmetry. While the algos dominate the S&P 500, the Russell 2000 constituents often lack meaningful coverage. This is where the "Buy-side" earns its keep. We are seeing a divergence where generalist funds are exiting these positions due to liquidity constraints, while specialized managers are stepping in to acquire cash-flowing assets at distressed multiples.

The "Coverage Cliff" and Valuation Disconnects

The primary driver of this opportunity is the lack of institutional eyes on the prize. Data shows that once a company drops below a $5B market cap, analyst coverage drops by over 70%. This creates mispricing. A disciplined long-only strategy in this environment isn't about macro forecasting; it's about balance sheet forensics. It requires identifying companies with sustainable ROIC (Return on Invested Capital) that are being punished simply because they are in an out-of-favor ETF basket.

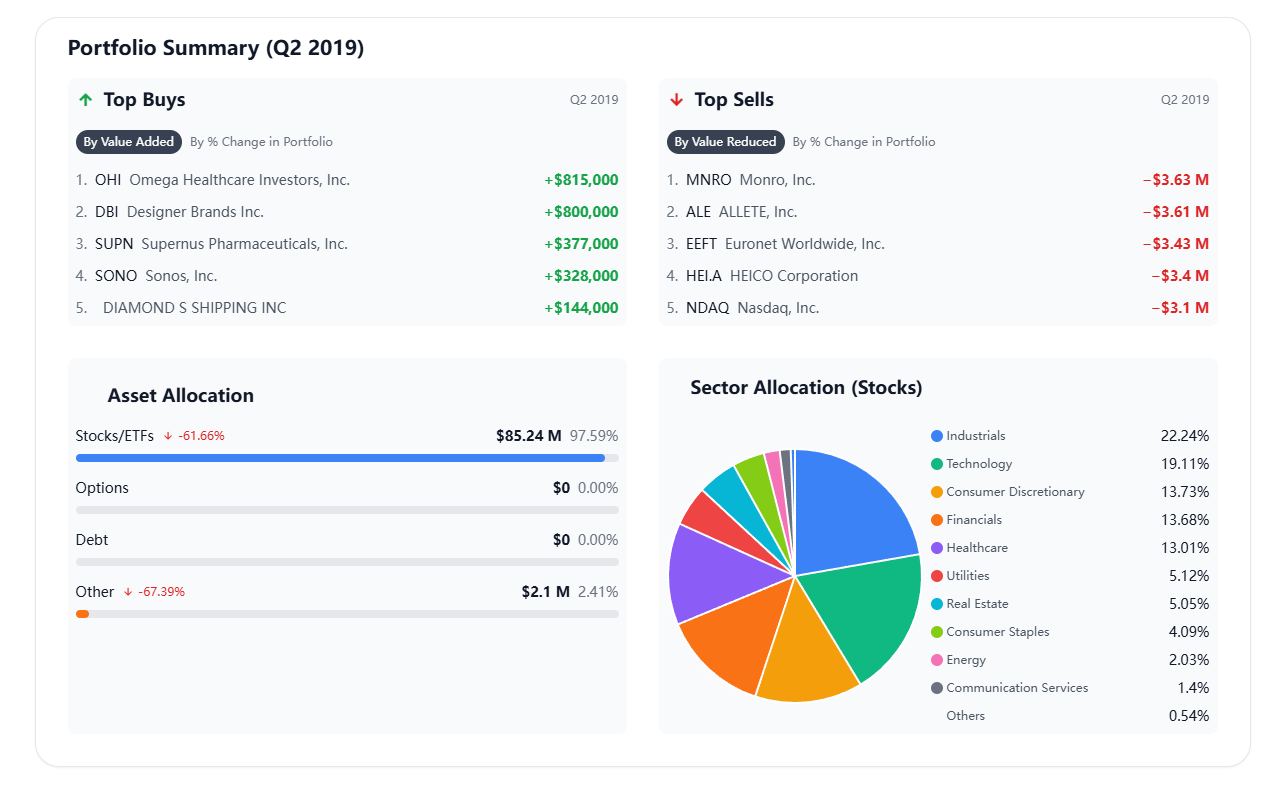

We can observe this methodology in practice by studying the historical 13F filings of dedicated small-cap specialists. For instance, the portfolio construction of firms like eagle boston investment management often reflects a "quality bias"—screening for low leverage and high insider ownership. Unlike multi-strat pods that churn positions weekly, these focused strategies tend to hold through volatility, treating the liquidity premium as a feature, not a bug. They are effectively acting as the liquidity providers of last resort for high-quality assets.

⚡ STRUCTURAL EDGE: The Liquidity Moat

Here lies the paradox that keeps this asset class inefficient:

Capacity Constraints: Large AUM funds literally cannot invest here. If a $50B fund tries to build a meaningful position in a $2B company, they move the market too much. This structural barrier protects smaller, nimble funds from competition.

The "Tourist" Effect: When generalist funds dip into small caps, they are the first to panic sell during drawdowns. This creates the entry points for the specialists.

Sector Specifics: Where the Puck is Going

Looking at the current quarter's aggregate filings, the "Smart Money" rotation is evident. There is a distinct move away from unprofitable SaaS (Software as a Service) and into niche industrials and regional financials. The logic is grounded in the current rate environment. Companies that manufacture physical goods or provide essential local services have shown an ability to maintain margins that software companies, currently fighting a price war, cannot.

Conclusion: The Return of Fundamental Analysis

For those in the industry or looking to break in, the message from the 2026 data is clear: Financial modeling matters again. The era of buying a ticker because it mentioned "AI" on an earnings call is over. The funds that are outperforming are those doing the ground work—channel checks, supplier calls, and rigorous cash flow analysis. The small-cap space remains the last frontier where hard work actually correlates with returns. It is less about being smarter than the market, and more about looking where the market isn't looking.

Porro laboriosam dicta aut rerum tenetur suscipit aut. Voluptatem porro qui aspernatur vitae quia. Totam consequatur ex temporibus architecto ab ducimus quos vel.

Ut officia blanditiis eveniet at qui. Doloribus et ut praesentium explicabo illo. Eum natus alias sed praesentium eos odio quia. Repellendus veniam repellendus ut culpa sapiente praesentium eius.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...